Shares of Selective Insurance Group, Inc. SIGI closed at $84.78 on Friday, near its 52-week high of $91.63. This proximity underscores investor confidence. It has the ingredients for further price appreciation.

The stock is trading above the 50-day and 200-day simple moving averages (SMA) of $79.66 and $80.47, respectively, indicating solid upward momentum. SMA is a widely used technical analysis tool to predict future price trends by analyzing historical price data.

Image Source: Zacks Investment Research

SIGI is an Outperformer

Shares of Selective Insurance have gained 1.3% in the year-to-date period, outperforming the Finance sector’s growth of 0.2% and the industry’s decline of 12.2%.

Selective Insurance has outperformed its peers, including Axis Capital Holdings Limited AXS, NMI Holdings Inc. NMIH and W.R. Berkley Corporation WRB. Shares of AXS, NMIH and WRB have lost 7.2%, 4.7% and 6.3%, respectively, in the year-to-date period.

Image Source: Zacks Investment Research

SIGI’s Growth Projection Encourages

The Zacks Consensus Estimate for Selective Insurance’s 2026 earnings per share indicates a year-over-year increase of 5.1%. The consensus estimate for revenues is pegged at $5.51 billion, implying a year-over-year improvement of 3.4%. The consensus estimate for 2027 earnings per share and revenues indicates an increase of 13.8% and 3.4%, respectively, from the 2026 estimates.

Selective Insurance has an impressive Growth Score of B. This style score helps analyze the growth prospects of a company.

Optimistic Analyst Sentiment for SIGI

Two of the five analysts covering the stock have raised estimates for both 2026 and 2027 over the past 30 days. Thus, the Zacks Consensus Estimate for 2026 and 2027 earnings has moved north 0.6% and 0.5%, respectively, over the past 30 days.

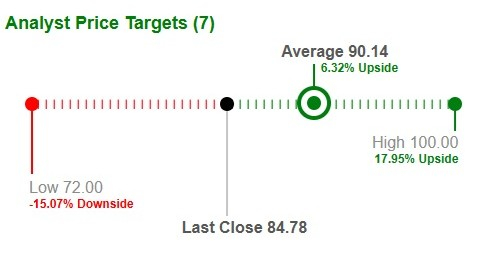

Target Price Reflects Potential Upside

Based on short-term price targets offered by seven analysts, the Zacks average price target is $90.14 per share. The average indicates a potential 6.3% upside from the last closing price.

Image Source: Zacks Investment Research

Factors Favoring SIGI Stock

Exposure growth, solid retention rates and higher new business gains in standard commercial and excess and surplus (E&S) lines should drive premium growth.

Steady betterment of premiums, improved net investment income and higher other income have resulted in top-line improvement.

The E&S Lines segment of Selective Insurance is likely to improve because of renewal pure price increases, higher direct new business and favorable E&S lines marketplace conditions.

Given impressive investment results, Selective Insurance expects after-tax net investment income of $465 million in 2026. Strong and reliable returns from its growing fixed-income portfolio, supported by higher returns from its non-fixed income portfolio, are likely to drive the metric.

Selective Insurance flaunts a sound capital structure and remains committed to enhancing shareholders' value while improving its financial strength and underwriting capabilities. As of March 31, 2026, stockholders’ equity was $3.6 billion, and the net premiums written to policyholders’ surplus ratio was 1.35x, indicating capacity to support underwriting and geographic expansion. Debt-to-total capitalization was 20.1% at quarter-end, and long-term debt was $901 million, which management has kept stable since year-end 2025. This balance supports continued investment in underwriting, claims and technology capabilities while maintaining room for shareholder returns.

Impressive Wealth Distribution

Selective Insurance continues to return capital through dividends and repurchases while keeping flexibility for underwriting and investment opportunities. From a valuation perspective, the stock’s multiples remain below broader market averages, and consensus expectations imply relatively steady earnings power, with 2026 EPS estimated at $7.45 and 2027 EPS estimated at $8.70. This combination supports long-term total return potential, even as near-term premium growth is moderated by underwriting choices.

SIGI’s Favorable Return on Capital

Return on equity in the trailing 12 months was 13.7%, better than the industry average of 7.3%. This highlights the company’s efficiency in utilizing shareholders’ funds.

Conclusion

While Selective Insurance remains well-positioned to gain from strong renewal, fuel price increases, favorable E&S lines marketplace conditions and higher income earned on fixed-income securities portfolio, the specific challenges facing the company, like exposure to catastrophe loss and escalating expenses, cannot be ignored.

SIGI also has a VGM Score of A. Stocks with a favorable VGM Score are those with the most attractive value, best growth and most promising momentum compared with peers.

SIGI should benefit from favorable growth estimates, higher return on capital and prudent capital deployment. It is, therefore, wise to hold on to this Zacks Rank #3 (Hold) stock at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

W.R. Berkley Corporation (WRB): Free Stock Analysis Report

Axis Capital Holdings Limited (AXS): Free Stock Analysis Report

Selective Insurance Group, Inc. (SIGI): Free Stock Analysis Report

NMI Holdings Inc (NMIH): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).