The semiconductor industry is reshaped by AI, advanced packaging, HBM and increasingly complex chip architectures. As semiconductor manufacturers race to improve yields and reduce defects, wafer inspection and metrology have become indispensable. Two companies benefiting from this trend are Onto Innovation, Inc. ONTO and Camtek Ltd. CAMT.

Per a report from Fortune Business Insights, the global wafer inspection equipment market is expected to go from $7.22 billion in 2026 to $13.52 billion by 2034 at a CAGR of 8.2%. Both Onto Innovation and Camtek specialize in helping semiconductor manufacturers detect these defects early, improving production yields and lowering manufacturing costs. As AI infrastructure spending continues to rise, demand for inspection equipment is expected to remain robust over the long run.

While both companies operate in semiconductor process control and inspection, they have different business models, customer exposure and growth trajectories. Here's a closer look at which stock appears to offer the better long-term investment opportunity.

The Case for CAMT Stock

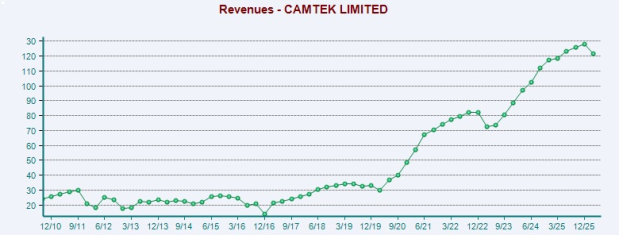

Camtek focuses primarily on inspection and metrology solutions for advanced semiconductor packaging. The company has consistently delivered strong revenue growth, high operating margins and returns on invested capital. It has become a preferred supplier for many advanced packaging applications tied directly to AI processors. Camtek's record order intake reinforces confidence in its 2026-2027 growth outlook, supported by more than $260 million in expected revenue from key customers. The company is expanding its presence in AI, HPC and advanced packaging markets while targeting a total addressable market exceeding $2 billion by 2027.

It continues to strengthen its portfolio with the Eagle G5 and Hawk systems, invest in AI-driven inspection software and integrate Visual Layer's AI technology to launch both standalone and hardware-integrated AI solutions. Strong demand across AI, HPC and advanced packaging, along with a resilient China business, is expected to support growth, particularly in the second half of 2026. For the second quarter of 2026, Camtek expects revenue between $129 million and $131 million, up sequentially. Importantly, management expects second-half 2026 revenue to grow more than 25% from first-half revenue. Such guidance indicates that customer shipments will accelerate meaningfully throughout the year as existing orders convert into revenue.

Image Source: Zacks Investment Research

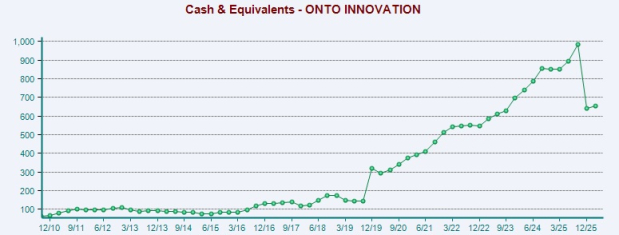

While China remains a healthy contributor, Camtek's growth is increasingly being driven by non-China markets. The company continues to expand opportunities in inspection, front-end applications, CMOS sensors, RF and photonics, supporting growth through 2027. Backed by its advanced technology, customized solutions, strong customer support and operational flexibility, Camtek is seeing solid adoption of its new systems and aims to further increase its market share across both 2D and 3D inspection markets. Its balance sheet continues to be one of its key strengths. At the end of March 2026, CAMT held approximately $849.7 million in cash, deposits and marketable securities. It also generated $3.1 million in operating cash flow during the quarter despite increased investment activity.

However, Camtek faces near-term headwinds from rising operating expenses, supply-chain cost pressures and intense competition in China. While the company is implementing cost-reduction initiatives and expects margins to improve in the second half, these challenges could weigh on profitability in the near term. Moreover, a slowdown in AI-related semiconductor spending could hurt Camtek's growth, while macroeconomic, geopolitical and broader semiconductor industry disruptions across global markets could further weigh on its business and financial performance.

The Case for ONTO Stock

Onto Innovation relies on a larger addressable market, diversified revenue streams, broad customer relationships, and multiple product categories. Onto delivered a stronger-than-expected first quarter, driven by robust AI-based demand across advanced nodes and advanced packaging, prompting management to raise its 2026 outlook. It now expects revenue to grow over 30% this year and aims for an operating margin above 30% by the fourth quarter. Growth is supported by Dragonfly G5 qualifications, increasing adoption of advanced packaging—such as 3D integration and panel-level packaging—and the planned $710 million investment for a 27% stake in Rigaku, which is expected to expand its process-control portfolio through X-ray software and long-term hybrid metrology opportunities.

ONTO continues to strengthen its growth outlook through new product adoption and expanding AI-driven demand. The Dragonfly G5 has secured qualification at a leading 2.5D logic customer, with shipments ramping through 2026, while the Atlas G6 is gaining traction across logic and memory applications, supported by new opportunities such as TSV metrology. Rapid adoption of advanced packaging technologies, including smaller, denser bumps, panel-level packaging and silicon photonics, is expected to drive strong growth, alongside a NAND market recovery. With increasing customer pull-ins and robust demand from new fabs, ONTO expects to outpace wafer fab equipment market growth in 2027.

Furthermore, Onto Innovation's planned acquisition of a 27% stake in Rigaku is expected to strengthen its process-control portfolio through AI Diffract software licensing, hybrid optical-X-ray metrology solutions and dividend income. The partnership complements ONTO's focus on the semiconductor market, while expanding its customer base through Gen 5 products and growing demand for advanced packaging. Innovations such as the Atlas TSV application have been developed independently, further enhancing the company's growth prospects.

Image Source: Zacks Investment Research

In addition, Onto Innovation maintains a strong balance sheet with $654.2 million in cash and investments, no long-term debt and positive operating cash flow at March-end. This financial strength provides the flexibility to fund strategic investments, including the Rigaku stake, while supporting growth opportunities tied to AI, advanced packaging and next-generation semiconductor manufacturing.

Share Price Movement for ONTO & CAMT

In the past six months, ONTO stock has surged 39.6% while CAMT has declined 5.3%.

Image Source: Zacks Investment Research

Valuation Comparisons

Both companies trade at premium valuations, Onto Innovation for its diversified business, larger market presence and consistent execution, while Camtek commands a premium driven by its stronger expected growth prospects.

In terms of forward price/earnings, ONTO shares are trading at 35.11X, lower than CAMT’s 37.62X.

Image Source: Zacks Investment Research

How the Zacks Consensus Estimate Compares for ONTO & CAMT

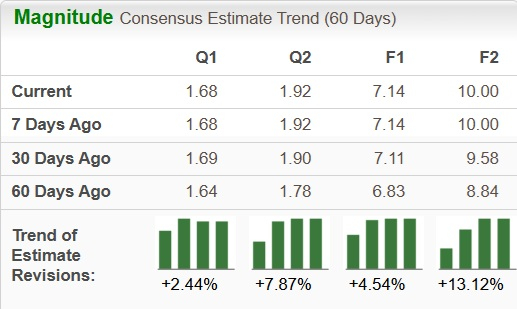

Earnings estimates for ONTO have moved up for both 2026 and 2027 over the past 60 days.

Image Source: Zacks Investment Research

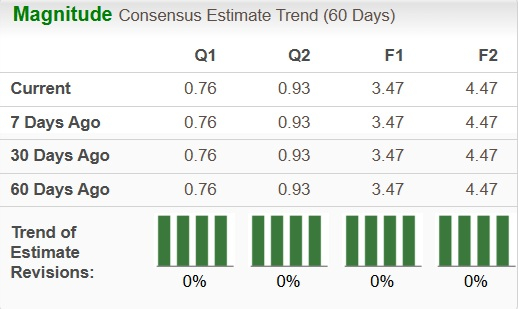

For CAMT, there is no estimate revisions.

Image Source: Zacks Investment Research

ONTO or CAMT: Which Stock to Buy?

Both Onto Innovation and Camtek are well-positioned to benefit from the increasing need for sophisticated inspection and metrology solutions. Camtek offers greater upside due to its exposure to advanced packaging, one of the fastest-growing segments of semiconductor manufacturing. However, ONTO stands out as the stronger all-around investment. Its diversified product portfolio, broad customer base, exposure across multiple semiconductor manufacturing stages and balanced participation in AI, memory and packaging markets provide a more resilient foundation for long-term growth. For investors seeking a combination of durable growth, profitability and resilience, Onto Innovation appears to be the better buy.

ONTO, at present, flaunts a Zacks Rank #1 (Strong Buy) while CAMT has a Zacks Rank #3 (Hold). Consequently, in terms of Zacks Rank and valuations, ONTO is a better investment option than CAMT. You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Camtek Ltd. (CAMT): Free Stock Analysis Report

Onto Innovation Inc. (ONTO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).