FTI Consulting, Inc. FCN shares have slipped 1.2% in the past year. While the shares have experienced a slight dip, the industry has plummeted 42.3%. The Zacks S&P 500 Composite has rallied 26.3% over the same period.

The Zacks Consensus Estimate for 2026 revenues is pegged at $4 billion. The figure is expected to increase 6.2% year over year. For 2027, the consensus estimate is pinned at $4.3 billion, suggesting a 7.3% rise from the preceding year’s actual.

For EPS, the consensus mark for 2026 is pegged at $9.1, indicating a 3.1% year-over-year rally. The Zacks Consensus Estimate for 2027 EPS is set at $11.29. The figure is expected to grow 24.1% from the preceding year’s actual.

Factors That Augur Well for FCN’s Success

Diversification & International Operations Aid Top Line: FCN’s diversification mitigates the impacts of macroeconomic headwinds, crises, events and changes in a particular practice, industry, or country. In 2025, the company generated 37% of its revenues from international operations. The recent performance paints a growth picture, wherein FCN generated $983.3 million in revenues in the first quarter of 2026, up 9.5% year over year. Management is optimistic and banking on the growth trajectory, reaffirming its 2026 revenue guidance of $3.94-$4.10 billion.

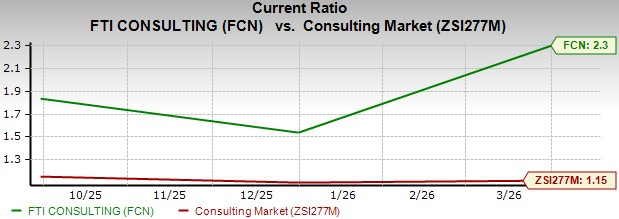

Robust Liquidity Position: The company ended 2025 with a current ratio of 1.56, a figure that bodes well with investors as it highlights FCN’s ability to pay off short-term obligations with ease. The company held this performance as it recorded a current ratio of 2.3 during the first quarter of 2026, outpacing the industry average of 1.15. FCN’s liquidity relies on its strong balance sheet position that ended the first quarter of 2026 with a cash chest of $198 million against no current debt.

Shareholder-Friendly Actions: In 2023, 2024 and 2025, the company repurchased shares worth $21 million, $10.2 million and $858.7 million, respectively. This initiative instills investor confidence. We expect investors to have been flattered by FCN repurchasing 787,098 shares during the first quarter of 2026 for $126.8 million. The company’s bottom line moved up to $1.9 from the year-ago quarter’s $1.74 despite lower net income, highlighting the success of its buyback strategy that supported per-share value.

Risks Faced by FTI Consulting

Cash Flow Contraction: FCN experienced substantial turbulence in cash flow flexibility during 2025. The company ended 2025 with an operating cash flow of $152.1 million, down from the preceding year’s $395.1 million due to higher forgivable loan issuances, compensation and income tax payments. This drag in the operational cash flow led to a decline in the free cash flow to $93.6 million in 2025 from the preceding year’s $360.2 million.

On a similar note, the company reported a severe cash depletion during 2025, as evidenced by a 59.9% year-over-year drag in cash and cash equivalents.

Bottom-Line Shoulders Cost Pressure: During 2025, FCN experienced a 14.5% year-over-year jump in operating expenses, demonstrating an acceleration from a 7.7% year-over-year increase in 2024. This substantial rise has been primarily caused by $54.7 million year-over-year growth in direct costs of revenues and special charges of $25.3 million in 2025, exceeding growth of three times from the preceding year. This rising cost structure left an imprint on the company’s profitability, as net income declined by $9.2 million or 3.3%, year over year in 2025.

Nil Dividend: FCN has never declared a dividend and currently does not have any plan to pay out cash dividends on common stock. Therefore, the only way for investors to gain is price appreciation, which is not a guaranteed phenomenon. Hence, investors seeking income are expected to refrain from investing in this stock.

FCN’s Zacks Rank & Stocks to Consider

The company has a Zacks Rank #3 (Hold) at present.

Some better-ranked stocks from the broader Zacks Business Services sector are Coherent Corp. COHR and Conduent CNDT, currently sporting a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Coherent Corp has a long-term earnings growth expectation of 46.8%. Coherent Corp delivered a trailing four-quarter earnings surprise of 6.2%, on average.

Conduent has a long-term earnings growth expectation of 8%. Conduent delivered a trailing four-quarter earnings surprise of 4%, on average.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

FTI Consulting, Inc. (FCN): Free Stock Analysis Report

Coherent Corp. (COHR): Free Stock Analysis Report

Conduent Inc. (CNDT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).