Cloud storage company Dropbox (DBX) recently announced that Ashraf Alkarmi will become the new CEO of the company. Succeeding co-founder Drew Houston, Alkarmi will serve as co-CEO with Houston for a period before taking over as the sole chief executive.

With prior experience at Amazon (AMZN) and Meta Platforms (META), Alkarmi previously occupied the role of Senior Vice President of Dropbox Core Products. In that position, he was responsible for Dropbox Sign, DocSend, and more, as well as emphasized artificial intelligence (AI) initiatives.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

So, where does Dropbox stand as an investment now? Let's take a closer look.

About Dropbox

Founded in 2007, Dropbox is one of the pioneers of consumer cloud storage and file synchronization. It provides a myriad of storage and related services such as cloud file storage, file sharing and synchronization, collaboration tools, e-signatures, document workflows, and AI productivity tools. Valued at a market capitalization of $6.1 billion, DBX stock is down roughly 3% on a year-to-date (YTD) basis.

Notably, Alkarmi's stint at Dropbox started in November 2024, and since then, the company's performance has been stable. However, growth has been elusive, with not only the share price but also revenue remaining relatively unchanged.

However, some of the strategic moves led by Alkarmi may have set the company up for a much brighter future. For instance, Alkarmi has been the internal champion for aggressively integrating AI into Dropbox's architecture and an advocate for tools like Dropbox Dash, an AI-powered universal search tool that integrates with third-party platforms like Alphabet's (GOOGL) Google Workspace and Salesforce's (CRM) Slack to help users intelligently manage files.

www.barchart.com

www.barchart.com How Will Dropbox Protect Its Turf?

To compete with the cloud giants, Dropbox is actively repositioning from a storage-centric model to a platform that enhances workflow efficiency through AI-driven insights. Its key asset in this fight is neutrality. Unlike Google or Microsoft (MSFT), Dropbox does not use customer data for ad targeting, and its non-competing stance gives users confidence in their privacy.

Further, Dropbox's response to Microsoft and Google has specifically been to stay cross-platform, simpler, and more workflow-focused rather than trying to out-feature the giants. It has also broadened its product portfolio to include Dropbox Sign for e-signatures, Replay for video collaboration, and DocSend for document tracking, converting the platform into a multi-product productivity suite with vertical add-ons aimed at sales teams, legal departments, HR, and operations groups. The logic here is that a user who depends on three Dropbox products is far less likely to leave than one who only uses cloud storage.

Finally, at the core of the company's AI strategy is Dash, a product that Alkarmi has spearheaded. In practical terms, Dash functions as a universal search layer that works across Dropbox, Google Drive, OneDrive, Slack, Notion, Salesforce, and other tools, pulling everything into a single search bar. Notably, Dash is powered by multiple machine learning technologies and generative AI, offering advanced filtering capabilities, granular access controls, and features that can summarize content, answer questions, surface insights, and generate drafts. The underlying architecture uses retrieval-augmented generation (RAG), which allows Dash to combine real-time retrieval of a company's own content with large language model capabilities, making responses contextually accurate rather than generic.

However, large-scale adoption remains an issue. Management itself has indicated during earnings calls that the initial focus for Dash is driving adoption rather than immediate revenue generation, suggesting a longer-term payoff timeline. That means the core business will have to hold together while the AI bet plays out.

A Steady Q1

Dropbox's results for the first quarter may not inspire much confidence when it comes to growth. Yet, a double beat is certainly not something to scoff at.

While revenues went up marginally on a year-over-year (YOY) basis to $629.5 million, earnings grew more than 8% to $0.76 per share. Notably, not only was this higher than the consensus estimate of $0.70 per share, it was also the eighth consecutive quarter of an earnings beat from the company. However, were expectations low for the period? That is something investors should ask themselves at a time when cloud storage is dominated by giants like Amazon, Microsoft, and Alphabet.

Two key operating metrics portrayed mixed signals for Dropbox. While paying users dropped to 18.09 million from 18.16 million in the prior year, average revenue per user went up to $141.18 from $139.26.

Net cash from operating activities climbed to $204.5 million in Q1 2026 from $153.8 million in Q1 2025. Overall, Dropbox ended the quarter with a cash balance of $1.21 billion.

Meanwhile, DBX stock trades at undervalued levels. With a forward price-to-earnings (P/E) ratio, price-to-sales (P/S) ratio, and price-to-cash flow (P/CF) ratio of 12.4 times, 2.4 times, and 8.6 times, its valuation metrics are all lower than the respective sector medians. However, growth seems to be the hindrance for the company again; analysts' forward projections are for a revenue decline of less than 1% in 2026, while full-year earnings are expected to grow by about 7%.

What Do Analysts Think of Dropbox Stock?

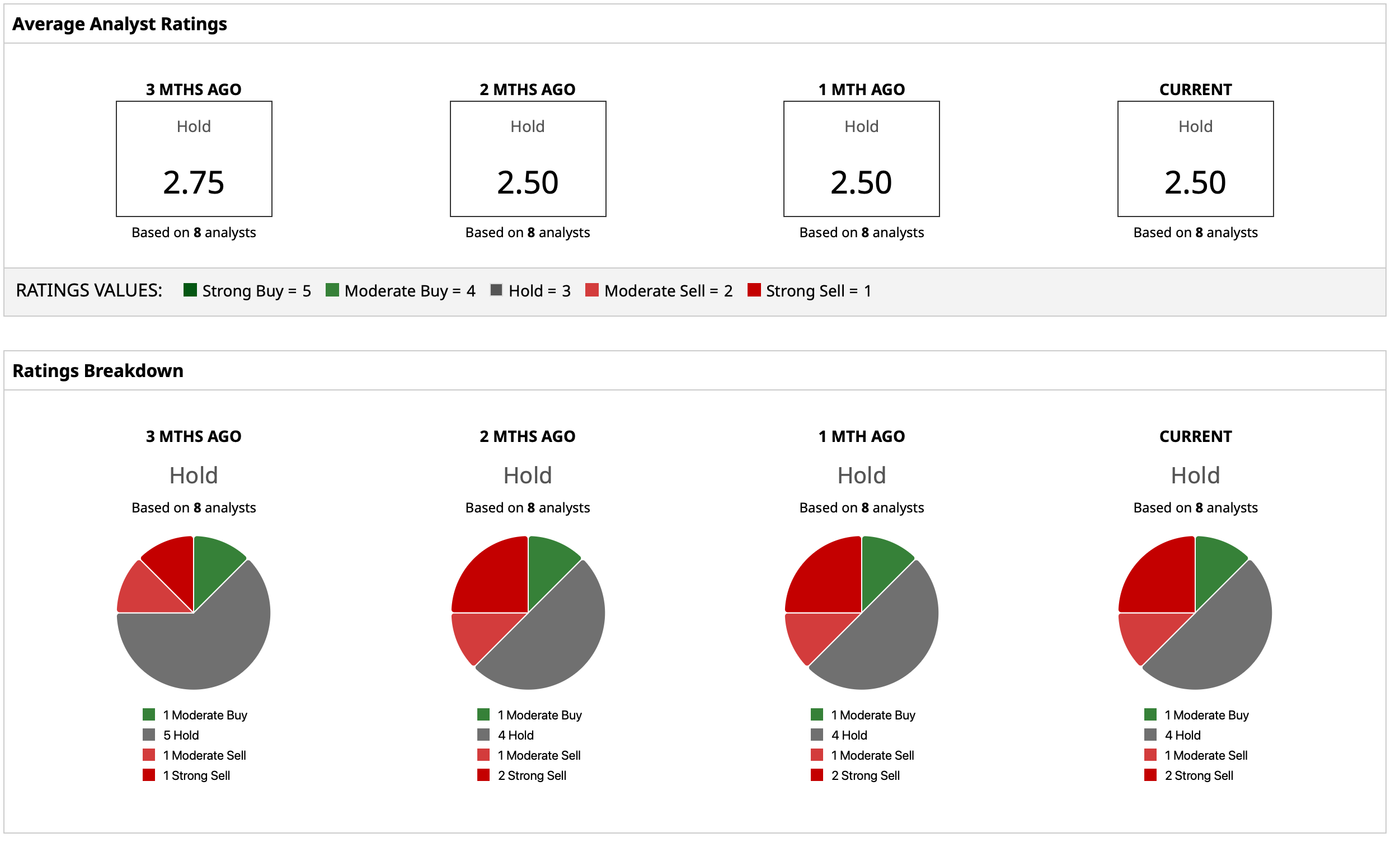

Analysts have a consensus “Hold” rating for DBX stock. The mean target price of $27.20 indicates potential upside of just 1% from current levels. Meanwhile, the Street-high target of $32 suggests 19% potential upside from here. Out of eight analysts covering the stock, one has a “Moderate Buy” rating, four have a “Hold” rating, one has a “Moderate Sell” rating, and two analysts have a “Strong Sell” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Wedbush Just Set a New Street-High Price Target of $325 on Palo Alto Networks. What This Means for PANW Stock. Billionaire Mark Cuban Asks Why Insurance Companies Pay $2,500 for an MRI When ‘a Center Down the Street’ Only Charges $350 Dropbox Gets A New CEO. The Payoff for DBX Stock Could Take a Long Time. Micron Stock Is Trading at 42x Trailing Earnings. Analysts Say That’s Still Cheap.