Tesla TSLA has long been the poster child of the electric vehicle (EV) revolution. But as competition intensifies, its dominance is no longer unquestioned. The company’s global EV leadership was first challenged by BYD Co Ltd BYDDY in the fourth quarter of 2023, and by 2025, BYD had overtaken Tesla on an annual basis for the first time.

While Tesla’s start to 2026 wasn’t particularly strong, it did manage to edge past BYD in first-quarter EV deliveries and reclaim the top spot. That said, Tesla deliveries came in below expectations, highlighting ongoing demand challenges.

Importantly, neither player is on a completely solid footing. Tesla continues to grapple with slowing growth and margin pressures in the EV business and is pivoting toward autonomous driving and artificial intelligence (AI) as its next growth engines. Meanwhile, BYD is also facing profitability pressures, with net profit declining in 2025 for the first time since 2021. The company is focused on accelerating global expansion and sharpening its competitive positioning.

With both EV giants navigating a more complex phase, let's take a closer look to find out which stock is better placed today and is either worth buying at all.

The Case for Tesla

Tesla’s near-term outlook remains muted as its core EV business loses momentum. First-quarter deliveries came in at 358,023 units, missing expectations and declining sequentially from the previous quarter. While volumes were slightly higher year over year, the broader trend is concerning—deliveries have now fallen for two straight years, with the decline accelerating from about 1% in 2024 to more than 8% in 2025. An aging vehicle lineup, limited new launches, intensifying competition and the withdrawal of the $7,500 federal tax credit are weighing on demand.

To offset this slowdown, Tesla is pivoting aggressively toward autonomous vehicles (AVs) and AI. However, these remain long-cycle bets with uncertain timelines. The company has begun rolling out its robotaxi service in select U.S. cities, but its technology is still at Level 2 autonomy, requiring driver supervision. In contrast, rivals like Waymo are already operating Level 4 systems in multiple cities, underscoring a meaningful gap in both capability and scale.

At the same time, Tesla is ramping up spending. Capital expenditures are expected to exceed $20 billion in 2026, funding AI infrastructure and new facilities. This comes at a time when the core business is slowing, raising concerns about near-term returns and execution risk.

One clear bright spot is Tesla’s energy division. Its Energy Generation and Storage segment continues to see strong demand for products like Megapack and Powerwall, with deployments growing rapidly and margins outperforming the auto business.

Overall, while Tesla’s long-term vision remains compelling, the combination of slowing EV momentum, rising competition and heavy investment tilts the near-term risk-reward balance toward caution.

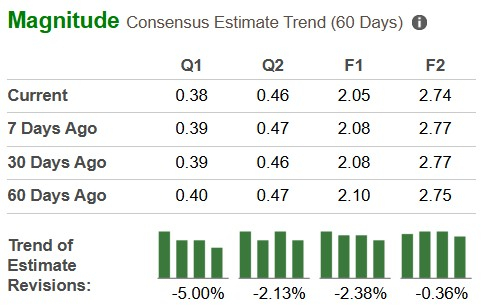

The Zacks Consensus Estimate for TSLA’s EPS has moved south over the past 60 days.

The Case for BYD

BYD is facing a tough operating environment as growth in its core market slows and policy support weakens in China. In the first quarter, the company’s pure EV sales declined 25% year over year to 310,389 units, while total new-energy vehicle (NEV) volumes dropped 30%, reflecting softer demand in China. Reduced subsidies and the reintroduction of purchase taxes have made EVs less attractive for buyers, directly impacting volumes.

Profitability is also declining. BYD reported a 19% drop in net profit for 2025, with margins pressured by intense price competition. Revenue growth slowed to its weakest pace in six years, and profits have declined for three consecutive quarters. The domestic market, once a key strength, is now a source of volatility.

Yet, BYD’s long-term positioning appears stable for now. The company is aggressively expanding overseas, with exports emerging as a key growth driver. It crossed 1 million export vehicles in 2025 and is targeting 1.5 million exports by 2026, signaling a strategic pivot beyond China. This global push could help offset domestic headwinds and diversify revenue streams.

A major competitive advantage lies in BYD’s vertical integration. The company produces around 80% of its components in-house, including batteries and semiconductors, enabling strong cost control. This gives BYD more flexibility to navigate price wars compared to its peers.At the same time, BYD continues to invest in technology, with next-generation battery innovations and new model launches aimed at improving range, charging speed and overall competitiveness.

Overall, while BYD’s cost leadership and global expansion offer structural support, near-term pressures on demand and margins continue to cloud the outlook.

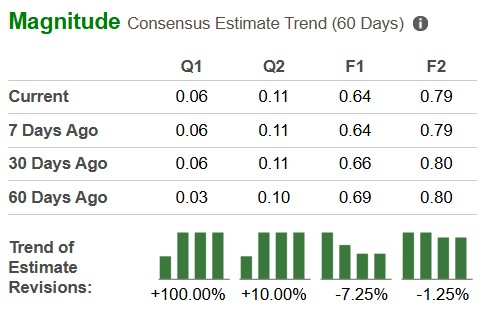

Near-term earnings visibility remains mixed, with the Zacks Consensus Estimate for quarterly EPS moving up but annual estimates trending lower over the past 60 days.

Price & Valuation Check

Tesla shares have declined year to date, while BYD stock has gained over the same period.

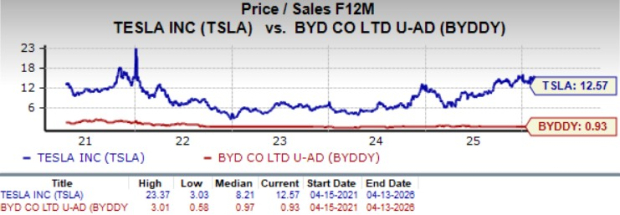

Based on its price/sales ratio, Tesla is trading at a forward sales multiple of 12.57, way higher than BYD’s 0.93.

Final Thoughts

Neither Tesla nor BYD presents a compelling near-term investment case, as both face slowing momentum and rising execution risks. For now, a wait-and-see approach toward both stocks seems prudent.

However, BYD appears relatively better positioned at this stage. It has a more diversified vehicle lineup, its valuation is far more grounded, its cost structure offers resilience in a price-competitive market, and its global expansion strides provide a clearer, more tangible growth pathway.

Tesla, in contrast, is navigating a transition phase, with its core EV business weakening while future growth hinges on capital-intensive, longer-dated bets like AI and autonomy. With visibility still limited, the risk-reward profile remains skewed.

Both Tesla and BYD carry a Zacks Rank #3 (Hold).You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Tesla, Inc. (TSLA): Free Stock Analysis Report

Byd Co., Ltd. (BYDDY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).