Nebius (NBIS) stock is inching higher ahead of the artificial intelligence (AI) infrastructure firm’s inclusion in the Nasdaq-100 before market open on June 22.

Index inclusion is expected to generate significant mechanical buying pressure from passive funds and exchange-traded funds (ETFs). NBIS is being added alongside Astera Labs (ALAB), CoreWeave (CRWV), Rocket Lab (RKLB), and Teradyne (TER).

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

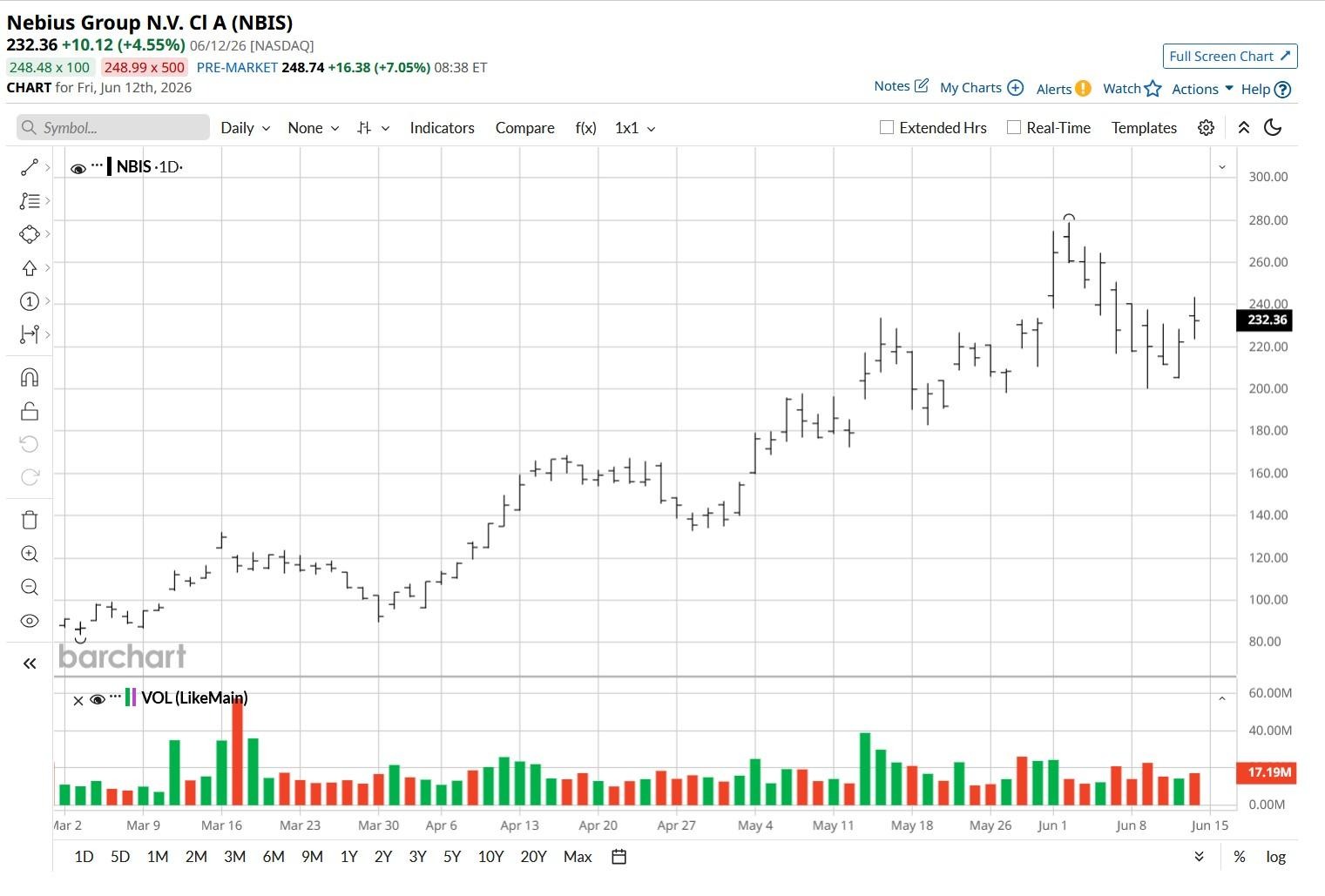

At the time of writing, Nebius stock is up nearly 212% versus the start of this year.

www.barchart.com

www.barchart.comNebius Reported a Solid Q1

NBIS shares’ recent rally reflects both the index inclusion catalyst and extraordinary fundamental momentum, as the company reported Q1 revenue of $399 million, representing a 684% year-over-year increase.

Meanwhile, adjusted EBITDA also swung from a loss to a profit of $129.5 million, demonstrating the company’s rapid path to profitability as an artificial intelligence infrastructure provider.

The bull case is reinforced by a $2.6 billion investment from hedge fund “Situational Awareness”, run by former OpenAI researcher Leopold Aschenbrenner, who acquired a 5.6% stake based on the thesis that physical infrastructure is the true bottleneck for AI advancement.

What Makes NBIS Stock Worth Owning?

Nebius is pursuing an exceptionally aggressive capital expenditure (CAPEX) program of roughly $22.5 billion for 2026 — aimed at expanding data center capacity to as much as 1 gigawatt by year-end.

Major projects include a “gigawatt-scale” AI factory in Pennsylvania, approximately $2.1 billion in U.K. facilities, and a massive complex in Missouri.

The spending is underpinned by contracted revenue, including a $17.4 billion GPU infrastructure deal with Microsoft (MSFT), a $27 billion five-year agreement with Meta (META), and Nvidia’s (NVDA) $2 billion strategic investment.

Beyond raw compute, the company is moving up the value chain through acquisitions of Eigen AI for $643 million and Tavily, forming what management calls a token factory platform for inference optimization.

This strategic pivot positions Nebius to capture higher margins as the AI industry shifts from model training toward real-time inference workloads.

Management has guided for full-year sales of $3 billion at least, with an adjusted EBITDA margin of some 40%, though a temporary margin dip is expected in Q2 before recovery later in the year.

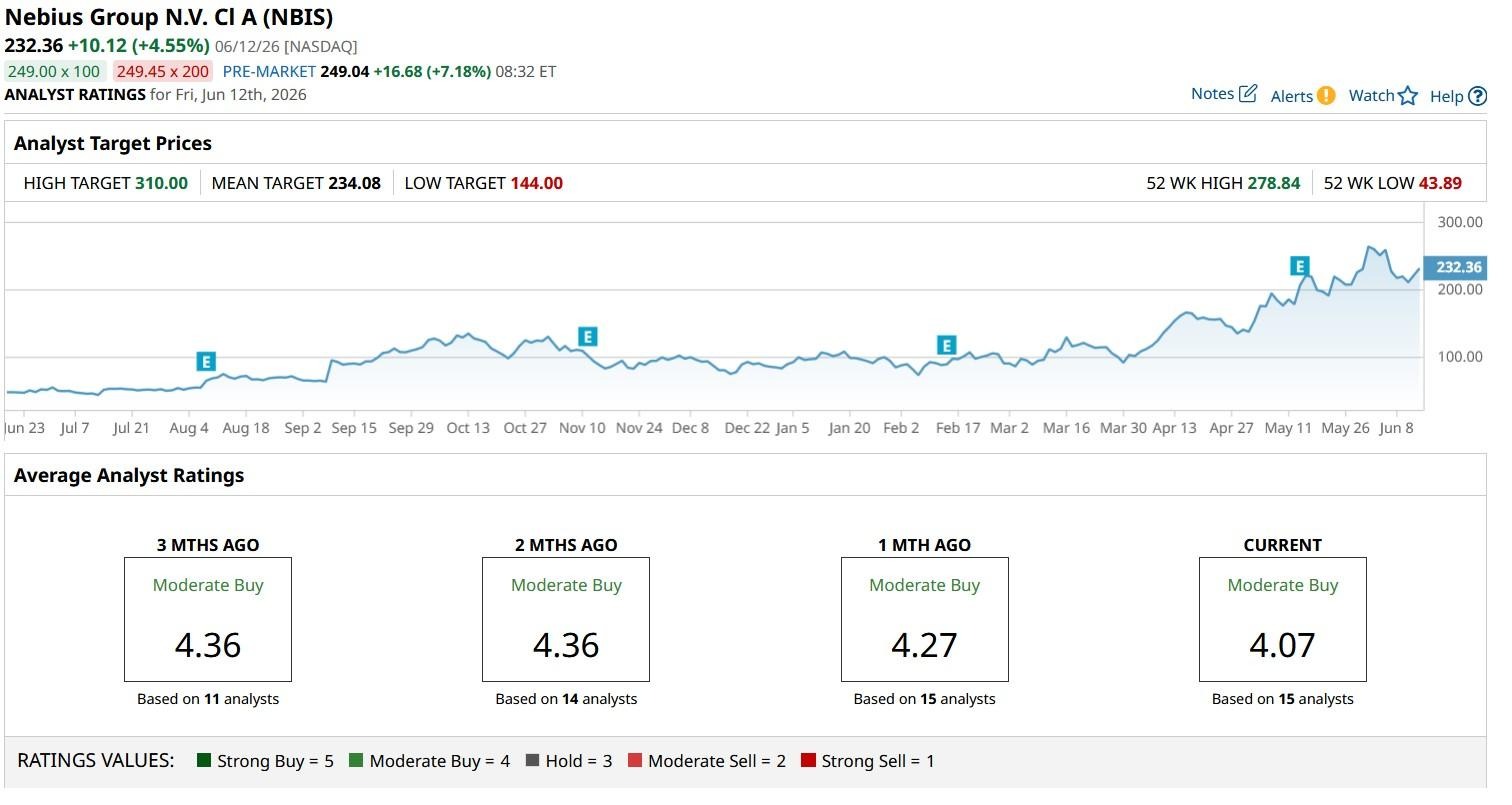

How Wall Street Recommends Playing Nebius Shares

On the flip side, risks are notable as well: insiders have sold NBIS stock worth millions over the past three months, with Morningstar estimating fair value at just $120.

The tension between the huge capital commitment and current revenue creates a binary-outcome dynamic where Nebius either delivers explosive growth or faces the consequences of overbuilding at premium valuations.

Still, analyst sentiment remains strongly positive, with the consensus “Moderate Buy” rating tied to price targets as high as $310 currently, signaling potential upside of about 33% from here.

www.barchart.com

www.barchart.com On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Experts Think Intel Should Raise Capital Right Now, and What It Means for INTC Stock Nebius Stock Gets a Boost From Nasdaq-100 Inclusion. What to Know. Cognizant’s CEO Just Compared This AI Launch to the iPhone Moment. You Should Buy This Rare Undervalued AI Stock. Adobe Stock Is Selling Off Back to 2019 Lows. What Bulls Need to Turn Things Around.