Unity Software U is entering the second-half of 2026 with a more balanced investment profile as improving advertising execution, expanding margins, and healthy liquidity support its long-term outlook. The company continues benefiting from stronger monetization within its Grow business, particularly through its Vector advertising platform, while ongoing restructuring efforts are helping stabilize profitability.

The stock has gained investor attention after Unity delivered stronger operating performance during recent quarters. However, valuation concerns and transition-related risks continue limiting the potential for a fully bullish investment thesis. Against this backdrop, Unity increasingly looks like a balanced growth story rather than an aggressive momentum play.

U Stock Outlook Anchored in Balanced Growth Profile

Unity’s long-term outlook remains neutral, with expectations that the stock will perform broadly in line with the market instead of significantly outperforming. The company’s improving fundamentals support stability, but restructuring noise and valuation concerns continue preventing a more directional bullish stance.

The investment case reflects strong Growth and Momentum characteristics offset by a weaker Value profile. Growth-oriented investors continue focusing on Unity’s improving ad monetization trends, while momentum indicators have strengthened alongside better profitability and free cash flow generation.

However, the stock does not appear deeply discounted relative to its operational and execution risks. That creates a setup where Unity looks suitable for investors seeking selective upside exposure instead of a high-conviction growth opportunity.

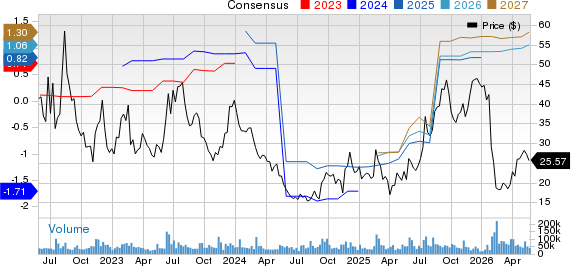

Unity Software Inc. Price and Consensus

Unity Software Inc. price-consensus-chart | Unity Software Inc. Quote

Unity Software Growth Powered by Vector Ad Momentum

Unity’s Grow segment remains the company’s most important growth engine heading into 2026. The primary catalyst has been Vector, Unity’s machine-learning advertising platform, which continues improving targeting, prediction accuracy, and advertiser engagement.

Strategic Grow revenue increased 49% year over year during the first quarter of 2026, driven largely by continued strength within the Unity Ad Network. Management attributed the acceleration to product upgrades and improving campaign optimization tied to Vector.

A major operational improvement involved the rollout of Day-28 return-on-ad-spend optimization. Advertisers are seeing better long-term campaign visibility compared with earlier Day-7 optimization methods, resulting in stronger advertiser confidence and higher spending levels.

Management also guided for Strategic Grow revenue growth of 50-52% year over year during the second quarter of 2026, reinforcing expectations that momentum will remain healthy.

Longer term, Unity expects runtime behavioral data integration to strengthen advertising performance further by incorporating richer user signals into live production models.

The emphasis on advanced advertising intelligence mirrors broader monetization initiatives at Roblox, where engagement-driven advertising opportunities are becoming increasingly important.

U Financial Trends Show Margin Expansion and Cash Strength

Unity’s first-quarter 2026 results reflected meaningful profitability improvement. Adjusted EBITDA increased to $138 million, while adjusted EBITDA margin expanded to 27%, improving significantly from the prior-year period.

The company also demonstrated improving cost discipline across key expense categories. Research and development spending declined as a percentage of revenue, while sales and marketing expenses improved alongside lower general and administrative costs.

Liquidity remains another important strength. Unity generated $66 million in free cash flow during the quarter and ended the period with approximately $2.14 billion in cash and equivalents.

The strong balance sheet provides flexibility to continue funding artificial intelligence initiatives, platform improvements, and future debt obligations.

Liquidity strength remains particularly important compared with Digital Turbine, which has experienced greater pressure from advertising volatility and platform uncertainty.

Unity Software Risks From Transition and Ad Volatility

Unity still faces several risks that could create near-term volatility. The company continues navigating revenue noise tied to the ironSource Ad Network shutdown and the planned Supersonic divestiture.

Approximately 80% of Grow revenue now comes from the Unity Ad Network, increasing exposure to advertiser spending shifts and mobile gaming demand trends.

Execution risk also remains elevated as Unity integrates runtime behavioral data into live production models.

Investors are also comparing Unity’s monetization strategy with peers such as AppLovin APP, Roblox RBLX and Digital Turbine APPS as competition intensifies across gaming and mobile advertising markets.

U Valuation Reflects Fair Pricing Relative to Growth Outlook

Unity currently trades near 22.18x forward earnings, below its historical median valuation of 412.02x. The valuation appears reasonable relative to sector benchmarks and aligns with Unity’s balanced outlook.

Comparisons with Roblox and Digital Turbine also highlight how investor sentiment across digital advertising and gaming companies remains highly sensitive to monetization consistency and execution.

Conclusion

Overall, Unity appears positioned as a hold-type stock with selective upside tied to continued Vector momentum, expanding margins, and improving cash generation. Unity currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AppLovin Corporation (APP): Free Stock Analysis Report

Digital Turbine, Inc. (APPS): Free Stock Analysis Report

Unity Software Inc. (U): Free Stock Analysis Report

Roblox Corporation (RBLX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).