The renowned Big Short Investor Michael Burry likes unpopular stocks. That is part of the appeal. Last week, He bought more PayPal Holdings (PYPL) while the market was still worried about slower growth, tougher competition, and a messy turnaround.

PayPal is still a giant in digital payments. It reaches about 200 markets and sits inside online checkout, peer-to-peer transfers, merchant tools, and cross-border payments. That gives it real scale, but it has also left investors asking whether the stock is cheap for a reason.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Is PayPal a Value Opportunity or a Value Trap?

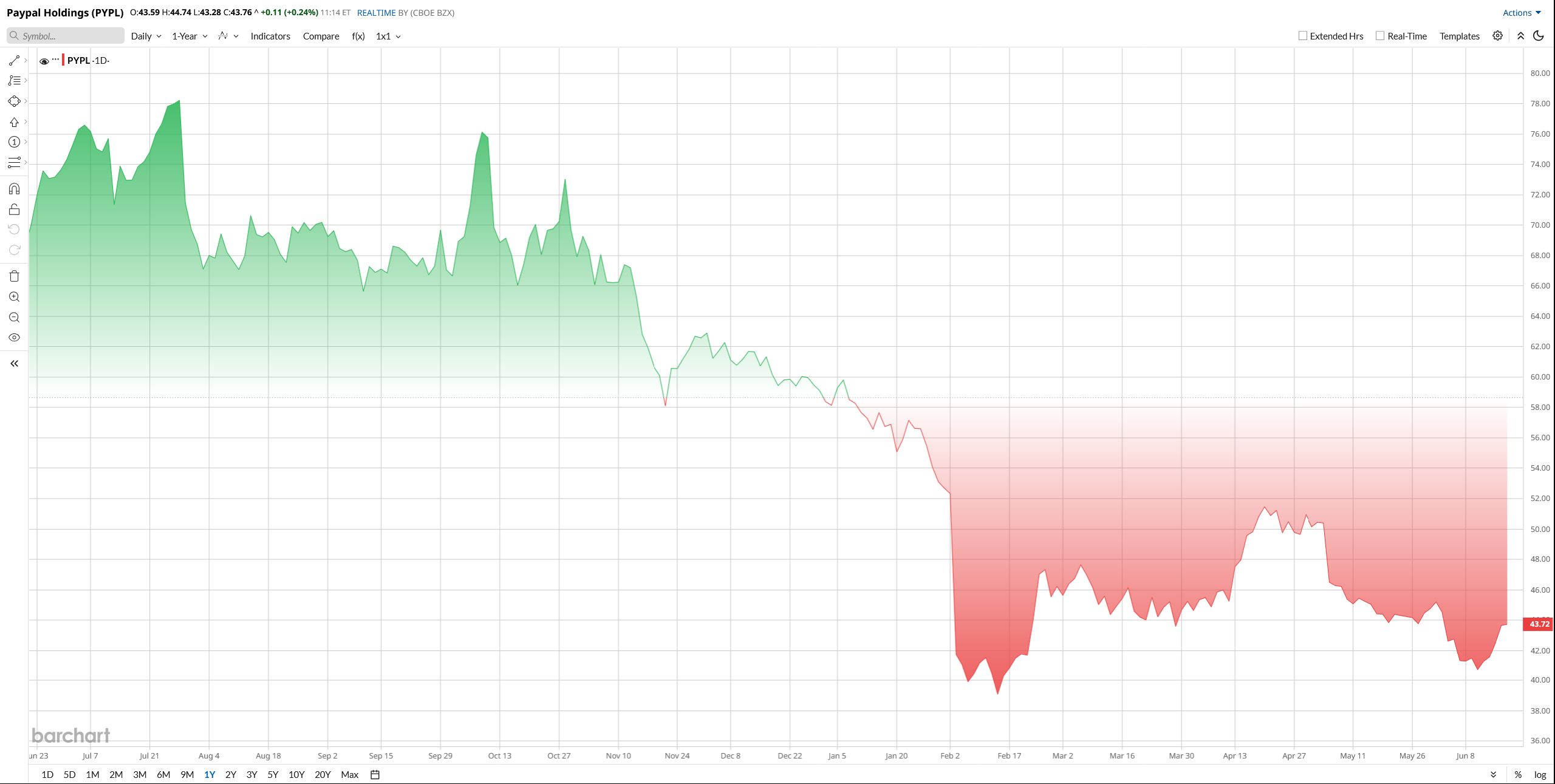

PYPL stock has had a rough ride. The shares are down about 45% from their 52-week high of $79.50. It has also fallen nearly 25% year to date (YTD), and it remains below both its 50-day moving average of $46 and 200-day moving average of $56. That is not a great technical setup. It says the market still wants proof, not hope.

The reason is simple. Investors do not trust the growth story yet. PayPal beat first-quarter results, but the company still guided for weaker EPS ahead, and the stock sold off anyway. When a stock is this beaten down, even decent results are not enough unless the outlook starts to improve.

On valuation, PayPal looks inexpensive. It trades at about 7.7 times trailing earnings, which is well below the S&P 500 financials sector’s 16.8 times P/E. It also trades at about 1.8 times sales, which is far below richer payment names like Visa (V) and Mastercard (MA), though close to lower-multiple peer Block (XYZ). In plain English, the market is not giving PayPal much credit for future growth right now.

That is why Burry’s move gets attention. He tends to buy when expectations are low and the crowd is impatient. The risk is that cheap stocks can stay cheap if the business does not reaccelerate.

www.barchart.com

www.barchart.com Michael Burry Sees Value

Burry’s bet fed the old value verses growth debate. He disclosed that he opened a roughly 3.5% position in PayPal, which many traders read as a vote of confidence in a stock the market had already written off.

At the time, Burry viewed PayPal’s depressed valuation as an opportunity rather than a warning sign. “I added to PayPal at $40.98,” he said, while criticizing what he saw as excessive negativity toward the stock. “The market has been attending PayPal’s wake for years now, though the body has yet to show.”

Social media also latched onto the company’s buybacks and low multiples. Still, the stock reaction was muted because the bigger issue is not sentiment. It is execution.

That is why the question is not whether PayPal is hated. It is. The real question is whether management can turn that hate into a better business before the valuation turns into a value trap.

The Latest Quarter Was Better Than It Looked

PayPal smashed the Q1 earnings estimate and delivered solid sales growth. Revenue rose 7% to $8.35 billion. Transaction revenue was $7.5 billion, while revenue from other value-added services was $852 million. Total payment volume climbed 11% to $464 billion, helped by stronger activity across the platform.

Profit was less impressive, though. Net income fell 14% to $1.11 billion. On the brighter side, non-GAAP EPS rose 1% to $1.34, free cash flow came in at $903 million, and adjusted free cash flow reached $1.72 billion. PayPal ended the quarter with $13.5 billion in cash, cash equivalents, and investments.

CEO Enrique Lores said management is sharpening strategy, simplifying the organization, and improving the cost structure. That sounds like a company trying to get back to basics.

Looking ahead, for the second quarter, PayPal expects EPS to decline in the mid-single digits and non-GAAP EPS to fall about 9%. For the full year, it still sees GAAP EPS down in the mid-single digits and non-GAAP EPS down slightly to flat. Analysts expect 2026 EPS of about $5.34 and revenue of about $34.3 billion.

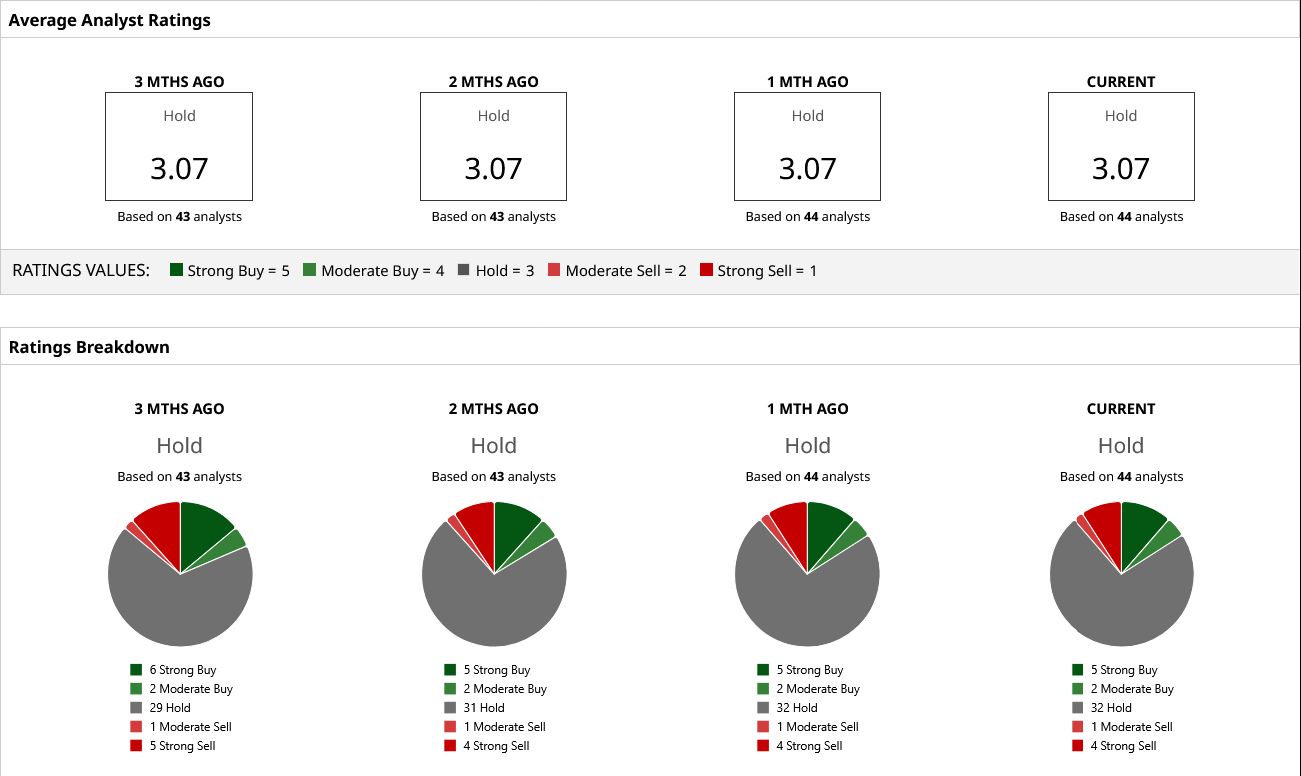

What Wall Street Thinks of PYPL Stock

Wall Street has a mixed opinion on PYPL stock. Barchart shows a consensus “Hold,” with 44 analysts covering the name. Analysts also put the mean price target at $48.30, which implies about 10% upside from the current price.

Analysts acknowledge PayPal’s strengths: a $14 billion cash pile, with $6 bilion free cash flow, and fast-growing Venmo & BNPL segments. But they worry that PayPal’s core has slowed. In short, the street is not cheering, but it is also not abandoning the stock.

My take is simple. Burry may be early, but he is not crazy here. PayPal looks cheap, throws off cash, and still has a credible turnaround story. But this is not a clean follow-the-smart-money trade. It is a patience test.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

How to Hunt for Mega-Cap Value After the SpaceX IPO PayPal Stock Trades at 7.7x Earnings. Michael Burry Thinks That’s an Opportunity. Unusual Options Activity Flags UMC, ASX and QXO Ahead of July Expiration While Investors Chase AI, Hidden Value Is Forming Somewhere Else