Regardless of remaining the most dominant company in the artificial intelligence (AI) infrastructure space, Nvidia (NVDA) stock has trailed some of its semiconductor peers in 2026. Shares are up 14.75% year-to-date (YTD), compared to massive rallies in rivals such as Advanced Micro Devices (AMD) and Intel (INTC).

While Nvidia's stock has lagged peers, its financial and operating performance remains exceptionally strong, in spite of operating at a significantly larger scale than its competitors and facing tough year-over-year (YOY) comparisons.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Moreover, Nvidia stock is trading at a significantly lower multiple than its peers and offers solid growth, which strengthens its bull case.

www.barchart.com

www.barchart.com Nvidia Continues to Deliver Massive Growth

Nvidia’s latest quarterly results show the reason the company remains central to the global AI boom. In the first quarter, total revenue surged 85% YOY to $82 billion. Moreover, the top line jumped 20% sequentially. Management highlighted that Q1 was the third consecutive quarter of accelerating annual growth and its fourteenth straight quarter of sequential revenue expansion.

Nvidia’s top line is driven by unprecedented demand for its Blackwell GPUs. Data center revenue remained the core growth engine. The segment generated $75 billion in revenue, up 92% YOY and 21% sequentially. Nvidia said demand for its GB300 and NVL72 systems has been especially strong among frontier AI model builders and major hyperscale customers.

Within the data center segment, computing revenue climbed 77% YOY to $60 billion, while networking revenue nearly tripled to $15 billion. Nvidia also reaffirmed expectations for $1 trillion in combined Blackwell and Rubin revenue between 2025 and 2027, reflecting management’s confidence in sustained demand for AI infrastructure.

CPUs Could Open a Massive New Market for Nvidia

While Nvidia is already dominant in AI GPUs, the company is now preparing to aggressively expand into CPUs with its upcoming Vera platform. Management believes the next wave of AI computing, particularly agentic AI, will create significant new opportunities beyond GPUs alone.

Nvidia’s management estimates the CPU market represents a $200 billion total addressable market in which the company has not yet meaningfully participated. And, Nvidia noted that nearly every major hyperscaler and system manufacturer is already partnering with the company to deploy Vera-based systems.

The company expects to deliver nearly $20 billion in CPU revenue this year alone, suggesting this business could quickly become another major growth driver.

Nvidia’s Strong Outlook and Shareholder Returns

Looking ahead, Nvidia expects second-quarter revenue of approximately $91 billion, which indicates strong YOY and sequential growth. Notably, the data center business will continue to drive growth. Moreover, it is focused on securing the supply chain to capitalize on strong demand.

Beyond growth, Nvidia is increasing shareholder returns. Management announced a new $80 billion share repurchase program, bringing the total to $39 billion under its existing program. The company previously indicated plans to return roughly 50% of free cash flow to shareholders this year, reflecting confidence in both profitability and cash generation.

Nvidia Still Looks Reasonably Valued

Nvidia’s valuation remains surprisingly reasonable relative to its expected growth. The stock currently trades at 26.72 times forward earnings, which appears modest given analysts' 76% earnings growth forecast for fiscal 2027. Also, Nvidia is expected to deliver profitable growth in fiscal 2028, with EPS projected to increase by more than 35% YOY.

By comparison, Advanced Micro Devices trades at a much higher forward earnings multiple of 81.29 times, while Intel also commands a richer valuation.

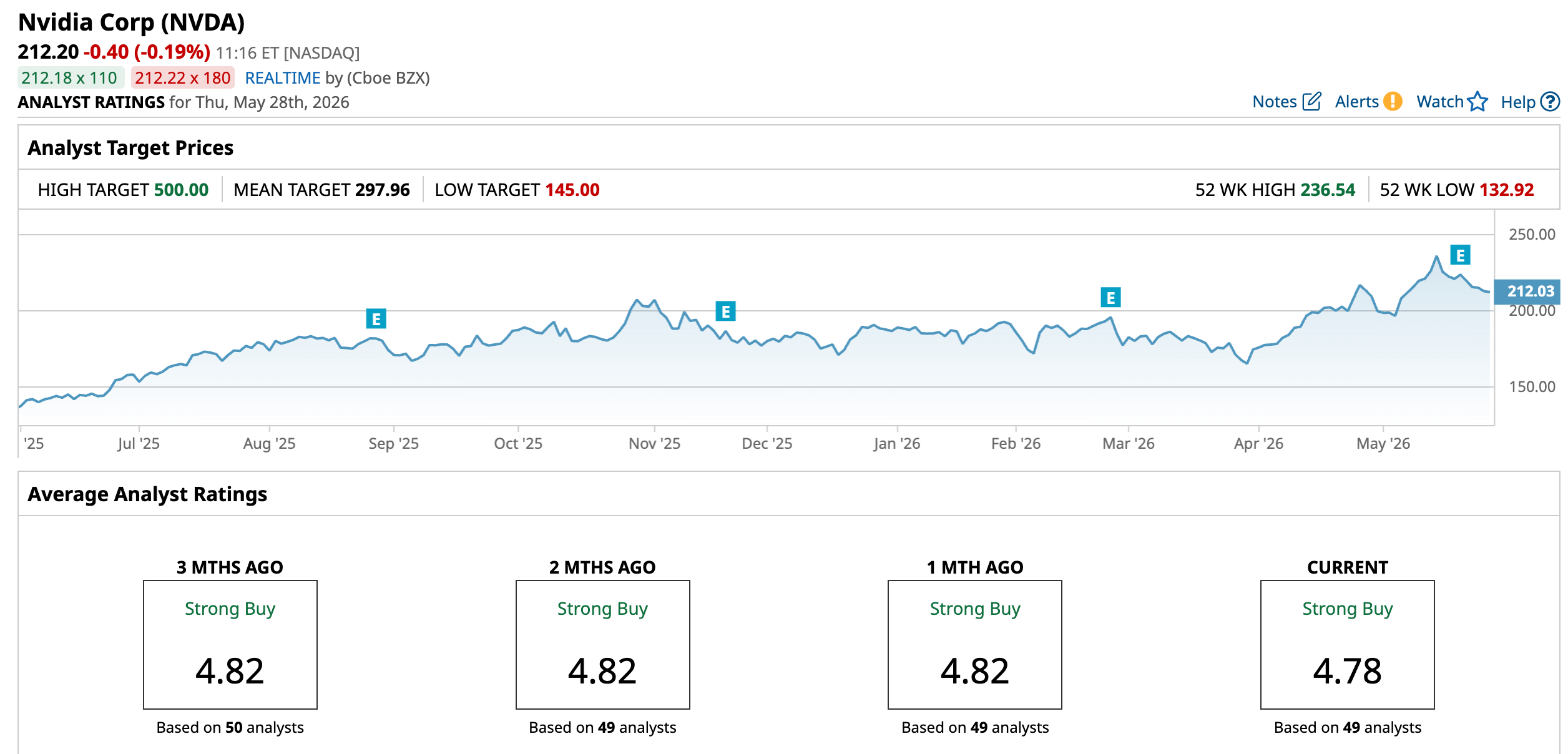

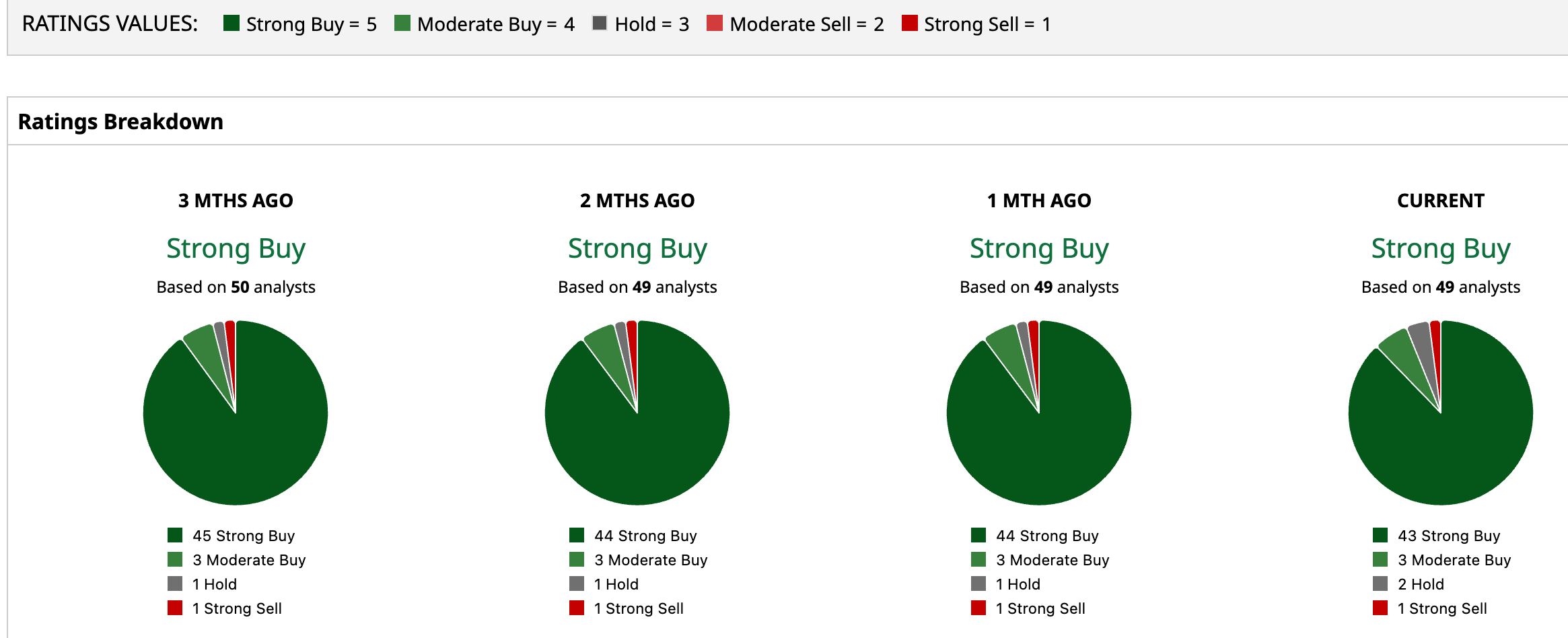

Is Nvidia Stock Still a Buy?

Although Nvidia has underperformed its semiconductor peers in 2026, the company’s underlying business momentum remains exceptionally strong. Revenue growth continues to accelerate, AI demand shows no sign of slowing, and new opportunities in CPUs augur well for growth.

At the same time, the stock’s valuation remains relatively attractive compared to both its growth outlook and industry peers. Combined with aggressive share buybacks and dominant positioning in AI infrastructure, Nvidia stock is a “Buy.”

Wall Street analysts are also bullish, maintaining a “Strong Buy” rating on NVDA stock.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Prepare for a Volatile Ride Ahead in Lam Research Stock After 278% Gains Nvidia and Micron Stocks Are Almost Exclusively Driving S&P Earnings Strength. These 3 Very Real Risks Could End It All. Aggressive Share Buybacks and Dominant Positioning Still Make Nvidia Stock a Top Buy Now The $43 Billion Reason to Buy Microsoft Stock Here