Shopify SHOP shares have declined 22.5% year to date (YTD) in contrast to the broader Zacks Computer and Technology sector’s appreciation of 17%. The underperformance can be attributed to slowing forward growth expectations and concerns about the cost of sustaining its AI-led expansion. However, Shopify’s prospects are expected to benefit from AI-driven commerce, strong merchant engagement, rising payments penetration, an expanding enterprise clientele and international footprint. So, does the pullback offer a buying opportunity for investors? Let’s find out.

SHOP’s Q2 Guidance Implies Deceleration

Shopify expects second-quarter 2026 revenue growth in the high-20% range, implying a meaningful sequential slowdown. The company reported first-quarter 2026 revenues of $3.17 billion, which jumped 34% year over year, while Gross Merchandise Volume (GMV) increased 35% year over year to $100.7 billion.

Shopify expects second-quarter gross profit to grow in the mid-20% range, slower than revenues. Gross profit is suffering from higher lower margin Merchant Solutions revenues, which currently account for almost 75% of Shopify’s revenues. Shopify’s Merchant Solutions business is benefiting from strong adoption of Payments, Capital and transaction services, which, however, carry lower gross margins than Subscription Solutions due to payment-processing and third-party expenses.

The company’s profitability prospect is suffering from higher AI infrastructure related costs as Shopify continues to invest heavily in Sidekick, AI commerce infrastructure and internal AI tools. Shopify management stated that in the first quarter of 2026, support efficiencies and economies of scale were partly offset by higher large-language-model expenses, particularly from Sidekick. SHOP expects this pressure to continue in the near term.

SHOP Shares Are Overvalued

Shopify is significantly overvalued, as suggested by a Value Score of F. In terms of the forward 12-month price/sales (P/S), SHOP is currently trading at 9.83X compared with the broader sector’s 6.98X. Shopify shares are pricey compared with Amazon AMZN, Wix.com WIX and Commerce.com CMRC. Shares of Amazon, Wix.com and Commerce.com are trading at P/S multiples of 3.01, 1.27 and 0.73, respectively.

SHOP Stock’s Valuation

Image Source: Zacks Investment Research

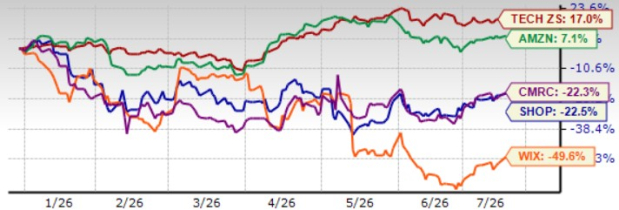

In terms of share price performance, Shopify has underperformed Wix.com YTD but lags Amazon and Wix.com. While Amazon shares returned 7.1%, Wix.com and Commerce.com dropped 49.6% and 22.3%, respectively.

SHOP Stock’s Price Performance

Image Source: Zacks Investment Research

Amazon’s services, such as Buy with Prime, Amazon Multi-Channel Fulfillment (MCF) and Amazon Pay, enable merchants to sell both on and off Amazon while leveraging its fulfillment network and checkout technology. Wix competes with Shopify by providing an all-in-one platform that combines website creation, online stores, payments, booking, marketing and AI-powered business tools. Commerce.com offers cloud-based software for building online stores, managing product catalogs, processing payments, supporting omnichannel selling and serving both B2C and B2B merchants.

SHOP to Ride on AI Push & Payments Penetration

Shopify is positioning itself as infrastructure for AI-driven commerce through Shopify Catalog and the Universal Commerce Protocol (UCP), which it co-developed with Google. Catalog distributes structured, real-time product information across ChatGPT, Microsoft Copilot, Google services and other AI surfaces, while UCP supports the entire journey from discovery through checkout. AI-driven traffic to Shopify stores increased eightfold in the first quarter, while orders originating from AI-powered searches rose nearly 13-fold. Shopify also says Catalog-powered AI searches convert at twice the rate of searches based on scraped data.

Meanwhile, weekly active shops using Sidekick increased roughly fourfold year over year. Merchants created more than 12,000 custom apps with Sidekick during the quarter, and nearly half of the newly generated Shopify Flow automations were built through the assistant. The Spring ’26 Edition expands Sidekick through proactive recommendations, mobile and voice access, and integrations with third-party applications such as Klaviyo, Loop and Yotpo.

Growing payment penetration is a key catalyst for Shopify. Shopify Payments processed $67 billion in first-quarter GMV, up 41%, and its penetration increased three percentage points to 67%. Management sees further upside from deeper usage across existing markets, adoption in recently launched European countries and Mexico, expansion beyond the current 39 markets, and continued Shop Pay momentum. Shop Pay processed $35 billion of GMV in the first quarter, up 59% year over year, including growth of more than 70% outside the United States. Shopify is also opening Shop Pay to brands that do not operate on Shopify, potentially extending the checkout product to a broader addressable market and more than 250 million shoppers.

International GMV increased 45% in the first quarter, including European GMV growth of 48%, or 35% at constant currency. Shopify is expanding local payment options, merchant billing currencies, capital availability and market-specific recommendations. Continued localization could help Shopify capture more of the commerce opportunity outside North America.

SHOP’s Earnings Estimates Revisions Are Positive

The Zacks Consensus Estimate for SHOP’s second-quarter earnings is currently pegged at 39 cents per share, unchanged over the past 30 days and indicating year-over-year growth of 11.43%.

Shopify Inc. Price and Consensus

Shopify Inc. price-consensus-chart | Shopify Inc. Quote

The Zacks Consensus Estimate for SHOP’s 2026 earnings is currently pegged at $1.84 per share, up a couple of cents over the past 30 days and indicating year-over-year growth of 57.26%.

Conclusion

Despite near-term concerns over slowing growth, margin pressure from AI investments and an outstretched valuation, Shopify’s long-term fundamentals remain compelling. AI-powered commerce, rising payments penetration, expanding international operations and growing enterprise adoption provide meaningful growth drivers. Positive earnings estimate revisions further reinforce confidence. While valuation limits near-term upside, the recent pullback could offer a buying opportunity for long-term investors willing to look beyond temporary profitability pressures and execution risks.

Shopify currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Shopify Inc. (SHOP): Free Stock Analysis Report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Wix.com Ltd. (WIX): Free Stock Analysis Report

Commerce.com, Inc. (CMRC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).