On Wall Street, being contrarian and going against the tide has been the investment philosophy of many market legends. Warren Buffett's bet on Goldman Sachs (GS) at the height of the global financial crisis comes across as a shining example. However, investment firm Seaport Research's rationale behind going “Underweight” on Broadcom (AVGO) is built on shaky grounds.

Seaport's Skepticism About Broadcom Misplaced

Sample this: in a note to clients, the firm's bearish case on the chip major says, “Broadcom retains its position as the leading competitor to Nvidia for AI compute, but just like Nvidia, the company is now increasingly confronting the limits of the industry. Beyond the headlines of industry shortages, we also see Broadcom increasingly getting drawn into the market for financing customers. Broadcom is doing well, but we see its gains as fully factored into consensus now.”

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

So, the firm's contention is about an issue that was doing the rounds mid-to-late last year, i.e., circular financing. However, shares of the VanEck Semiconductor ETF (SMH), one of the largest ETFs covering chip stocks, are up about 24% since then, even amid the headwinds of war. Moreover, the AI infrastructure buildout requires massive capex, which may not be available for some of the partners of these chip giants. Financing them with real cash and revenues should not seem to be an issue for now.

And specifically for Broadcom, in a later part of the note, Seaport itself found no issues with the company, stating, “To be clear, we believe Broadcom's business is still in very good shape. The company is poised to grow revenue 60% this year on the back of strong adoption of its ASIC business around Google, Anthropic, and the others.”

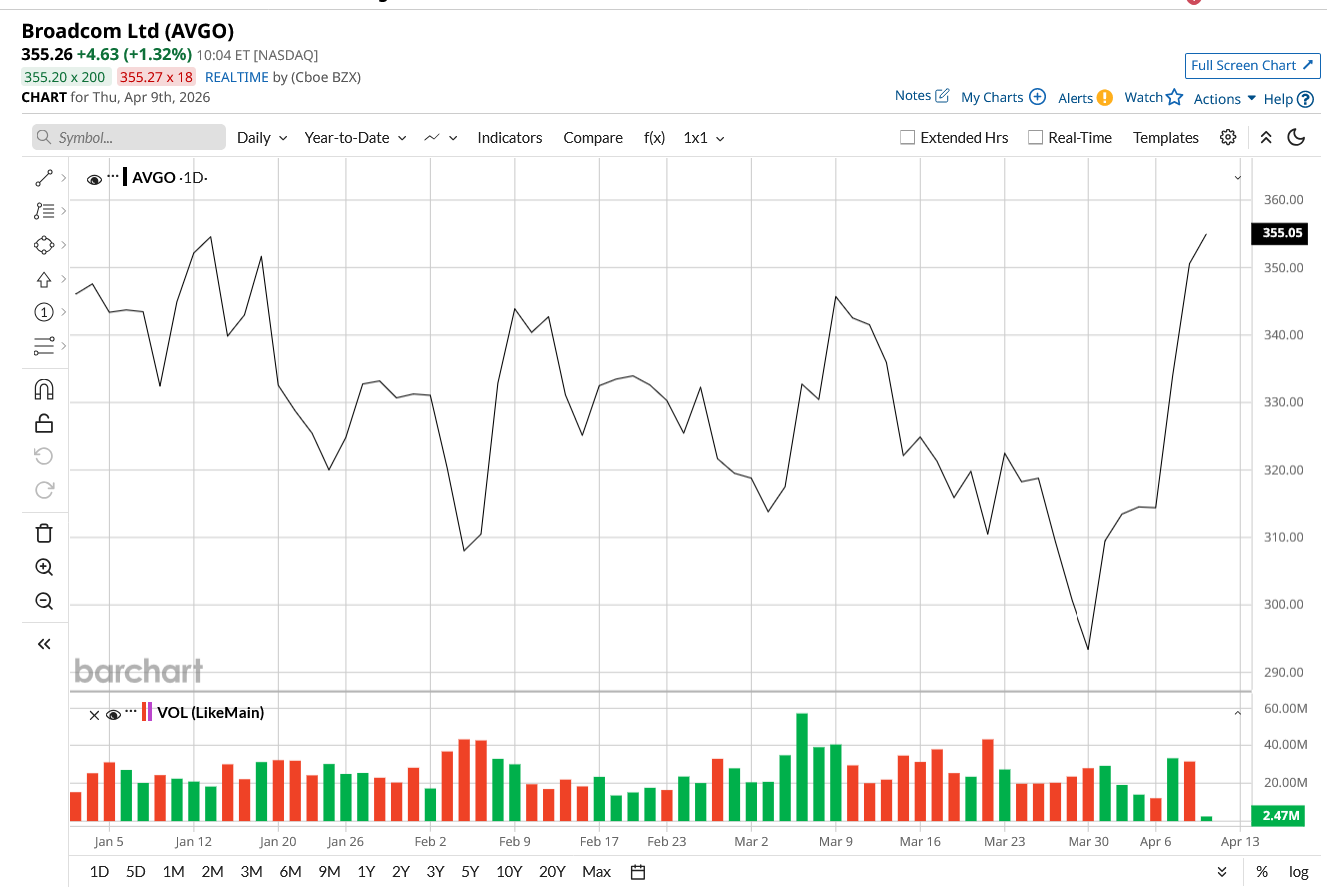

Valued at a mammoth market cap of $1.6 trillion, the AVGO stock is up a mere 2.6% on a year-to-date (YTD) basis. However, with several possible tailwinds, should Seaport's advice be heeded, and should investors avoid Broadcom? I reckon not to, and here's why.

www.barchart.com

www.barchart.com Starting in 2026 From Where It Left off in 2025

Broadcom kick-started 2026 similarly to 2025: with a beat on earnings and revenues.

In Q1 2026, Broadcom's revenue came in at $19.3 billion, representing a 29% year-over-year (YoY) growth rate. The Semiconductor Solutions segment of the company, which includes its data center revenues and marquee customers like Alphabet's (GOOG) (GOOGL) Google and Claude-maker Anthropic, saw a 52% yearly jump in revenues to $12.5 billion. On the other hand, revenues from the Infrastructure Software side of the company were at $6.8 billion, up a mere 1% in the same period.

Meanwhile, earnings were up 28% from the previous year to $2.05 per share. This was also above the consensus estimate of $2.05 per share, marking the ninth consecutive quarter of earnings beat from the company.

Furthermore, not just for the short term, over the last decade, Broadcom's revenue and earnings have grown at great CAGRs of 25.65% and 33.11%, respectively.

Q1 2026 also saw Broadcom increasing its cash flow from operations and free cash flow at YOY rates of more than 30%. While cash flow from operations at $8.3 billion denoted an annual growth rate of 35%, free cash flow grew by 33% from the previous year to $8 billion, which should alleviate some concerns about the company not being able to finance alleged vendor financing deals. Further, the company also authorized a new $10 billion share repurchase program.

The company has guided Q2 revenues to be $22 billion. If realized, this would denote an annual uptick of 47%.

However, the AVGO stock continues to trade at overvalued levels, but it is within the realms of sanity. Its forward P/E, P/S, and P/CF are 29.43, 15.10, and 29.06, which are all within the vicinity of the sector medians at 21.74, 2.96, and 16.53, respectively. In fact, its forward PEG ratio, which considers the company's massive growth rate, stands at 0.71, lower than the sector median of 1.32.

Broadcom Is Looking Unstoppable

Broadcom's expansion is fueled by absolute dominance in the custom chip market, where it designs specialized processors tailored to the exact specifications of companies like Google, Meta (META), and Anthropic. As agentic applications require efficient scaling, the industry is realizing that standard GPUs can be too expensive for specific workloads. Here is where Broadcom comes in as the ultimate design partner by managing complex engineering and foundry relationships with TSMC (TSM) to deliver millions of custom tensor processing units.

Notably, the company maintains a formidable competitive edge over peers like Marvell (MRVL) through a unique combination of networking supremacy and advanced interconnect technology. While Marvell is growing its custom silicon footprint, Broadcom still commands roughly 80% of the Ethernet switching market as of early 2026. Its Tomahawk 6 switch is the first production hardware to deliver 102.4 terabits per second of bandwidth, acting as the critical backbone linking massive computing clusters together.

Broadcom also tightly integrates advanced optical engines and networking cores directly into its silicon to maximize energy efficiency. The massive scale of the enterprise generates billions of dollars in annual free cash flow, providing an R&D budget that smaller rivals find difficult to match.

To sustain its leading position, Broadcom is aggressively advancing its technology roadmap to address the extreme power and bandwidth bottlenecks of future supercomputers. The company is actively developing its Tomahawk 7 switch, projected for a 2027 release, which aims to double current switching capacities to a staggering 204.8 terabits per second. Management is also pioneering newer optical interconnects that integrate silicon photonics directly with compute components to slash power consumption drastically.

Finally, the leadership team already has a line of sight to over $100 billion in chip sales for 2027, backed by massive gigawatt-scale infrastructure contracts with clients like Anthropic. By pairing these hardware leaps with the recurring software revenue from its VMware acquisition, Broadcom is building an impenetrable hybrid infrastructure moat.

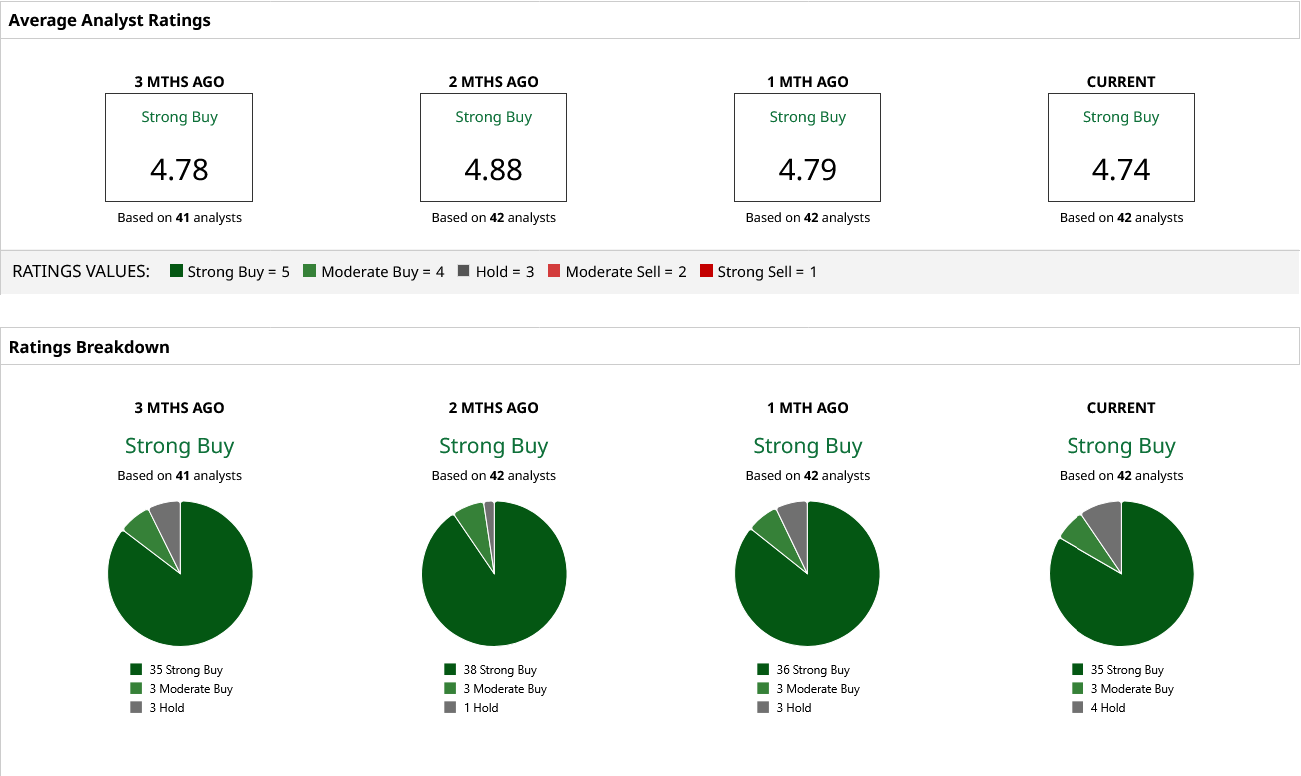

Analyst Opinion on AVGO Stock

Thus, unsurprisingly, analysts have earmarked an overall rating of “Strong Buy” for AVGO stock, with a mean target price of $467.64. This indicates an upside potential of about 32% from current levels. Out of 42 analysts covering the stock, 35 have a “Strong Buy” rating, three have a “Moderate Buy” rating, and four have a “Hold” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Should You Chase the Rally in Royal Caribbean Stock Today? Seaport Research Warns on AVGO Stock: Broadcom Is Confronting the ‘Limits of the Industry’ This S&P 500 Stock Is Up 814% in Just the Past Year Broadcom Is Making AI Chips with Google. Does That Make AVGO Stock a Buy Now?