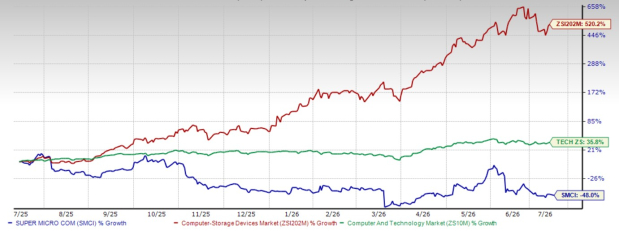

Super Micro Computer SMCI stock’s 52-week high was recorded at $62.36 on July 31, 2025. Since then, SMCI stock has declined 55.6%. Year to date, SMCI shares have lost 48%, underperforming the Zacks Computer- Storage Devices industry and the Zacks Computer and Technology sector’s growth of 520.2% and 35.8%, respectively.

SMCI YTD Performance Chart

Image Source: Zacks Investment Research

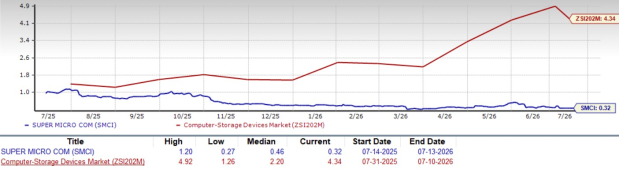

This underperformance has led the stock to trade at a discounted price-to-sales (P/S) multiple of 0.32X compared to the industry’s P/S multiple of 4.34X.

SMCI Forward 12-Month (P/S) Valuation Chart

Image Source: Zacks Investment Research

Given these dynamics, investors are wondering if it is the right time to accumulate SMCI stock or exit it before further decline. Let’s discuss the fundamentals further to understand if you should buy, sell or hold SMCI stock at present.

SMCI Grapples With Rising Inventory and Cash Flow Pressures

Super Micro Computer’s cash flow and working capital profile weakened significantly in the third quarter of fiscal 2026. The company reported cash flow used in operations of approximately $6.6 billion during the quarter compared with only $24 million used in the previous quarter. The deterioration was driven by a large reduction in accounts payable and continued inventory buildup.

SMCI’s cash conversion cycle increased sharply to 106 days in the third quarter of fiscal 2026 from 54 days in the prior quarter, while days inventory outstanding rose to 106 days from 63 days. These trends indicate rising working capital intensity and execution risk as SMCI scales its AI infrastructure business. If customer deployment timelines continue to shift or collections slow further, the company may face additional liquidity pressure.

Super Micro Computer continues to face inventory-related risks tied to the rapidly evolving AI hardware market. The company recorded inventory valuation adjustment write-downs of approximately $239.3 million during the first nine months of fiscal 2026, largely related to older-generation GPUs and components.

While management stated that newer AI platforms such as NVIDIA GB300 NVL72 and AMD MI350/355 are ramping up aggressively, elevated inventory levels remain a concern. The company had nearly $11.1 billion in inventory at the end of the third quarter of fiscal 2026, up from $10.6 billion in the previous quarter. Such a sizable inventory position could lead to additional write-downs or working capital pressure if customer demand or technology cycles shift unexpectedly.

Stiff Competition Poses Challenge to SMCI Stock

The competition in the AI infrastructure market is intensifying rapidly. Big players like Hewlett Packard Enterprise HPE, Dell Technologies DELL and Cisco CSCO are competing with SMCI in this space. Dell Technologies is a major supplier of servers and storage systems, with a broad customer base across enterprises and cloud providers.

DELL’s scale, established distribution and service offerings give it an edge in winning large contracts. However, Dell Technologies has not grown as quickly as SMCI in AI-specific systems; its ability to bundle hardware with services makes it a strong rival. Hewlett Packard Enterprise is also expanding aggressively into AI and high-performance computing.

HPE’s GreenLake platform provides customers with flexible, cloud-like consumption models, which can be attractive to enterprises. Hewlett Packard Enterprise’s focus on hybrid cloud and AI workloads positions it as a direct competitor in areas where SMCI is seeking growth through its DCBBS strategy.

Hewlett Packard Enterprise offers a range of servers, including HPE ProLiant, HPE Synergy, HPE BladeSystem and HPE Moonshot servers. Dell Technologies has built the Dell AI Factory in collaboration with NVIDIA. Dell Technologies also collaborated with Red Hat Enterprise Linux AI for Dell PowerEdge servers. Cisco has also taken $5.3 billion of hyperscaler AI infrastructure orders year to date in fiscal 2026 and raised its full-year order outlook to $9 billion from $5 billion.

Competition from DELL, HPE and Cisco can lead to price competition, leading to margin pressure for all the players. These factors have led SMCI’s bottom line to be volatile throughout 2025 and 2026. The Zacks Consensus Estimate for SMCI’s fiscal 2026 earnings per share has been pegged at $2.59, indicating a year-over-year increase of 26%. The estimates have remained unchanged over the past 30 days.

Image Source: Zacks Investment Research

Conclusion: What Should Investors Do With SMCI Stock?

Although SMCI trades at a steep valuation discount after falling 56% from its 52-week high, rising inventory, deteriorating cash flow, higher working capital requirements and intensifying competition remain significant concerns. Until the company demonstrates stronger execution and healthier cash generation, investors should avoid the stock and consider selling or staying on the sidelines. Considering these factors, we suggest that investors should stay away from this Zacks Rank #4 (Sell) stock for the time being.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cisco Systems, Inc. (CSCO): Free Stock Analysis Report

Dell Technologies Inc. (DELL): Free Stock Analysis Report

Super Micro Computer, Inc. (SMCI): Free Stock Analysis Report

Hewlett Packard Enterprise Company (HPE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).