Rocket Companies RKT is operating in a mortgage market that is still fighting the last cycle. Housing conditions remain restrictive, and the path to a healthier origination mix is not straightforward.

At the same time, Rocket is absorbing two major acquisitions while carrying a heavier cost structure and interest burden. The setup leaves the stock sensitive to both execution and the timing of any rate-driven demand recovery, even with an integrated platform that could benefit when conditions improve.

RKT Faces a Tough Housing Backdrop

Low housing inventory, elevated home prices and affordability pressure continues to reduce transaction volumes and slow purchase demand. That matters because purchase activity is the primary source of originations when refinancing remains subdued.

Mortgage rates have eased from prior peaks, but they are still relatively high. Combined with cautious consumer sentiment, that backdrop can suppress home turnover and keep both origination and refinance volumes constrained. In a purchase-driven market with fewer total loans available, near-term upside tends to be limited, and lenders often compete harder for each transaction.

Rocket’s Expense Base and Interest Burden Stay Heavy

Rocket’s expense profile remains a central investor concern. Over the last six years (2019-2025), total expenses increased at an 8.8% compound annual growth rate, and integration-related charges add to the burden. A higher interest burden compounds the challenge by raising the bar for volume-driven profitability improvement.

The most recent quarterly results underscore the pressure. In the fourth quarter of 2025, total expenses rose sharply year over year to $2.52 billion, offsetting the benefit from materially higher revenues. Without a stronger rate-driven volume tailwind, the company’s elevated cost base can delay meaningful profitability improvement.

RKT Integrates Redfin and Mr. Cooper With Execution Risk

Rocket is simultaneously integrating Redfin and Mr. Cooper, which increases execution and timing risk. Even when early indicators are described as constructive, integrating two large businesses at once can create friction in systems, workflow and operating cadence. The risk is not limited to whether integration works, but how quickly it works.

The Mr. Cooper transaction is significant in scale. Rocket completed the $14.2 billion all-stock acquisition in October 2025, creating a combined servicing footprint expected to serve nearly 10 million clients and manage a $2.1 trillion unpaid principal balance. That expands strategic optionality, but it also raises the importance of clean integration to avoid cost creep and delayed operating leverage.

Rocket Targets Synergies, but Timing Is the Swing Factor

Management targets $540 million of total cost synergies across the two deals, and the pace of capture is critical. In a muted origination environment, “when” those benefits arrive can be as important as “how much,” because the company needs efficiencies to show up before expenses and interest burden eat away at incremental gains.

On the Mr. Cooper side, management has line-of-sight to $400 million of expense synergies, plus an incremental $100 million of revenue tied to higher blended recapture rates. The platform is also expected to scale volume without proportional headcount or cost escalations, supported by capacity improvements and technology investment. Those are meaningful levers, but the operating leverage story depends on how quickly synergy capture ramps while industry volumes remain restrained.

RKT Faces Regulatory Uncertainty and Competitive Intensity

Mortgage origination and servicing are highly rule-bound, and regulatory changes remain an overhang. Stricter requirements can lift compliance costs, slow cycle times, restrict product flexibility, and tighten marketing and disclosure practices. Those dynamics can pressure efficiency and limit how aggressively lenders can adjust offerings to meet borrower demand.

Thus, RKT currently carries a Zacks Rank #5 (Strong Sell).

Competition is also intense across direct-to-consumer lenders, banks, credit unions and fintech platforms. In a market with fewer loans to win, pricing concessions and heavier promotions can pressure gain-on-sale margins and reduce the benefit of recapture. Within the same mortgage and related services space, Zillow Group ZG and PennyMac Financial Services PFSI both carry Zacks Rank #3 (Hold), highlighting that investor sentiment varies widely across the peer set as the cycle resets.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

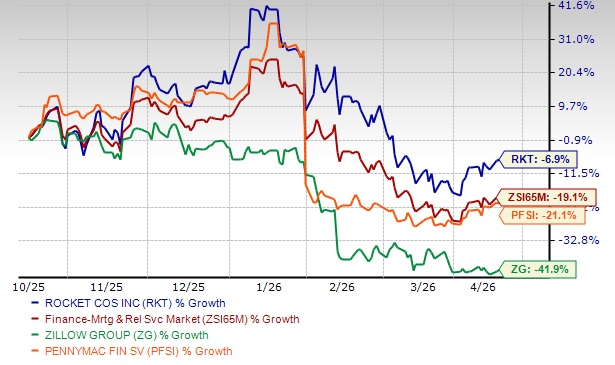

In the past six months, shares of RKT have lost 6.9%. ZG and PFSI shares have lost 41.9% and 21.1%, respectively, in the same time frame.

6-Month Price Performance

Image Source: Zacks Investment Research

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Rocket Companies, Inc. (RKT): Free Stock Analysis Report

PennyMac Financial Services, Inc. (PFSI): Free Stock Analysis Report

Zillow Group, Inc. (ZG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).