The Oracle (ORCL) stock saga recently kicked back into the headlines after a report that OpenAI missed some internal targets sent shockwaves through tech. Shares of chip and AI names like Nvidia (NVDA) and Tesla (TSLA) dipped on the news, and Oracle wasn’t spared from the reaction. ORCL stock fell on fears that its big AI bet might be cooling.

However, Wedbush analyst Dan Ives called the drop an “overreaction.” Ives argues that demand at OpenAI and other cloud projects remains huge, and he urged investors to treat the selloff as a buying opportunity. In short, Ives believes investors should ignore the panic, as Oracle’s business is still humming along under the hood. Let's take a closer look.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About Oracle Stock

Oracle is a database and cloud giant that has grown into a tech powerhouse, selling enterprise software, servers, and cloud services. These days, its pitch is heavy on artificial intelligence.

Beyond that, Oracle is bulking up data centers to serve projects for Meta Platforms (META), Elon Musk’s xAI, OpenAI, and others. The company now mixes big databases with cloud AI, and has expanded multicloud deals with Amazon's (AMZN) AWS and Alphabet's (GOOGL) Google Cloud, letting customers run Oracle’s tech on rival clouds.

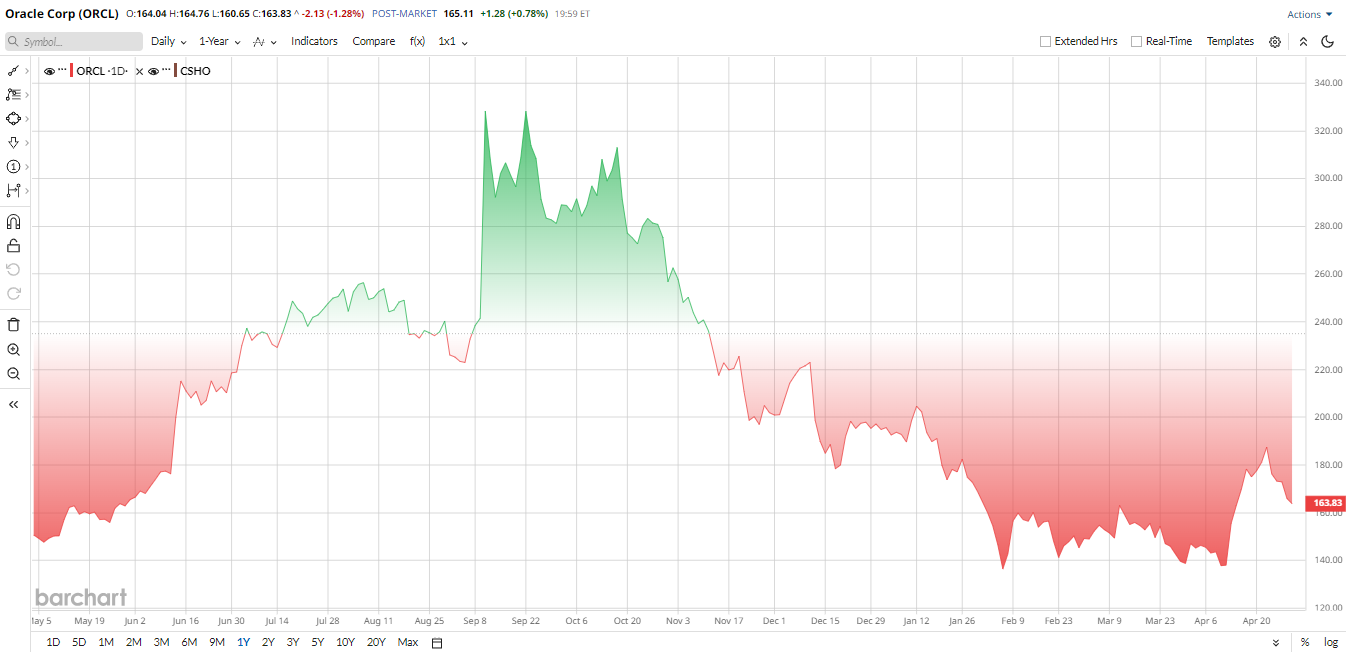

After a huge mid-2025 rally, ORCL stock has cooled off. Shares climbed to all-time highs near $346 last year on AI hype. Now, the stock is trading around $172, off roughly 50% from its peak. While Oracle is still up 17% over the past 52 weeks, the stock is down about 9% year-to-date (YTD). The slide reflects both a broader tech pullback and jitters over the company’s heavy spending.

Investors seem to be worried about Oracle's $50 billion data-center buildout and debt. Weaker smartphone demand has also trimmed revenue in its legacy hardware business. Still, ORCL stock is up significantly from two years ago. It has been a volatile ride, but the bulls see long-term growth under the surface.

On paper, Oracle isn’t cheap. It trades around 26.5 times forward earnings, while the price-to-sales ratio of about 8 times and price-to-book ratio of about 13.6 times are well above tech averages of roughly 4 times each. In other words, investors are paying up for Oracle’s cloud growth.

Still, there’s some justification, as Oracle’s earnings have been surging. While ORCL stock looks pricey on paper, the firm is also outperforming peers on growth.

www.barchart.com

www.barchart.com What Happened With OpenAI?

A flurry of news on OpenAI recently triggered a selloff in AI-linked stocks like Oracle. On April 27, reports emerged that OpenAI had fallen short of some internal user and revenue targets. Traders took this as a warning sign. Already down about 29% over the past six months, ORCL stock dropped more than 4% on April 28.

The fear was that Oracle — which has a massive backlog of contracts, including a $300 billion compute deal with OpenAI — might see weaker demand. But investors quickly remembered the big picture. Wedbush and others pointed out that OpenAI’s long-term growth is intact. Ives noted the “sky-high demand” for AI capacity and said Oracle’s backlog and deals are locked in.

In short, the Wedbush analyst sees the pullback as a short-term scare in a long-term bull market.

Oracle Reports Q3 Earnings

Oracle recently reported strong third-quarter results, beating market expectations as growth in its cloud business accelerated. Revenue for the quarter rose 22% year-over-year (YOY) to $17.19 billion, coming in above estimates. Cloud services and license revenue climbed 44% to $8.9 billion, helped by strong demand for cloud infrastructure. OCI revenue jumped 84% to $4.9 billion. Fusion applications and NetSuite also posted steady growth.

Net income was $3.7 billion, while adjusted net income rose about 23% to $5.2 billion. Adjusted EPS came in at $1.79, up about 21% YOY and above expectations.

The company continued to spend heavily on expansion. Operating cash flow was about $23.5 billion over the past year, but free cash flow was negative at around $24.7 billion as Oracle invested in data centers.

Oracle said remaining performance obligations, a measure of future revenue, rose 325% YOY to $553 billion, driven by large AI-related contracts.

For Q4, the company expects revenue growth of 19% to 21% and adjusted EPS of $1.96 to $2.00. Oracle maintained its full-year 2026 revenue forecast of about $67 billion and raised its fiscal 2027 revenue target to $90 billion.

Oracle's Recent Developments

Oracle has been busy with major initiatives in 2026, raising capital and restructuring. In early February, the company announced a plan to raise about $45 billion to 50 billion this year via debt and equity to fund its cloud expansion. Oracle has already locked in roughly $30 billion through bonds and convertible notes.

This has raised eyebrows, and some bondholders even sued, fearing dilution and more debt. Oracle also carried out massive layoffs this year, reportedly cutting thousands of jobs across various divisions as it streamlined costs.

On the partnership front, Oracle tied up with AWS in April to give customers a private, high-speed link between its cloud and Amazon’s cloud. The firm also deepened alliances with Microsoft (MSFT) Azure and Google Cloud for running Oracle databases.

Finally, on the hardware side, Oracle signed a deal to use Advanced Micro Devices' (AMD) new MI450 AI chips in its servers, deploying 50,000 of them by late 2026.

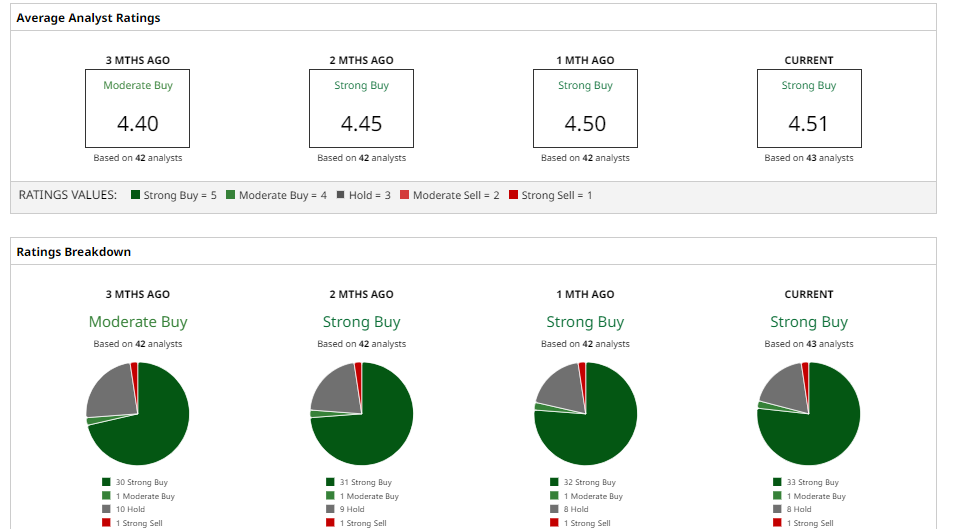

What Does Wall Street Think of ORCL Stock?

Wall Street analysts have mixed views on Oracle, reflected in a wide range of price targets.

As previously noted, Wedbush analyst Dan Ives is very bullish on ORCL stock. Ives initiated coverage with an “Outperform” rating and $225 target. Meanwhile, Morgan Stanley analyst Keith Weiss went the other way in April. Weiss kept an “Equal-Weight” rating on shares and trimmed his target to $207, warning of uncertainty around the costs and margins of Oracle’s new GPU-as-a-Service business.

Barclays recently raised its target to $240, saying the strong Q3 report helped alleviate concerns over infrastructure spending and margins. Bank of America analyst Tal Liani is also upbeat, resuming coverage in March with a “Buy” rating and $200 target, highlighting Oracle’s huge backlog of contracted revenue.

On balance, analyst sentiment is cautiously positive. ORCL stock has a consensus “Strong Buy” rating with an average price target of $247.43, which implies potential upside of 39% from current levels.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Ignore the OpenAI Panic and Keep Buying Oracle Stock, Says Wedbush FS KKR Corp, a Private Credit Fund, Sports a 16.6% Yield - Is FSK A Value Buy? Taiwan Semi Just Dumped Its Stake in ARM Stock. Why Investors Don’t Seem to Care. Amazon Stock Forecast: Could AI and Chips Make AMZN a $4 Trillion Company?