PayPal Holdings (PYPL) may be setting up for a contrarian opportunity. The digital payments giant has fallen sharply in 2026, pushing its shares into deeply oversold territory and making it one of the most oversold stocks in the S&P 500 Index ($SPX). Technical indicators such as the Relative Strength Index (RSI) suggest that selling pressure may have become excessive, with a reading hovering near 30 to 40, a level often viewed as a sign of excessive selling pressure, even as PayPal continues to generate strong cash flow, expand Venmo’s ecosystem, and maintain its position as one of the world’s largest online payments platforms.

While concerns about intensifying competition and cautious management guidance have weighed on investor sentiment, oversold conditions often create attractive entry points for long-term investors willing to look beyond near-term headwinds. So, let’s dig deeper into whether PayPal’s recent weakness represents a value opportunity or a warning sign of deeper challenges ahead.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About PayPal Stock

PayPal is a leading fintech firm that operates a digital payments platform connecting consumers, merchants, and financial institutions across more than 200 markets. It offers a broad array of services, including peer-to-peer transfers, merchant processing, digital wallets, and consumer credit products. PayPal is headquartered in San Jose, California and currently boasts a market cap of $37.5 billion.

PayPal Holdings’ stock has been under significant pressure over the past year, making it one of the weaker performers in the large-cap fintech space.

PayPal shares have declined 40% over the past 52 weeks, reflecting investor concerns about slowing growth, increasing competition in digital payments, and weaker-than-expected guidance. The stock has also fallen 27.2% year-to-date (YTD), significantly underperforming the broader market. Additionally, PayPal is trading about 45.3% below its 52-week high of $79.50, highlighting the extent of the selloff.

The decline accelerated following the company’s first-quarter 2026 earnings report. Although PayPal delivered revenue and earnings that exceeded Wall Street expectations, investors focused on management’s cautious outlook. The stock dropped 7.7% immediately after the report on May 5, extending its broader downtrend.

Despite the sharp pullback, the stock’s steep decline has pushed several technical indicators into oversold territory, leading some investors to view PayPal as a potential contrarian opportunity if the company can stabilize growth and improve investor confidence.

www.barchart.com

www.barchart.com PYPL evidently trades at a discount compared to the sector median and its own historical average at 7.84 times forward earnings. In terms of price-to-sales, it is trading at 1.09 times, which is also significantly down from the average.

Mixed Q1 Performance

PayPal delivered a mixed first-quarter 2026 report on May 5, beating Wall Street’s revenue and earnings expectations while showing accelerating payment volume growth. However, investors focused on management’s cautious outlook and rising investment spending, sending the stock sharply lower following the release.

For the quarter ended March 31, 2026, revenue increased 7% year-over-year (YOY) to $8.4 billion, ahead of analyst estimates. Non-GAAP earnings per share came in at $1.34, up 1% from the prior-year quarter and above the consensus estimate. Total Payment Volume (TPV), rose 11% YOY to $464 billion, reflecting improving momentum across the platform.

Several operating metrics also showed improvement. Venmo TPV grew 14% YOY, marking the sixth consecutive quarter of double-digit growth, while Buy Now, Pay Later (BNPL) volume increased 23%. Pay with Venmo TPV surged 34%, and transaction margin dollars rose 3% YOY. Active accounts increased 1% to 439 million.

The main concern was profitability. Non-GAAP operating income declined 5% YOY to about $1.5 billion, while operating margins contracted as PayPal increased spending on technology modernization, artificial intelligence initiatives, marketing, and branded checkout improvements.

Furthermore, management guided for low-single-digit revenue growth in Q2 2026, a low-single-digit decline in transaction margin dollars, and roughly a 9% YOY decline in non-GAAP EPS. For full-year 2026, PayPal reiterated its outlook, expecting transaction margin dollars to be roughly flat to slightly down and non-transaction operating expenses to rise about 3%, with full-year non-GAAP EPS expected to range from slightly negative to slightly positive growth.

In addition to the financial results, management also announced a broad restructuring initiative, including a plan to generate at least $1.5 billion in gross run-rate cost savings over the next two to three years through AI adoption and operational simplification.

Analysts predict EPS to be $5.30 for fiscal 2026, down slightly YOY, before surging by 9.1% annually to $5.78 in fiscal 2027.

What Do Analysts Expect for PayPal Stock?

Recently, Freedom Broker lowered its price target on PayPal to $60 from $100 but maintained a “Buy” rating.

However, on the other hand, Truist Securities lowered its price target on PayPal to $44 from $45 while maintaining a “Sell” rating after the company’s first-quarter 2026 earnings report.

Plus, William Blair reiterated its “Market Perform” rating on PayPal, remaining cautious. The firm questioned PayPal’s long-term competitive advantages, arguing that Venmo is unlikely to evolve into a true digital banking competitor.

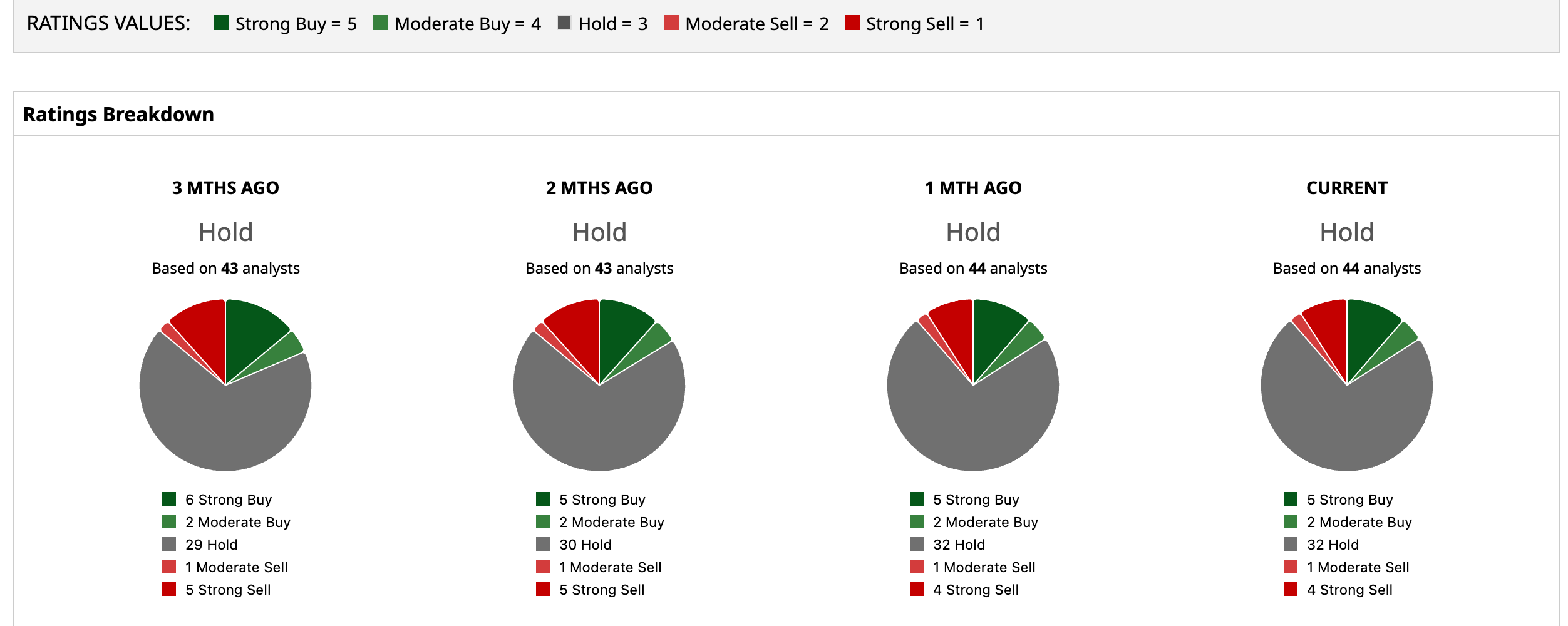

Wall Street remains cautious on PYPL with an overall consensus “Hold” rating. Of the 44 analysts covering the stock, five advise a “Strong Buy,” two suggest a “Moderate Buy,” 32 analysts are on the sidelines, giving it a “Hold” rating, one gives a “Moderate Sell,” and four rate it as a “Strong Sell.”

The average analyst price target for PYPL is $48.30, indicating a potential upside of 11.44%. The Street-high target price of $65 suggests that the stock could rally as much as 50%.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

PayPal Stock Is Deeply Oversold in 2026. How to Play PYPL Here. Why Grok Could Be a Reason to Stay Away from the SpaceX IPO Dear Astera Labs Stock Fans, Mark Your Calendars for June 22 FuelCell Energy Stock Sold Off on Earnings. That Didn’t Stop This Analyst from Setting a New Street-High Price Target.