Reliance, Inc. RS is benefiting from strong end-market demand and strategic acquisitions that are expanding its capabilities and market presence, while weak semiconductor and commercial aerospace markets and higher aluminum and tariff-related costs continue to pressure margins.

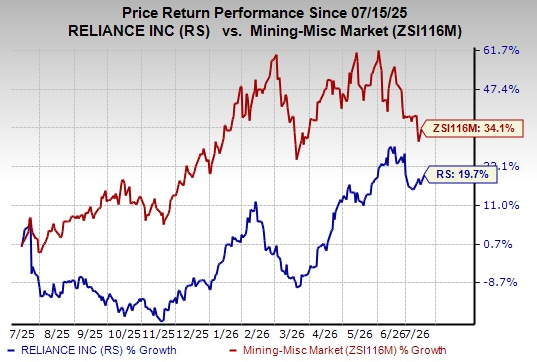

RS stock has gained 19.7% in the past year compared with the Zacks Mining - Miscellaneous industry’s 34.1% growth.

Let’s find out why RS stock is worth retaining at the moment.

Strong Shipments and Acquisitions Aid Reliance

Reliance reported first-quarter 2026 tons sold of roughly 1.673 million, up 9.4% sequentially and 2.7% year over year, marking its 13th consecutive quarter of outperforming industry shipment trends.

The company continues to benefit from strong demand in non-residential construction, driven by public infrastructure, heavy civil construction, data centers, energy infrastructure and manufacturing projects.

Through its AMI Metals subsidiary, Reliance secured major Department of Homeland Security border wall contracts that are expected to support revenue growth. Demand also remained healthy across automotive toll processing, semiconductors, defense, shipbuilding, industrial machinery and nuclear-related markets, particularly those tied to small modular reactor programs.

Reliance continues to strengthen its growth profile through acquisitions that expand its geographic footprint, product offerings and value-added processing capabilities. Earlier acquisitions, such as Metals USA, Tubular Steel, Best Manufacturing, Ferguson, All Metals, Fry Steel Company and Merfish United, enhanced its service center network and higher-margin product mix.

Recent acquisitions, including Rotax, Admiral Metals, Nu-Tech Precision Metals, Southern Steel Supply, Cooksey Iron & Metal Co. and American Alloy, further increase its presence in attractive U.S. growth markets.

Tariffs and Higher Costs Continue to Weigh on Reliance

RS continues to face weak demand in semiconductor and commercial aerospace markets, as U.S. chip plant delays, customer pullbacks and elevated inventory levels weigh on specialty operations despite a gradual improvement in build rates.

Tariffs on materials are increasing costs, particularly in aluminum. The 50% Section 232 aluminum tariffs are compressing gross profit margins as Reliance is unable to fully pass through the tariff-related cost increases to customers.

Reliance is exposed to aluminum cost increases due to tariffs amid an elevated supply and soft demand environment. Higher-than-expected material costs led to last-in, first-out (LIFO) first-quarter 2026 LIFO expense of $37.5 million compared with the company’s estimate of $25 million. The company also raised its full-year 2026 LIFO expense outlook to $150 million from the prior $100 million estimate, mainly due to elevated carbon steel and aluminum product costs.

Reliance, Inc. Price and Consensus

Reliance, Inc. price-consensus-chart | Reliance, Inc. Quote

RS’ Zacks Rank & Key Picks

RS carries a Zacks Rank #3 (Hold).

Some better-ranked stocks in the Basic Materials space are CSW Industrials, Inc. CSW, Idaho Strategic Resources, Inc. IDR and Southern Copper Corporation SCCO. CSW, IDR and SCCO carry a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for CSW’s current-year earnings stands at $12.52 per share, implying a 20.6% year-over-year increase. Its earnings beat the Zacks Consensus Estimate in three of the trailing four quarters and missed once, with the average surprise being 3.8%.

The Zacks Consensus Estimate for IDR’s current-year earnings is pegged at $1.52 per share, implying a 33.3% year-over-year increase. Its earnings beat the Zacks Consensus Estimate in three of the trailing four quarters and missed once, with the average surprise being 68.7%.

The Zacks Consensus Estimate for SCCO’s current-year earnings is pegged at $7.8 per share, indicating a 48.9% year-over-year increase. Its earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 9.1%.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Reliance, Inc. (RS): Free Stock Analysis Report

Southern Copper Corporation (SCCO): Free Stock Analysis Report

Idaho Strategic Resources, Inc. (IDR): Free Stock Analysis Report

CSW Industrials, Inc. (CSW): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).