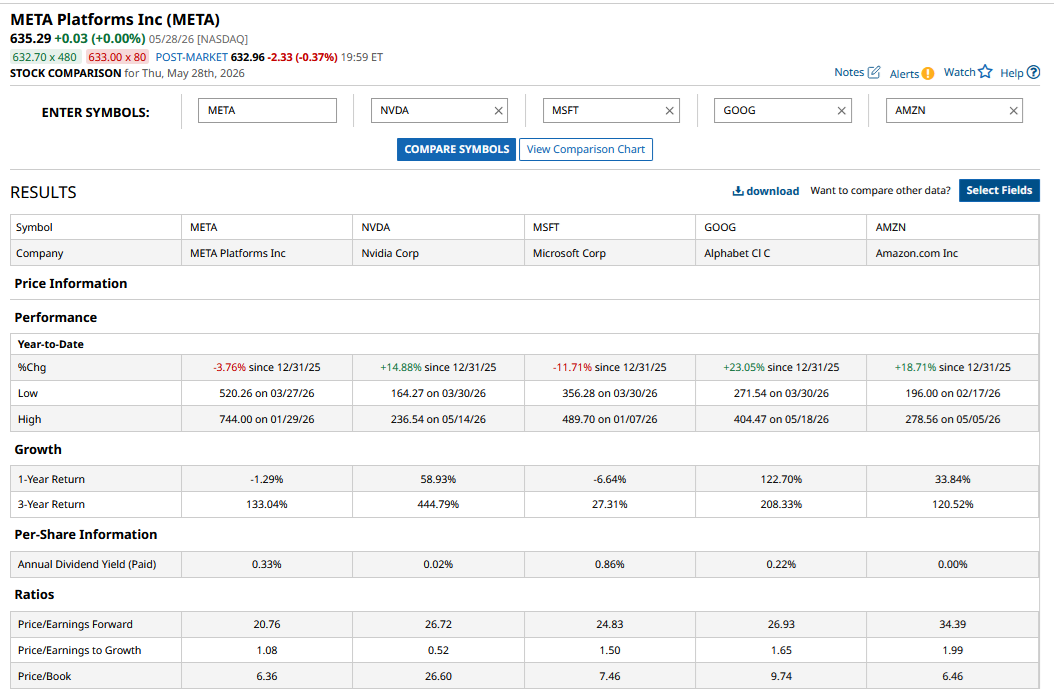

With a year-to-date (YTD) loss of 4.66%, Meta Platforms (META) is underperforming the markets this year. Among its Magnificent 7 peers, only Microsoft (MSFT) has fared worse this year. Alphabet (GOOG) (GOOGL) is, meanwhile, the best-performing among the lot, a position the Google parent also held last year.

The divergence in price action among Big Tech companies can largely be attributed to market perceptions of their artificial intelligence (AI) initiatives. Alphabet proved critics wrong and is literally firing on all cylinders. The company’s core search and digital advertising business has managed to protect its turf from upstarts like OpenAI and its ad business is growing way faster than its two bigger competitors, namely Microsoft and Amazon (AMZN).

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.comAI Has Helped Fuel Meta’s Revenue Growth

As for Meta, its ad business has been doing remarkably well, and the company’s revenues rose by an impressive 33% year-over-year in Q1 2026, the highest growth since 2021. AI-powered personalized ads have been a key driver of that growth. For context, only Nvidia (NVDA) reported a higher growth in the most recent quarter, even though the reporting period is not similar for the two companies.

Other hyperscalers have sprawling cloud operations whose growth has been turbocharged due to strong demand for AI. The growing cloud revenues help tech giants validate their AI capex to some extent. Meta, however, does not have an in-house cloud business and has been struggling to justify its ever-rising capex, which stood between $125 billion and $145 billion at the last count. At the top end of that range, this year Meta would spend twice as much as it did in 2025, and while capex budgets of other hyperscalers are also facing scrutiny, markets have been particularly harsh on Meta amid concerns over the company’s ability to monetize these investments.

Meanwhile, Meta has a plan to monetize its AI capex and is launching new subscriptions. Additionally, CEO Mark Zuckerberg has touted the possibility of launching a cloud computing business. Let’s examine what these initiatives would mean for Meta stock, which is trading around 20% below its all-time highs even as the broader markets have been hitting record highs almost daily.

www.barchart.com

www.barchart.comMeta Rolls Out Subscriptions

So far, Meta doesn't have any major paid subscription business apart from Meta Verified and the ad-free subscriptions in Europe. The latter was launched to comply with regulatory requirements and give users the option to opt out of personalized ads by paying a subscription fee. Meta does not publicly disclose subscriber figures or subscription revenues, but the numbers are not significant, as they are part of the “Other” segment, which accounted for less than 2% of its total Q1 revenues.

Meta is now trying another shot at subscriptions, and this time around, it is not a regulatory turnaround but a conscious business decision. The company is rolling out subscriptions for Instagram, Facebook, and WhatsApp. The subscribers would be getting extra features like profile customization and super reactions by shelling out a fee, which is $3.99 per month for Facebook and Instagram, and $2.99 per month for WhatsApp.

Additionally, the company is testing two subscriptions for its AI offerings and has priced Meta One Plus at $7.99 a month and Meta One Premium at $19.99 a month. Meta is spending billions of dollars every year on building AI models, and these subscriptions would help it monetize and justify its capex.

Will Meta’s Subscriptions Be Successful?

Meta owns the biggest social media apps, and subscriptions were the next logical step for the company. I believe the bulk of Meta’s initial over 3.5 billion daily active users won’t opt for the subscription. However, going forward, the company might increase the features it provides to subscribers while limiting them for non-paying members, which should cajole more users to opt for a subscription.

For AI offerings, Meta is following the trajectory of other tech giants, which charge for premium features. Over the long term, subscriptions can be a key driver of Meta’s growth and should also help support its valuations as markets love the recurring revenues they bring.

Should You Buy Meta Stock?

Currently, Meta trades at a forward price-to-earnings (P/E) multiple of 20.7x, which is the lowest among Mag 7 peers. Consensus estimates call for Meta’s earnings per share (EPS) to slightly increase this year. The company does not provide EPS guidance but is optimistic about its 2026 operating income being higher than the last year. Meta’s P/E should be seen in the light of its current depressed earnings as well as the continued losses in the Reality Labs segment. However, the company's earnings are expected to improve from next year, with analysts modeling over a 19% rise in its EPS. I find Meta's valuations quite attractive, and the launch of subscriptions only strengthens my bullish bias for the stock.

On the date of publication, Mohit Oberoi had a position in: META , GOOG , MSFT , AMZN , NVDA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Meta Has a Plan to Monetize Its AI Investments. Its Underperforming Stock Needs It Badly. Jobs Data, Tech Earnings and Other Key Things to Watch this Week After a 13% Selloff, Wolfspeed Now Trades at Steep Discounts. Don’t Be Fooled into Buying the Dip. Why Warren Buffett Hasn’t Sold Coca-Cola Stock for Over 30 Years