Argan, Inc.’s AGX fourth-quarter performance suggests that execution is becoming more than just an operating strength — it may be turning into a competitive moat. The company’s EBITDA rose to $56 million, up from $39.3 million a year earlier, while EBITDA margin expanded to 21.4% from 16.9%. That improvement came alongside a 25% gross margin, driven largely by the Power segment and the early substantial completion of the 950-MW Trumbull Energy Center.

The key takeaway is that Argan is not simply benefiting from higher demand; it is converting project execution into margin upside. Management said the margin improvement reflected “strong project execution,” especially at Trumbull, where finishing ahead of schedule helped avoid extra site costs. That matters in EPC construction, where delays, labor pressure and supply-chain issues can quickly erode profitability.

This execution edge also supports Argan’s ability to win and manage larger projects. The company ended fiscal 2026 with a $2.9 billion backlog, including $2.7 billion in Power segment backlog, and says only a handful of firms can build the large combined-cycle plants needed for AI, data centers and broader electrification demand.

Furthermore, Argan’s financial "bankability" serves as a strategic barrier to entry. With $895 million in cash and investments and no debt, the company provides customers with a reliable EPC partner in an industry where financial stability is critical for bonding and long-term infrastructure commitments. By maintaining a disciplined approach focusing on the "right projects with the right partners," Argan leverages its strong balance sheet and execution track record to secure high-value contracts while minimizing the risk of costly project overruns.

Argan’s Competitive Landscape

Argan operates in an increasingly competitive power and infrastructure market alongside major engineering and construction firms such as Jacobs Solutions Inc. J and EMCOR Group, Inc. EME, which are also benefiting from strong end-market demand and improved project execution.

Jacobs continues to benefit from its higher-margin consulting and program management model, which supports relatively stable profitability compared with more construction-intensive peers. In the first quarter of 2026, adjusted EBITDA increased 14% year over year to $255 million, while adjusted EBITDA margin expanded 90 basis points to 15.2%. Management attributed the improvement to disciplined project execution, portfolio optimization and increasing exposure to higher-value infrastructure, water and advanced manufacturing programs.

In comparison, EMCOR, meanwhile, delivered another quarter of strong profitability driven by a favorable project mix and disciplined execution across its Electrical Construction and Mechanical Services operations. In the first quarter of 2026, revenues increased 12.7% year over year to $4.1 billion, while operating income rose 21.6% to $373 million. Operating margin expanded 70 basis points to 9.1%, supported by continued strength in technically complex projects tied to data centers, healthcare, institutional and industrial markets.

Compared with peers, Argan’s profitability profile highlights the benefits of its highly specialized focus on large-scale natural gas power projects and disciplined project selection strategy. As demand tied to electrification, AI-driven data centers and grid reliability continues to rise, the company’s execution consistency is increasingly emerging as a key competitive differentiator.

AGX Stock’s Price Performance & Valuation Trend

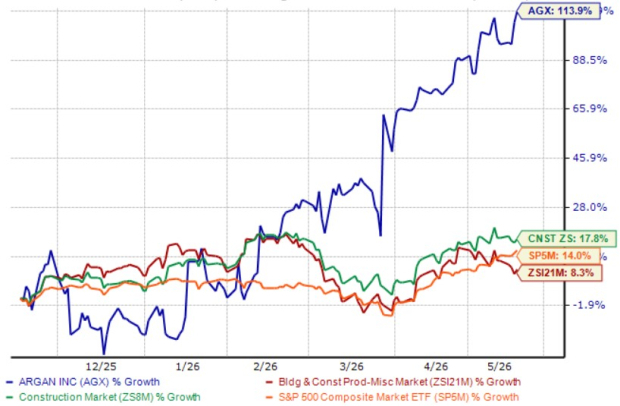

Shares of this global provider of consulting services of engineering, procurement and construction have surged 113.9% in the past six months, outperforming the Zacks Building Products - Miscellaneous industry, the broader Construction sector and the S&P 500 Index.

Image Source: Zacks Investment Research

AGX stock is currently trading at a premium compared with the industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 58.24, as evidenced by the chart below.

Image Source: Zacks Investment Research

Earnings Estimate Revision of AGX

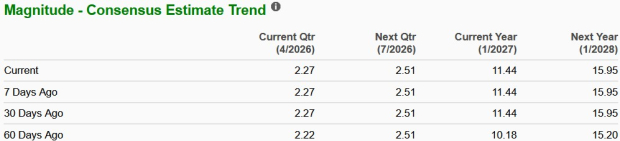

AGX’s earnings estimates for fiscal 2027 and 2028 have trended upward in the past 60 days. The revised estimates for fiscal 2027 and 2028 imply year-over-year growth of 17.5% and 39.5%, respectively.

Image Source: Zacks Investment Research

Argan currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

EMCOR Group, Inc. (EME): Free Stock Analysis Report

Argan, Inc. (AGX): Free Stock Analysis Report

Jacobs Solutions Inc. (J): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).