Once again, the Street is getting aggressively bullish on Nvidia (NVDA) ahead of earnings. This time, however, Wall Street sees something bigger than an earnings beat as an opportunity.

Wolfe Research recently reiterated its "Outperform" rating on Nvidia, referring to NVDA stock as its best pick in the AI Infrastructure theme. This comes as worries about hyperscaler capex spending are allayed due to strong cloud first-quarter earnings and capex forecasts for the coming years. Let's take a closer look.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About Nvidia Stock

Based in Santa Clara, California, Nvidia has a market capitalization of $5.46 trillion. What started as a computer graphics chip manufacturer is now an unparalleled AI infrastructure platform provider. The company produces the industry's leading GPUs, networking components, AI accelerators, software stack and full-rack systems, serving as a cornerstone of hyperscaler AI deployments. Nvidia is now valued as one of the largest stocks in the world — and arguably the most important supplier in the compute ecosystem.

Nvidia is experiencing yet another rally in shares. The price of NVDA stock reached a fresh all-time high of $236.54 on May 14, now up roughly 75% from the 52-week low. Over the past five days, NVDA stock has managed to gain about 5%. Despite this rise, however, Nvidia has lagged some peers recently. According to Wolfe Research, this “relative underperformance” is driven more by visibility, citing a lack of clarity in regard to the company's 2027 revenue outlook.

www.barchart.com

www.barchart.com NVDA stock is richly valued today. Currently, the stock trades at a forward price-to-earnings (P/E) ratio of 30 times and a price-to-sales (P/S) ratio of 26.4 times. Although these numbers seem rather expensive, Nvidia has a stellar profitability metric. The company has a profit margin of 55.6% and a 97.37% return on equity. Furthermore, the P/E-to-growth (PEG) ratio of 0.74 times implies that Nvidia has more upside than downside ahead.

Nvidia Surged Thanks to Inference and Agentic AI Boom

Nvidia's most recent quarterly report proved why the company is seen as the backbone of the AI infrastructure trade. During Q4 fiscal 2026, Nvidia recorded $68.1 billion in revenue, marking a year-over-year (YOY) rise of 73% and beating analyst consensus estimates. Furthermore, diluted EPS jumped 82% to $1.62 while net income rose to $39.5 billion on a non-GAAP basis, up 79% YOY.

The most exciting part of the report was the acceleration in Nvidia's data-center business. Revenue for the segment soared to a record $62.3 billion, which marked a YOY increase of 75% and amounted to more than 91% of total revenue. Demand for Blackwell systems grew sharply during the quarter as hyperscalers secured compute capacity aggressively. Finally, Nvidia maintained impressive profitability in Q4, with non-GAAP gross margins reaching 75.2%.

On the earnings call, CEO Jensen Huang noted that an "agentic AI inflection point has arrived." As per management commentary, enterprise adoption of AI agents has increased at a far quicker pace than many had expected.

Nvidia further highlighted the significance of Blackwell systems and the future of Vera Rubin. Wolfe Research believes that the latter is not yet reflected in Nvidia's 2027 consensus, although NVDA stock initially fell post-earnings due to worries around expectations. Thanks to hyperscalers' aggressive capex spending plans, however, sentiment quickly turned positive again because, as Wolfe Research noted, "hyperscalers simply have no choice but to spend" to avoid getting left behind. Nvidia will release its Q1 fiscal 2027 earnings on May 20.

What Do Analysts Think About Nvidia?

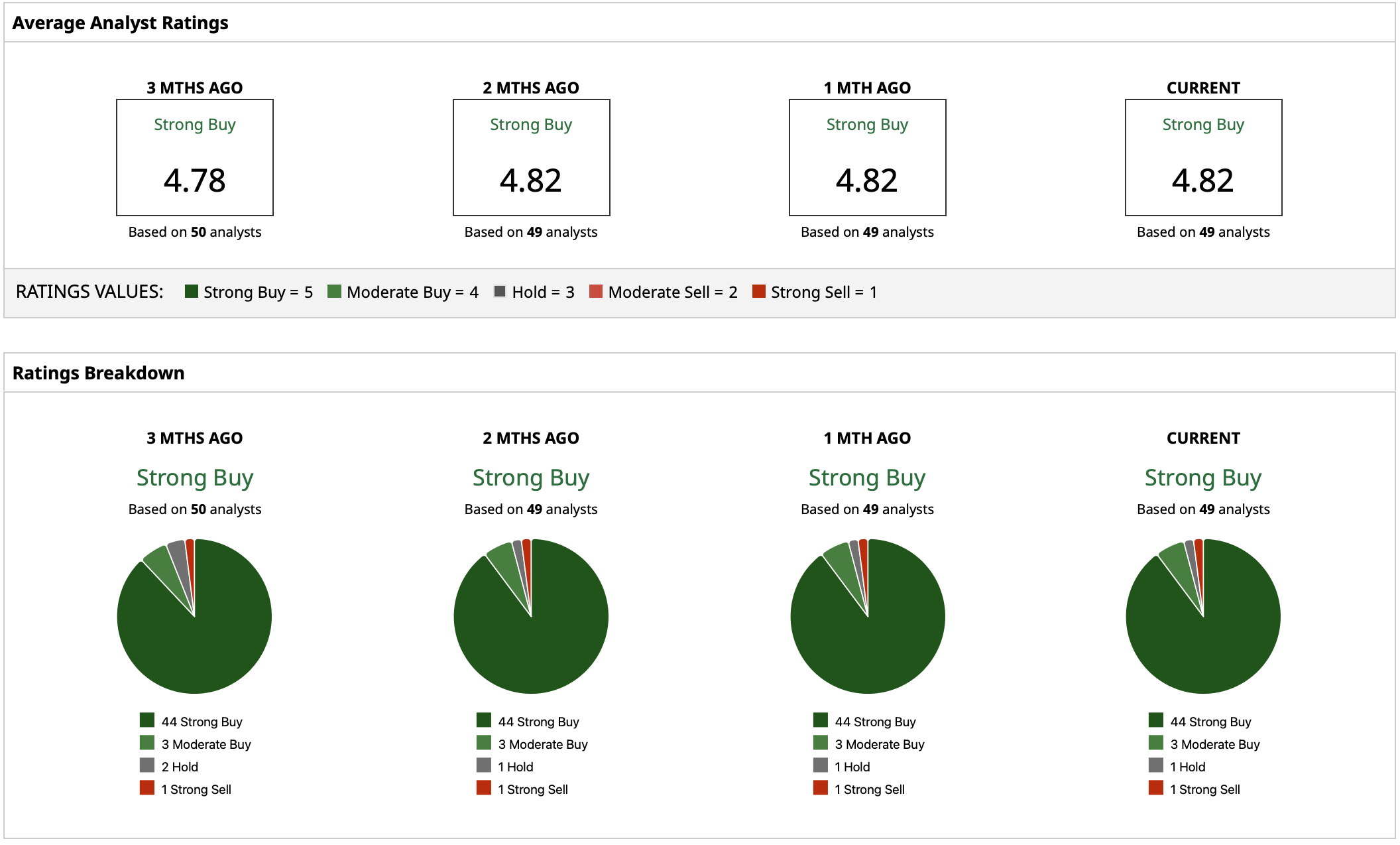

Nvidia currently carries a “Strong Buy” consensus rating. The mean price target stands at $273.16, representing potential upside of roughly 21% from current levels. Meanwhile, the Street-high target of $380 implies significant potential upside of 69% from here — if Nvidia can successfully expand its AI dominance deeper into inference, networking, and full-stack AI infrastructure deployments over the next several years.

www.barchart.com

www.barchart.com On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Microsoft Stock Is an AI Bargain That Investors Are Missing Nvidia’s AI Lead Is Back in Focus as Wolfe Research Doubles Down A $1.5 Trillion Reason to Buy Taiwan Semi Stock Here