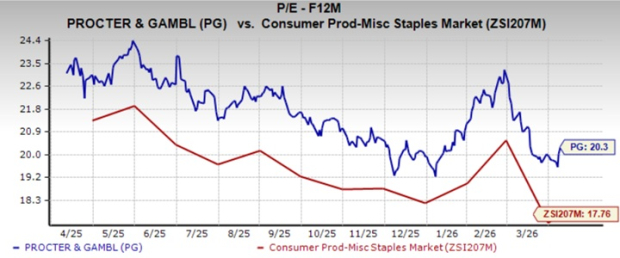

The Procter & Gamble Company PG has been gaining by leveraging its solid market position and focusing on productivity and cost-efficiency. However, its current forward 12-month price-to-earnings (P/E) ratio of 20.3X raises questions about whether the stock is fairly valued. This multiple is significantly higher than the Zacks Consumer Products – Staples industry average of 17.76X, making the stock appear relatively expensive.

The price-to-sales (P/S) ratio of Procter & Gamble, a distinguished name in the consumer staples sector, is 3.85X, above the industry’s multiple of 2.19X. This adds to investor unease, especially considering its Value Score of D, which suggests that it may not be a strong value proposition at current levels.

Image Source: Zacks Investment Research

PG’s Premium Valuation Surpasses Peers

At 20.3X P/E, Procter & Gamble is trading at a valuation much higher than its competitors. The company’s peers like The Clorox Company CLX, Unilever PLC UL and Albertsons Companies, Inc. ACI have experienced declines and are delivering solid growth and trade at more reasonable multiples. Clorox, Unilever and Albertsons Companies have forward 12-month P/E ratios of 16.07X, 15.85X and 0.12X — all significantly lower than that of PG. At such levels, Procter & Gamble’s valuation seems out of step with its growth trajectory.

The PG stock’s premium valuation suggests that investors have strong expectations for its growth. However, the stock currently seems somewhat overvalued. Procter & Gamble’s ability to meet or exceed these lofty expectations is crucial in justifying its premium pricing.

In the past three months, the company’s shares have risen 3.4%, against the broader industry’s decline of 0.4%. The company has outperformed the Zacks Consumer Staples sector and the S&P 500’s declines of 3.5% and 3%, respectively.

Procter & Gamble’s performance is better than that of its competitors, including Clorox’s 1.4% growth and Unilever’s 8.9% decline in the past three months. However, PG has underperformed Albertsons Companies, which rose 4.9% in the same period.

PG’s current share price of $146.66 trades 14.6% below its recent 52-week high mark of $171.65. The stock trades 6.6% above its 52-week low of $137.62.

Procter & Gamble trades below its 50 and 200-day moving averages, indicating bearish sentiment. The moving average is an important indicator for gauging market trends and momentum.

Procter & Gamble Trades Below 50 & 200-Day SMA

Image Source: Zacks Investment Research

PG’s Growth Drivers vs. Market Challenges

Procter & Gamble’s growth strategy is centered on innovation, brand superiority and geographic expansion, but near-term performance remains constrained by softer consumer demand and competitive pressures. Management highlighted that growth outside the United States remains encouraging, with most regions delivering organic sales gains and benefiting from targeted innovation and improved execution.

The company is leaning on consumer-insight-driven product launches, such as premium Baby Care and fabric enhancer innovations, alongside stronger brand communication and in-store execution to drive category growth and share gains. These initiatives, supported by productivity improvements and reinvestment in innovation, are expected to fuel stronger performance in the second half of fiscal 2026.

PG is also advancing a longer-term reinvention strategy built on superior data, AI-enabled innovation and deeper integration with retail partners. Management emphasized leveraging extensive consumer data, advanced R&D capabilities and supply-chain platforms to accelerate product development and enhance marketing effectiveness across channels. The company aims to strengthen brand engagement across fragmented media platforms while improving value propositions to drive household penetration and usage growth.

However, the growth outlook is tempered by persistent market challenges. Consumer spending remains pressured by inflation across essential categories, while media fragmentation and evolving retail dynamics complicate brand building. Usage growth has been slow, with volume trends largely flat in key markets, reflecting cautious consumer behavior and reliance on pricing-led growth in recent years.

Additionally, aggressive competition, geopolitical uncertainty and tariff-related cost headwinds are expected to weigh on margins and limit near-term acceleration. Despite these hurdles, PG expects innovation-led interventions and improved execution to gradually restore growth momentum.

PG’s Estimate Revision Trend

The Zacks Consensus Estimate for Procter & Gamble’s fiscal 2026 EPS has been unchanged in the past 30 days. Meanwhile, the consensus mark for EPS has moved down 0.3% in the past seven days. However, revenue and EPS estimates for fiscal 2026 and 2027 indicate year-over-year growth.

For fiscal 2026, the Zacks Consensus Estimate for PG’s revenues and EPS implies year-over-year growth of 2.9% and 2.1%, respectively. The consensus mark for fiscal 2027 revenues and EPS indicates 2.6% and 4.5% year-over-year rallies, respectively.

Image Source: Zacks Investment Research

Is Procter & Gamble a Lucrative Buy Now?

Procter & Gamble remains a high-quality consumer staples name, backed by strong brands, innovation and productivity initiatives. Its reinvention strategy and international growth opportunities support long-term prospects. However, soft demand, flat volume trends and competitive pressures continue to weigh on near-term performance.

The stock’s premium valuation, with elevated P/E and P/S multiples versus peers, suggests much of the optimism is already priced in. Earnings growth expectations remain modest, limiting upside potential. While PG remains a solid long-term compounder, near-term investors may stay cautious. Existing shareholders may consider retaining this Zacks Rank #3 (Hold) stock in their portfolios, while awaiting clearer signs of earnings reacceleration. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Unilever PLC (UL): Free Stock Analysis Report

Procter & Gamble Company (The) (PG): Free Stock Analysis Report

Albertsons Companies, Inc. (ACI): Free Stock Analysis Report

The Clorox Company (CLX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).