If the AI chip race were the box office, then the undisputed leaders of it have been Nvidia (NVDA), AMD (AMD), and Broadcom (AVGO). However, just like in the movies where a forgotten star of yesteryear suddenly makes an impactful comeback, Intel (INTC) is hogging the limelight like there is no tomorrow.

With backing from the United States government and led by an able industry veteran in Lip-Bu Tan, Intel's shares have been on a roll. And now, adding to the good times for the company is Apple (AAPL). It is believed that the consumer electronics major is contemplating manufacturing its processors in the U.S., and Intel could be one of the potential partners. On the back of this news, shares of Intel ended markedly higher in yesterday's trading session by 12.92%. The stock has rallied by 456.57% over the past 52 weeks.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com So, with Apple potentially added to its roster of clients again, is that another reason to insert Intel into investors' portfolios, or should caution be exercised?

Impactful Q1

In my last analysis of Intel, I made a point about how Intel's financials were improving, but not quite there. Well, the results for Q1 2026 dispelled some of those fears with a strong showing. Notably, both revenue and earnings surpassed Street estimates.

Revenues went up by 7% from the previous year to $13.6 billion, powered by the Data Center and AI (DCAI) and Foundry segments. While the DCAI segment grew by 22% on a YOY basis to $5.1 billion, the Foundry segment also witnessed a solid growth rate of 16% to $5.4 billion. However, Intel's biggest revenue generator, the Client Computing Group (CCG), was up by just 1% in the same period, coming in at $7.7 billion, reflecting supply constraints and a mature PC market.

Meanwhile, non-GAAP earnings more than doubled to $0.29 per share, comfortably outpacing the consensus estimate of $0.02 per share. Further, this was the third consecutive quarter of earnings beat from the company.

For Q2 2026, the company expects revenue to be in the range of $13.8 billion to $14.8 billion and non-GAAP EPS of $0.20. Street expectations for the same are $14.39 billion and $0.21 per share, respectively.

Net cash from operating activities also increased to $1.1 billion from $813 million in the year-ago period. Overall, Intel ended Q1 2026 with a cash balance of $17.7 billion, much higher than its short-term debt levels of about $2 billion.

However, Intel continues to trade at a premium to its sector medians as well as its own 5-year averages. Its forward price-to-earnings, price-to-sales, and price-to-cash flow of 100.02 times, 9.28 times, and 38.7 times are all well above the sector medians of 55.17 times, 2.64 times, and 12.49 times, respectively.

Agentic AI Phase Can Be Intel's

As AI infrastructure grows more intricate and the demands placed upon it continue to multiply, Intel sees a meaningful revival of interest in the CPU taking shape. The reasoning stems from a fundamental shift in how AI workloads are being structured. As applications increasingly incorporate AI at their core, the CPU is being asked to carry a far greater burden than it once did. It is no longer simply contributing raw compute power to the equation.

Instead, it has assumed the role of the orchestration and control layer sitting atop the entire AI stack, coordinating and directing the broader infrastructure beneath it. This is the context in which Intel's Xeon processor line is experiencing a pickup in demand tied directly to AI infrastructure buildouts, a trend that is being reinforced by a growing list of notable partnerships. Among them is a collaboration with Alphabet (GOOG) (GOOGL) spanning AI and cloud workloads, as well as Tesla's (TSLA) stated intention to leverage Intel's forthcoming 14A process node for its own computing ambitions.

And with its prowess in the AI CPU server segment, Intel has a golden opportunity to make hay in the agentic AI sunshine. For years, the GPU was the undisputed center of gravity in AI data centers, with CPUs playing a supporting, almost afterthought role. In a traditional AI training setup, one CPU was needed for every four to eight GPUs. But as workloads shift toward inference and agentic AI, that ratio is already compressing, moving from 1:8 to 1:4, and Intel's own management believes it could eventually converge to 1:1, or even tip further in favor of CPUs.

Intel is already translating this thesis into concrete wins. At Nvidia's GTC 2026 conference, Intel announced that its Xeon 6 processors will serve as the primary CPU for NVIDIA's next-generation flagship AI server, the DGX Rubin NVL8, handling task orchestration, memory management, scheduling, and data transfer to GPU accelerators. So, the world's dominant AI hardware company chose Xeon as the brain of its most important agentic AI platform.

Also, Intel's Xeon 6 delivers over 50% faster LLVM compilation times compared with Arm-based server CPUs and up to 70% faster vector database performance compared with available x86-based offerings, which matters enormously for coding agents and tool-heavy agentic workflows. Meanwhile, the supply side tells its own story. Server CPU lead times are currently around the six-month mark, server CPU prices have risen 10% to 20% since March, and analysts expect another round of increases of 8% to 10% in the second half of 2026. Intel is supply-constrained, not demand-constrained, and that is a fundamentally different and a far more comfortable problem to have.

However, Intel's competitive story in 2026 and beyond essentially rests on one foundation - the Intel 18A process node. Intel's 18A combines RibbonFET gate-all-around transistors with PowerVia backside power delivery, representing the most advanced semiconductor manufacturing capability produced entirely in the U.S. Moreover, Intel 18A is the first process in the industry to implement backside power delivery, a technology that boosts efficiency by moving power circuitry to the back of the chip.

Beyond products, Intel's foundry ambitions may be the most underappreciated part of the story. The 18A node is the product Intel is selling to Apple, Amazon, and Tesla's Terafab, and every company that has signed or is negotiating a foundry agreement. If those relationships convert into volume contracts, Intel's foundry business transforms from a money-losing drag into a genuine second revenue engine. Intel also recently launched Crescent Island, a dedicated inference accelerator, and has previewed Jaguar Shores, a rack-scale computing platform designed for the AI data center of the late 2020s, signaling that it is no longer willing to concede the accelerator market entirely to NVIDIA and AMD.

Analyst Opinion on INTC Stock

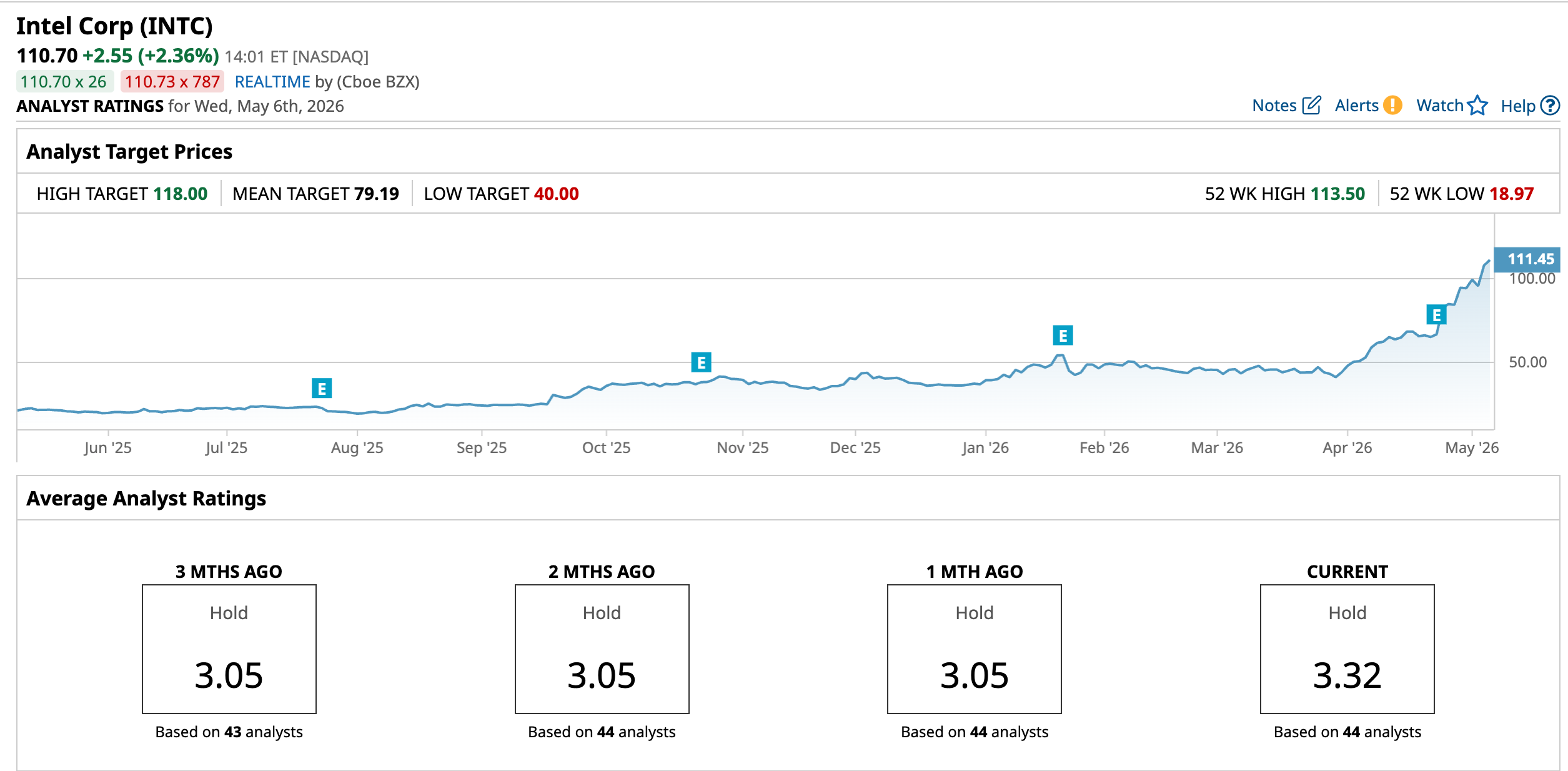

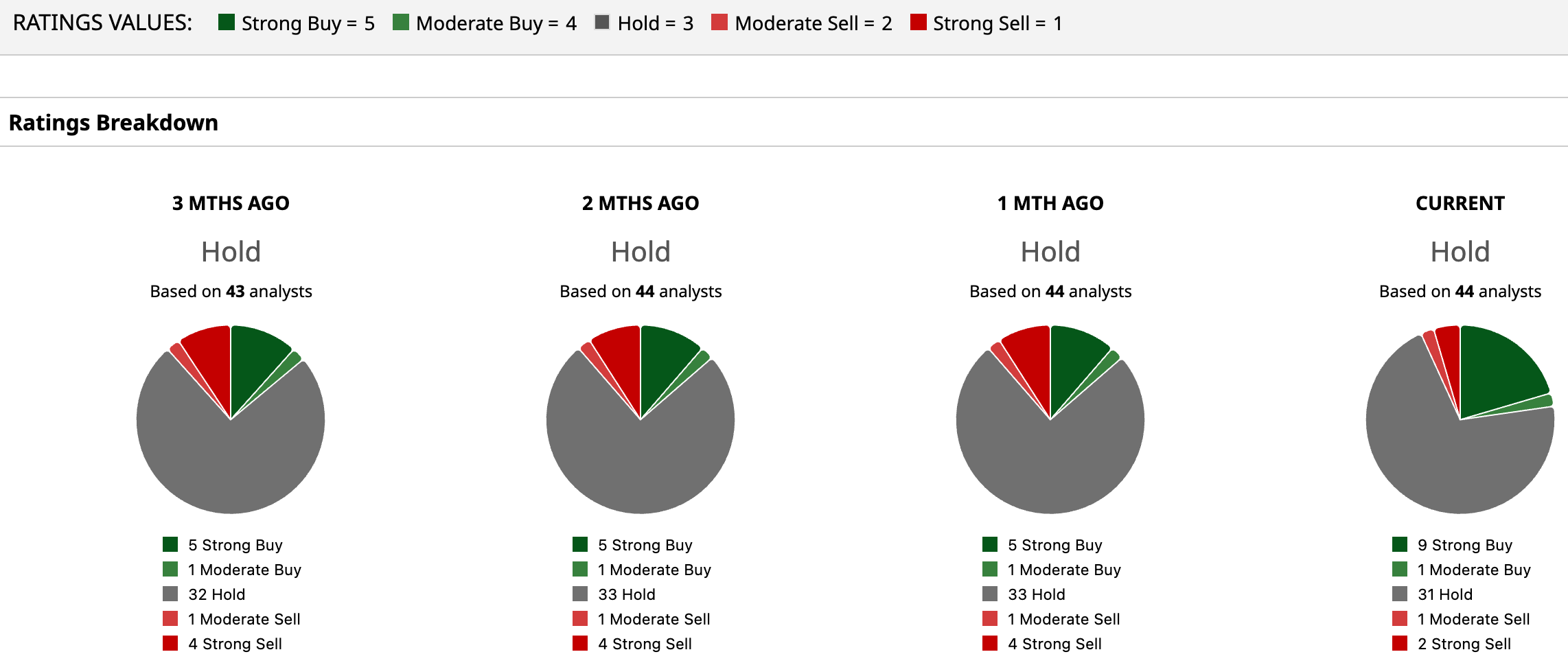

Considering all, analysts have attributed to INTC stock a consensus rating of “Hold.” The mean target price of 79.19 has already been surpassed, whereas the Street-high target price of $118 denotes an upside potential of 6.6% from current levels. Out of 44 analysts covering the stock, nine have a “Strong Buy” rating, one has a “Moderate Buy” rating, 31 have a “Hold” rating, one has a “Moderate Sell” rating, and two have a “Strong Sell” rating.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Intel Stock Just Hit New Record Highs. This Time, Apple Gets All the Credit. AMD’s AI Moment May Be Bigger Than Nvidia Investors Realize You May Not Know This 1 China-Focused Chip Stock but Seaport Global Analysts Can’t Get Enough Shopify's Strong Q1 FCF Growth Sparks Unusual Buying of SHOP Calls