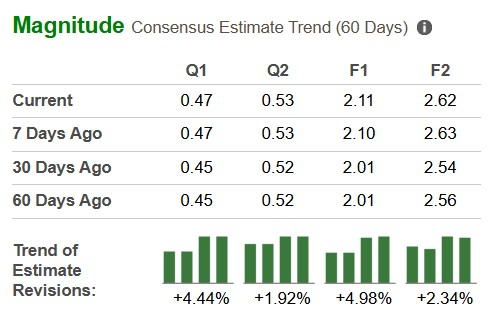

Tesla TSLA is slated to release second-quarter 2026 results on July 22, after market close. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings and revenues is pegged at 47 cents per share and $24.7 billion, respectively.

The earnings estimate for the to-be-reported quarter has been revised upward by 2 cents over the past 30 days. The bottom-line projection indicates year-over-year growth of 17.5%. The Zacks Consensus Estimate for quarterly revenues suggests year-over-year growth of 10%.

For full-year 2026, the Zacks Consensus Estimate for TSLA’s revenues is pegged at $102 billion, implying a rise of 7.6% year over year. The consensus mark for 2026 EPS is pegged at $2.11, suggesting an uptick of around 27% on a year-over-year basis.

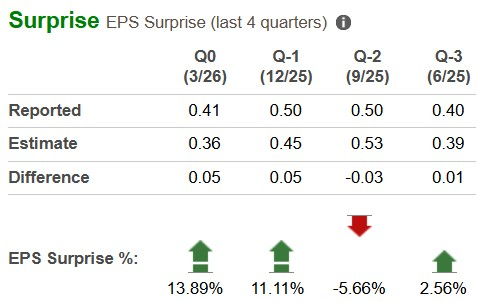

In the trailing four quarters, this electric vehicle (EV) and technology giant topped EPS estimates on three occasions and missed once, with the average negative earnings surprise being 5.48%.

Earnings Whispers for TSLA

Our proprietary model predicts an earnings beat for Tesla this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. That’s the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

TSLA has an Earnings ESP of +16.52% and a Zacks Rank #3.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Shaping Tesla’s Q2 Results

In the second quarter, Tesla delivered 480,126 vehicles (including 467,762 Model 3/Y and 12,364 other models), beating our model estimate of 400,133 units. Deliveries increased 34% sequentially and 25% on a year-over-year basis. It was Tesla’s strongest quarter for EV sales since the third quarter of 2025. Back then, sales got a similar lift when U.S. buyers rushed to purchase before federal EV tax credits expired, prompting Tesla and other automakers to see a temporary surge in demand.

Second-quarter deliveries were largely driven by high gas prices amid the Middle East conflict, which likely pushed consumers toward EVs. Demand trends strengthened across key international markets like Europe and China.Although Tesla doesn’t break down sales by region, Europe was a key catalyst, where sales momentum has been robust in recent months. In China, where Tesla commands a huge presence, retail deliveries rebounded strongly in May, snapping a two-month run of year-over-year sales declines. Despite softer U.S. demand, robust international performance helped offset the weakness.

Tesla’s smaller pure-play EV peers—Rivian Automotive RIVN and Lucid Group LCID—came up with contrasting second-quarter delivery reports. While Rivian delivered 12,194 vehicles, topping estimates and its own prior guidance, Lucid fell short of expectations, delivering just 3,953 vehicles.

Coming back to Tesla, we expect the company’s automotive revenues and gross margins to improve year over year on the back of strong deliveries. We forecast second-quarter total automotive revenues and gross margins at $17 billion (up over 2% year over year) and $3.2 billion (up 11% year over year).

The company’s energy business revenues are also expected to increase as Tesla deployed 13.5 GWh of energy storage in the second quarter, reflecting an uptick of 53% and 40% on a sequential and year-over-year basis, respectively. The number also came ahead of our model projection of 12.66 GWh. The outperformance was driven by stronger-than-expected demand for Megapack and Powerwall.

Tesla Price Performance & Valuation

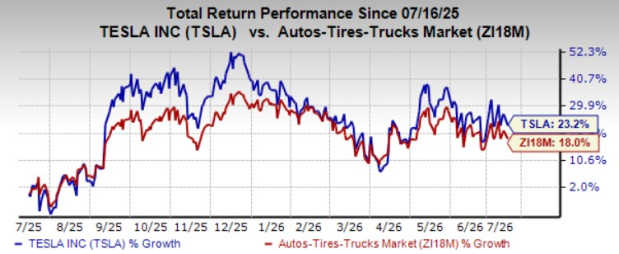

Over the past year, shares of Tesla have risen 23%, outperforming the industry.

Tesla stock is quite overvalued. Going by its price/sales ratio, the company is trading at a forward sales multiple of 13.68, way higher than the industry as well as its own 5-year average.

How to Play TSLA Stock Now

Yes, Tesla's delivery trends are improving, but deliveries are no longer the company's central growth story. Its energy storage business is also performing well, though it still accounts for a relatively small portion of overall revenues.

Tesla has aggressively pivoted toward autonomous vehicles (AVs) and artificial intelligence (AI). The problem is these are long-cycle bets with uncertain timelines. The company operates unsupervised robotaxi service in Austin, Dallas, Houston and Miami and supervised service in the San Fransico Bay Area. Still, it has a lot of catching up to do with Alphabet’s GOOGL Waymo, which is the frontrunner in this space. CEO Elon Musk has already pushed back the robotaxi timeline. The story with Optimus is also not much different. On the first-quarter earnings call, Musk admitted production will be “quite slow” and said it’s “literally impossible to predict” output this year.

On top of that, Tesla lifted its 2026 capital expenditure forecast from $20 billion to $25 billion. Management has warned that free cash flow could turn negative as it ramps up spending on AI and autonomous-driving initiatives.

Tesla does possess a powerful brand, industry-leading technology capabilities, and multiple long-term growth platforms. Tesla’s next chapter could be transformational, but it is capital-intensive, high-risk, and likely years away from delivering material financial returns. Until then, execution and valuation risks remain concerning. As such, from a broader perspective, this may not be the right entry point for new investors, even if Tesla beats second-quarter earnings expectations.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Tesla, Inc. (TSLA): Free Stock Analysis Report

Alphabet Inc. (GOOGL): Free Stock Analysis Report

Lucid Group, Inc. (LCID): Free Stock Analysis Report

Rivian Automotive, Inc. (RIVN): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).