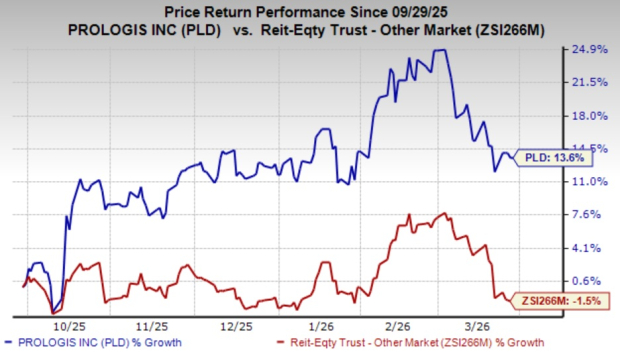

Shares of Prologis PLD have rallied 13.6% in the past six months against the industry’s decline of 1.5%. Analysts seem bullish on this Zacks Rank #3 (Hold) company. The Zacks Consensus Estimate for its 2026 FFO per share has moved marginally northward over the past two months to $6.14.

This industrial REIT is poised to gain from its scale and strategically located modern distribution facilities in key markets globally. Prudent buyouts, development and a healthy balance sheet will drive growth. The company is also converting some of its warehouses into data centers to capitalize on the growing opportunity in this asset category.

However, amid macroeconomic uncertainty, customers remain focused on cost controls and delay their decision-making with respect to leasing. Elevated interest expenses add to PLD’s concerns.

Image Source: Zacks Investment Research

Let’s delve deeper and find out what’s in favor of this stock and what’s not.

What’s Aiding Prologis Stock?

Prologis manages one of the largest industrial real estate portfolios globally, focusing on high-density, supply-constrained markets near key transportation hubs. These strategic locations enable efficient logistics and continue to drive strong tenant demand. In the fourth quarter of 2025, the company reported a retention rate of 77.7% and an average occupancy of 95.3%. For 2026, management expects occupancy to remain stable within 94.75–95.75%, with leasing activity supporting future rental income growth.

The company is also expanding through acquisitions and development in high-barrier markets. In 2025, Prologis completed $1.71 billion in acquisitions and initiated $2.96 billion in development projects, with 61.1% classified as build-to-suit. Looking ahead to 2026, acquisitions are projected between $1.00 billion and $1.50 billion, while development starts are expected to range from $3.00 billion to $4.00 billion.

Build-to-suit projects remain a key growth driver. In the fourth quarter of 2025, development starts reached $1.02 billion, with nearly half allocated to such projects. These developments reflect strong demand from large, multi-site customers, particularly in e-commerce. Many of these facilities are located near major population centers, supporting last-mile delivery. In March 2026, Prologis partnered with GIC to form a $1.6 billion joint venture focused on build-to-suit logistics assets across major U.S. markets.

Prologis is also tapping into the rapidly growing data center sector, fueled by demand for cloud computing, artificial intelligence and big data infrastructure. The company is exploring both warehouse conversions and new developments to capture this opportunity.

Financially, Prologis remains well-positioned. As of the fourth quarter of 2025, liquidity stood at $7.6 billion, with a low weighted average interest rate of 3.3% and an average debt maturity of 8.2 years. Strong credit ratings, A2 from Moody’s and A from S&P, help keep borrowing costs low. The company also continues to reward shareholders, raising its quarterly dividend by 5.9% in February 2026 to $1.07 per share, reflecting consistent growth and a sustainable payout outlook. In the last five years, Prologis has increased its dividend five times, and its five-year annualized dividend growth rate is 11.58%. Check Prologis’ dividend history here.

What’s Hurting Prologis Stock?

Amid macroeconomic uncertainty and geopolitical concerns, some customers still remain focused on cost controls and are delaying their decisions with respect to leasing. As such, demand remains subdued in some markets and is expected to continue in the near term. Moreover, Prologis’ business is tied to global trade flows. Any slowdown in imports, retail demand or industrial production is likely to hamper revenue growth.

Prologis has a substantial debt burden, and its consolidated debt as of Dec. 31, 2025, was $35.04 billion. With a high level of debt, interest expenses are likely to remain elevated. In the fourth quarter of 2025, interest expenses jumped 12.2% on a year-over-year basis to $260.5 million.

Stocks to Consider

Some better-ranked stocks from the broader REIT sector are Chatham Lodging Trust REIT CLDT, sporting a Zacks Rank #1 (Strong Buy), and Terreno Realty TRNO, carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Chatham Lodging’s 2026 FFO per share is pegged at $1.20, which indicates year-over-year growth of 17.7%.

The consensus estimate for Terreno Realty’s full-year FFO per share is pinned at $2.79, which implies a marginal increase from the year-ago period.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO), a widely used metric to gauge the performance of REITs.

Just Released: Zacks Top 10 Stocks for 2026

Hurry – you can still get in early on our 10 top tickers for 2026. Handpicked by Zacks Director of Research Sheraz Mian, this portfolio has been stunningly and consistently successful.

From inception in 2012 through November, 2025, the Zacks Top 10 Stocks gained +2,530.8%, more than QUADRUPLING the S&P 500’s +570.3%.

Sheraz has combed through 4,400 companies covered by the Zacks Rank and handpicked the best 10 to buy and hold in 2026. You can still be among the first to see these just-released stocks with enormous potential.

See New Top 10 Stocks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Prologis, Inc. (PLD): Free Stock Analysis Report

Terreno Realty Corporation (TRNO): Free Stock Analysis Report

Chatham Lodging Trust (REIT) (CLDT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).