Founded in 2012, Figma (FIG) has evolved from a design tool into a connected, AI-powered platform that helps teams go from idea to shipped product, serving designers, developers, and product teams across the entire creative workflow. Led by co-founder and CEO Dylan Field, Figma went public on the NYSE on July 31, 2025, and has since rapidly expanded beyond its core design canvas.

Launched at Config 2025, Figma now offers Figma Make for AI-powered app and prototype generation, Figma Sites for live website publishing, Figma Draw for vector illustration, and Figma Buzz for brand asset creation at scale, effectively doubling the platform's surface area. With deepening AI partnerships across Google's (GOOG) (GOOGL) Gemini, OpenAI, and Anthropic, Figma is positioning itself as the indispensable creative layer of the AI-native software era, where, as CEO Dylan Field puts it, “when code is a commodity, design is the competitive edge.”

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Figma Stock Performance

Figma went public at an IPO price of $33 per share, with shares opening at $85 and closing at $115.50 on its NYSE debut, before suffering a dramatic post-IPO collapse driven by lock-up expirations, SaaS sector AI disruption fears, and valuation concerns. The stock's 52-week range spans from $16.60 to $142.92, with shares down significantly from their IPO price despite recent recovery momentum.

Against the Nasdaq Composite's ($NASX) approximately 8–9% year-to-date (YTD) return in 2026, FIG has dramatically underperformed the broader index, reflecting a sharp market re-rating of high-multiple, AI-exposed SaaS names since its mid-2025 listing. The stock's recent earnings-driven rebound suggests sentiment may be stabilizing.

www.barchart.com

www.barchart.com Figma Beats Estimates

Figma reported Q1 2026 EPS of $0.10, beating the consensus forecast of $0.06 by approximately 67%, while revenue of $333.4 million exceeded projections of $316 million by 5.5%, sending shares up nearly 7% in aftermarket trading. Revenue grew 46% year-over-year (YoY), accelerating from 40% growth in the previous quarter, marking the second consecutive quarter of growth acceleration, a rare feat for a company of Figma's scale.

Q1 delivered $275 million in gross profit at an 82% margin, $52 million in non-GAAP operating income at a 16% margin, and $89 million in free cash flow at a 27% margin. Net dollar retention hit 139%, the highest in over two years, amid strong seat expansion across both new and existing customers, while international sales grew 48% year over year, outpacing the company's overall growth rate and underscoring Figma's accelerating global expansion.

Following the strong beat, Figma raised its full-year 2026 revenue guidance by $55 million to $1.422–$1.428 billion, implying 35% growth, while increasing its operating income guidance to $125–$135 million. CFO Praveer Melwani stated that the company is "raising our guidance for the year based on promising early traction on AI monetization and strength across the core platform, a testament to the team's execution and our confidence in the road ahead." CEO Dylan Field added that as AI continues to commoditize code, human-driven design judgment becomes an even more critical competitive differentiator, reinforcing management's conviction that Figma's AI-native platform strategy is durable rather than disruptive to its long-term business model.

Analyst Upgrades FIG Stock

Citi began coverage of Figma with a “Buy/High-risk” rating and a $36 price target, sending shares up approximately 3% in premarket trading. While acknowledging legitimate concerns around seat compression as AI-native, low-cost design tools proliferate, Citi analysts believe the market underestimates offsetting growth drivers, including seat mix upgrades, expanding non-designer personas, and rising AI-driven consumption.

Proprietary customer and go-to-market checks with hyperscalers and large financial services firms revealed strong seat upgrades and credit pack utilization, reinforcing confidence in Figma's AI monetization strategy. Citi's Q2 and full-year 2026 revenue estimates sit seven and nine points above consensus, respectively, with catalysts including the upcoming Config conference and new MCP server monetization launches, though a final lock-up expiry in mid-August remains a key offsetting risk to watch.

Should You Buy FIG?

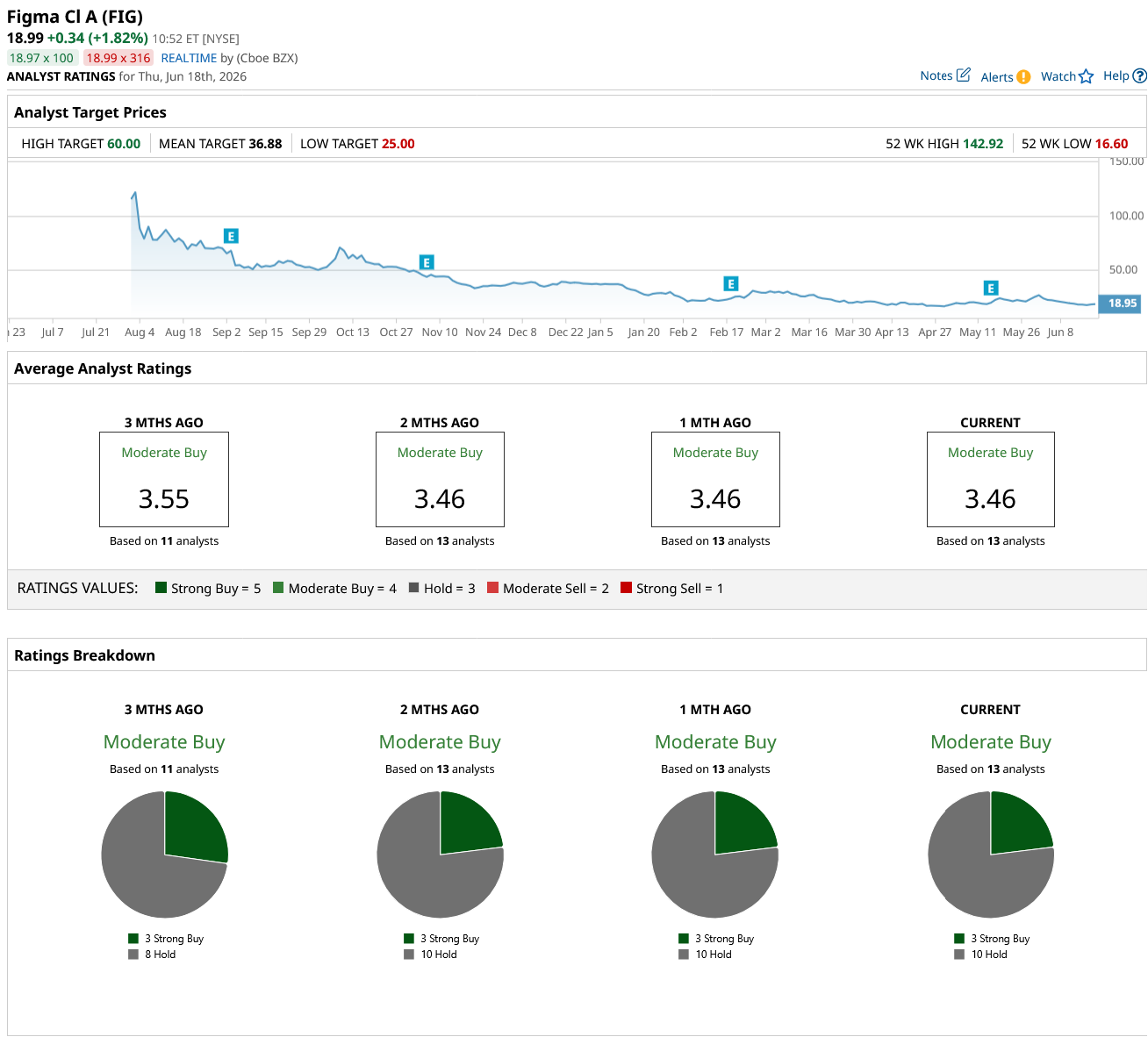

With Citi's bullish initiation and $36 price target reinforcing confidence in Figma's AI monetization strategy, institutional sentiment toward the design platform appears to be turning a corner. However, the broader analyst consensus remains more measured; FIG carries a "Moderate Buy" rating across 13 analyst ratings, comprising three "Strong Buy" and 10 "Hold," with a mean price target of $36.88.

For investors, Figma represents a high-risk, high-reward opportunity in the AI-native software space, one where conviction in the company's seat expansion and AI monetization roadmap must be weighed carefully against valuation and ongoing lock-up-related volatility.

www.barchart.com

www.barchart.com On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Citi Initiates Bullish Coverage on Figma Stock as the AI Monetization Story Takes Shape American Express Stock Is Powering the Financial Sector to a Fresh Breakout Intel Stock Is Soaring: Why a $150 Price Target Could Be Within Reach in 2026 AMD and Rackspace Team Up on a 30 MW AI Compute Agreement. This Could Be a Win for Both Stocks.