Amazon (AMZN) is steadily positioning itself as a significant player in the artificial intelligence (AI) infrastructure market, and a key driver of that momentum is the company’s rapidly expanding in-house chip business.

During its fourth-quarter earnings call, Amazon’s management highlighted that the company’s internally developed chips have already become a meaningful contributor to its financial performance. Custom processors such as Graviton and Trainium are gaining traction within Amazon Web Services (AWS), helping power the growing demand for cloud computing and AI workloads.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

According to management, the combined annual revenue run rate from these chips surpassed $10 billion and continues to grow at triple-digit rates.

www.barchart.com

www.barchart.com The True Scale of Amazon’s Chip Business May Be Much Larger

Amazon recently provided additional insight into the scale of its custom silicon business in its shareholder letter. The company revealed that the broader chip portfolio, which includes Graviton, Trainium, and Nitro, the networking chip used in its EC2 cloud infrastructure, has now exceeded a $20 billion annual revenue run rate.

Even that figure may understate the business's true economic value. At present, Amazon largely monetizes its chips internally through AWS rather than selling them directly in the open market. Management noted that if it sold the chips directly to AWS and other customers, the annual revenue run rate could approach $50 billion.

Moreover, its own chip platform provides the company with important strategic advantages, including stronger cost control and greater efficiency across its cloud infrastructure.

Amazon believes its AI chips could play an important role in improving the economics of large-scale AI workloads. As these chips are deployed more widely across AWS, the company expects them to generate substantial financial benefits.

Management estimates that Trainium could significantly reduce capital expenditures. In addition, Amazon expects notable improvement in operating margin as inference workloads shift toward its internally designed processors.

Heavy AI Investments Are Raising Questions

Despite the strong growth of Amazon’s AI chip business, investors have expressed concern about the company’s rising capital expenditures. During the fourth-quarter conference call, management disclosed plans to invest approximately $200 billion in capital expenditures through 2026.

Most of that spending will be directed toward expanding AWS infrastructure and strengthening Amazon’s AI capabilities. The scale of the investment has raised questions among investors about near-term profitability and free cash flow.

However, Amazon’s leadership emphasized that much of the planned spending is supported by customer commitments, which helps reduce uncertainty around the investment cycle. As an example, the company pointed to a recently announced commitment from OpenAI valued at more than $100 billion. Management also noted that several additional agreements have already been completed, remain unannounced, or are currently in advanced stages of negotiation.

AI Demand to Drive AWS Growth

Amazon expects adoption of AWS to continue accelerating as companies deploy both traditional computing and AI workloads in the cloud. Management emphasized that the company is currently monetizing new infrastructure capacity as quickly as it can deploy it. This suggests that the current investment is being driven primarily by customer demand.

Moreover, Amazon noted that it already has customer commitments covering a substantial share of future capacity, which provides visibility into long-term demand.

AMZN’s Long-Term Prospects Remain Solid

While higher capital expenditures may place pressure on margins in the near term, these investments are essential to capturing the rapidly expanding opportunities in cloud computing and AI. While increased spending will hurt free cash flow in the short term, it could generate substantial free cash flow over the medium to long term.

As AWS continues to scale and Amazon’s proprietary silicon becomes more deeply embedded in the AI ecosystem, the company’s chip business could evolve into one of the most important drivers of value creation for AMZN.

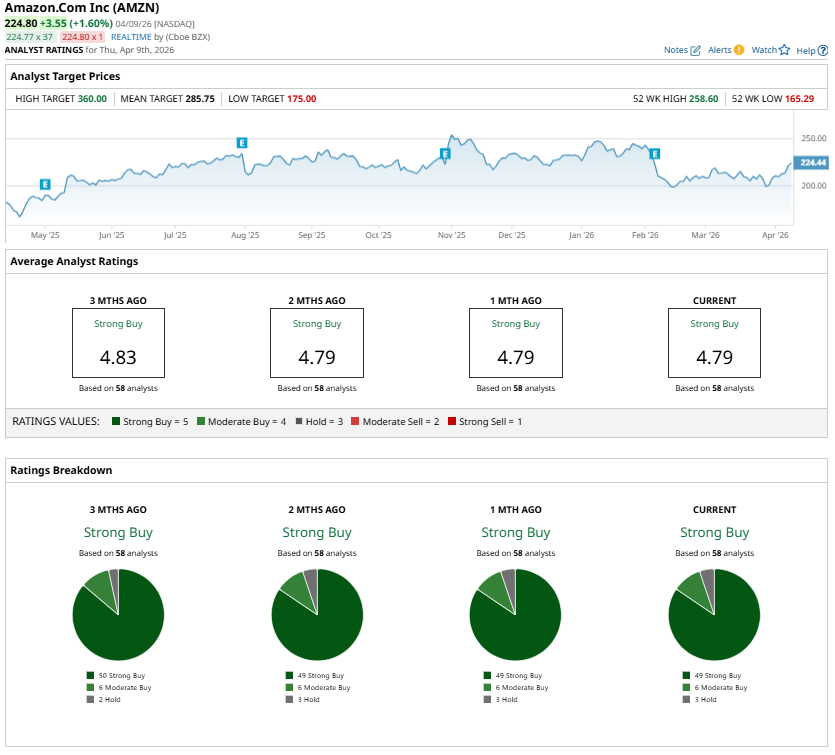

Reflecting these prospects, Wall Street remains broadly optimistic about Amazon’s outlook. AMZN stock currently carries a “Strong Buy” consensus rating.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Amazon’s AI Chip Business Is Surging—And It Could Be a Major Catalyst for AMZN Stock Intel Pivots from ‘Dead Money’ to ‘Hot Stock’: Should You Too Buy INTC Stock Here? Intel Stock Just Hit a New 52-Week High. Should You Chase the Rally Here? Dear UnitedHealth Stock Fans, Mark Your Calendars for April 21