Navient Corporation NAVI is attempting a major turnaround at a time when its core revenue streams remain under pressure. The company’s strategy now focuses on simplifying operations, cutting costs and repositioning its Earnest platform as a more scalable, capital-efficient fintech lender. While these efforts may improve efficiency, the key question is whether they can fully offset weak net interest income, lower servicing revenues and a highly leveraged balance sheet.

A major part of Navient’s transformation is its Phase 2 strategy, announced in November 2025. This plan builds on the company’s earlier restructuring efforts and focuses on higher-margin digital lending, cost reduction and operational efficiency. Navient has already taken several steps in this direction, including selling its healthcare services business in September 2024 and divesting its remaining government services business in February 2025. These moves have narrowed the company’s focus but also reduced diversification. The company has also significantly reduced its workforce. By the end of March 31, 2026, Navient lowered its headcount by more than 85% from the end of 2023, with total workforce reductions expected to reach nearly 90% by 2026. These initiatives helped the company complete its $400-million expense-reduction target by the end of March 31, 2026.

These cost-control measures are already showing results. In first-quarter 2026, total expenses declined 29% year over year. However, revenue pressure remains concerning. Net interest income fell 12.5% year over year and other income declined sharply. Servicing revenues have been shrinking due to the transfer of ED servicing contracts and the outsourcing of servicing operations.

Navient’s turnaround, therefore, will hinge on execution. While cost-cutting efforts should support near-term earnings and improve operating efficiency, they are unlikely to fully counter the pressure from weak revenue growth. To achieve sustained profitability, the company will need meaningful growth in refinance and in-school loan originations, greater margin stability and disciplined capital management.

Until then, its turnaround story remains promising but carries execution risks. This cautious outlook is reflected in the Zacks Consensus Estimate, which suggests a 3.8% decline in revenues for 2026, followed by an 11.1% rebound in 2027.

How Are NAVI Peers Positioned?

Salie Mae SLM has been focused on improving its NII by increasing the amount of cash and cash equivalents held to gain from yields on cash and other short-term investments. Also, the rising average loan balance and its focus on expanding the Private Education Loan portfolio will support NII growth. However, Salie Mae’s non-interest expenses continue to rise due to higher compensation and benefits expenses, along with planned investments in product enhancements and marketing costs, weighing on bottom-line growth.

Ally Financial’s ALLY net interest margin (NIM) has stabilized but remains sensitive to the path of deposit costs and asset repricing. NIM has improved to 3.43% in 2025 from 3.27% in 2024 and 3.33% in 2023. The uptrend continued in the first quarter of 2026. Even so, management expects the balance sheet to remain modestly asset-sensitive in the near term, and a relatively high-interest-rate backdrop is likely to keep funding competition elevated. Also, with Ally Financial launching products and focusing on core operations, non-interest expenses are expected to remain elevated in the near term.

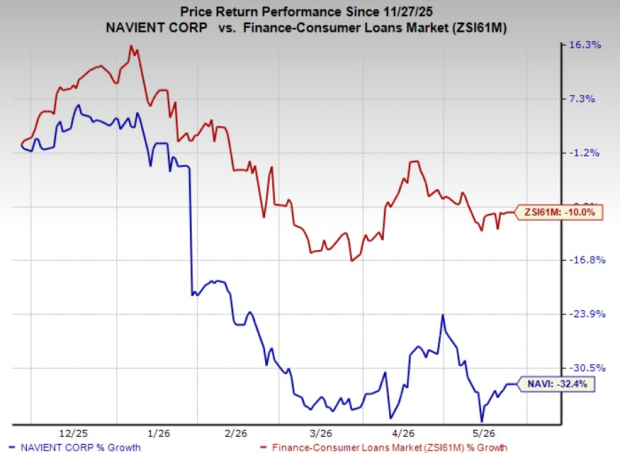

Navient Price Performance & Zacks Rank

The company’s shares have lost 32.4% in the past six months compared with the industry’s 10% decline.

Image Source: Zacks Investment Research

Currently, NAVI carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

SLM Corporation (SLM): Free Stock Analysis Report

Ally Financial Inc. (ALLY): Free Stock Analysis Report

Navient Corporation (NAVI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).