While the 2008 financial crisis is but a distant memory, the lessons learned from that era continue to be felt in the stock market. Michael Burry, who at the time was running the Scion Capital hedge fund, identified that the housing market was under duress because of an unsustainable bubble of risky subprime loans. Burry and his associates famously bet that the house of cards would fall. The trade was depicted in a book and movie of the same title, The Big Short.

Burry has since closed his hedge fund and today operates a Substack, Cassandra Unchained, in which he talks about the markets. His Substack is closely watched by investors because of his often contrarian takes on the market. One of Burry's most recent posts highlights Adobe (ADBE), which he says has been unfairly punished as investors ignore cash-generating companies in favor of flashy AI stocks that carry sky-high valuations.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

“These companies generally are suffering in comparison to AI capital flows as well as to extrapolated maximum-AI scenarios that are unlikely," Burry wrote. “LLMs are language models, not AI. No one is using AI yet. Companies are spending hundreds of billions, even trillions, of dollars on making language models the last search engine one will ever need. There is no evidence of anything more [than] that, and there is plenty of evidence that the training of these search engines is hitting diminishing returns well before profitability, let alone return of capital.”

Burry argues that investors are pricing AI on the most optimistic future possible, rather than on what it’s worth today, which may be too aggressive.

Burry was right about the housing market. Is he right about overvalued AI stocks as well? Let’s take a closer look at Adobe, which he identifies as a solid software stock to buy now.

About Adobe Stock

Adobe is best known for its cloud software products, including Photoshop and Illustrator, which are used for media creation and marketing, as well as Acrobat, which is most often used to create PDFs. The company has also released Firefly, a generative AI model that allows users to create graphics, images, and text effects from written prompts. Firefly is incorporated into its Creative Cloud apps, such as Illustrator and Photoshop.

However, ADBE stock is down 48% over the last 12 months on fears that software stocks and their traditional subscription models will be punished by new AI features that could duplicate the products of software firms like Adobe. In Adobe’s case, the fear is that generative AI is reducing the value of its Creative Cloud offerings, which help users create photos and graphics.

www.barchart.com

www.barchart.com But that drop is also making Adobe stock historically affordable. The stock’s forward price-to-earnings (P/E) ratio is 9.8 times, which is a multi-year low. As way of comparison, the P/E 10-year mean for ADBE stock is more than 45 times.

In addition, ADBE stock fell another 7% on June 12 after announcing that Chief Financial Officer Dan Durn will step down in mid-June.

Adobe Is Dramatically Changing Its Business

Despite issues that have pushed the stock price down, Adobe reported solid second-quarter earnings and raised its full-year guidance. Revenue was $6.62 billion in Q2, up 13% from a year ago. Cash flows from operations were $2.17 billion, while net income was $2.4 billion. Adobe reported EPS of $5.96 on a non-GAAP basis.

What's more, the company reported these results while making massive changes to its core business model. For years, Adobe operated on a model in which it signed people up to its Creative Cloud suite so they could learn how to use Illustrator, Photoshop, and other products. The addressable market was confined to creative professionals.

Now, AI is expanding the addressable market to more business users and consumers — and changing what that market wants. Adobe seems to understand that more people would rather use AI tools to create content than spend months learning Photoshop. Its answer is to make its basic versions free — a so-called “freemium” model — and get customers to pay for more powerful tools. If Adobe can increase the number of people using its free products, it has a better chance of converting them to paid users.

Adobe said it increased the number of customers in its Business Professionals and Consumers segment from 700 million to more than 850 million in the last year. “The opportunity is to serve billions of business professionals and consumers through a comprehensive freemium funnel, building on the success of the Adobe Reader model,” said CEO Shantanu Narayen.

“For next-generation creators, the opportunity is to deliver an AI production studio across web and mobile that seamlessly integrates with the power and precision capabilities of Creative Cloud,” Narayen said. “We have increased our creative freemium MAU from 50 million to 90 million year-over-year. The opportunity is to attract hundreds of millions of additional creators through a freemium funnel based on the early success of Firefly.”

Adobe’s full-year guidance calls for revenue between $26.5 billion and $26.6 billion, with non-GAAP EPS in the range of $24.35 to $24.45 per share.

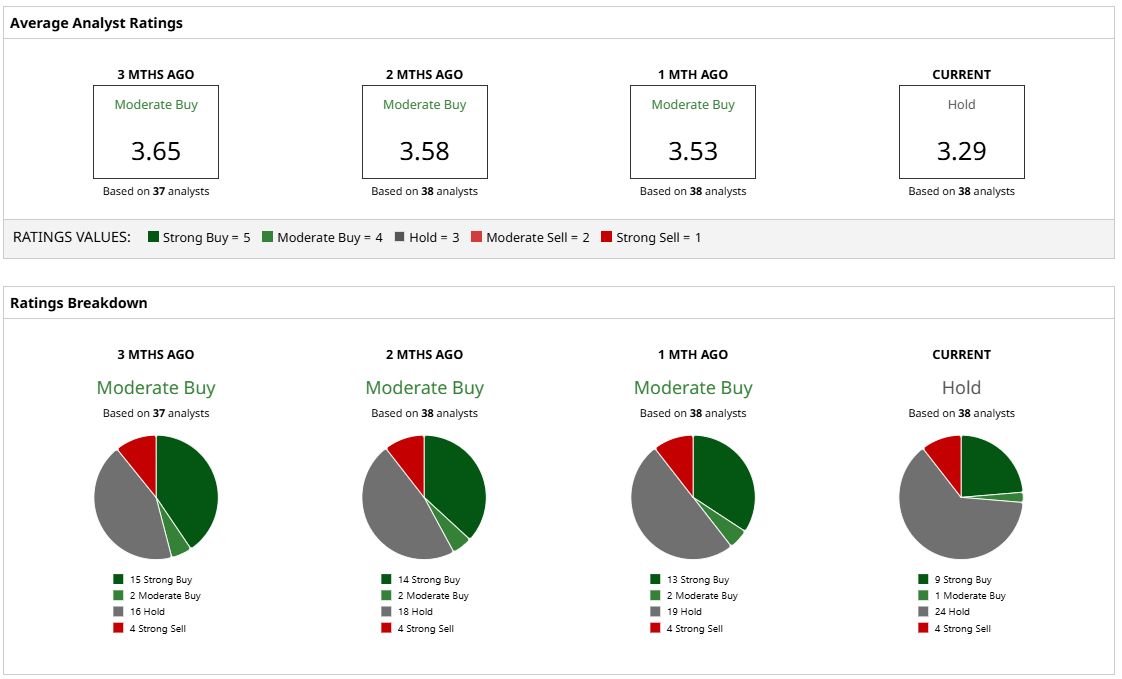

What Do Analysts Expect for Adobe Stock?

While Burry sees value in Adobe, analysts are more divided, with 38 experts who cover ABDE stock offering a consensus “Hold” rating. Only nine analysts have a “Strong Buy” rating, one has a “Moderate Buy,” 24 analysts have a “Hold” rating, and four have a “Strong Sell” rating. Notably, the sentiment against Adobe has worsened over the last three months. The mean price target of $276.19 represents potential upside of 41% from current levels, while the most bullish target of $460 represents a huge potential jump of 136%.

Burry has done well with his contrarian bets in the past, and Adobe is notably increasing revenue while ramping up its freemium products. If management can successfully convert freemium users into paying customers, today's depressed valuation could prove attractive for long-term investors.

www.barchart.com

www.barchart.com On the date of publication, Patrick Sanders did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Michael Burry Thinks the Market Has Adobe Stock Wrong. What Management Needs to Do to Prove Him Right. Nothing Seems to Be Going Right for Meta Platforms. How to Play META Stock Here. Hormuz Status, MU Earnings and Other Key Things to Watch this Week Why This Analyst Thinks Nano Nuclear Energy Stock Can Gain 78% from Here