Arista Networks (ANET) was thrown into the spotlight after releasing its fiscal 2026 first-quarter earnings on May 5, and despite delivering another impressive beat on both revenue and profit, investors still headed for the exits. The networking powerhouse posted results that easily topped Wall Street expectations, yet the market response was brutal. Shares of the hardware and software specialist tumbled more than 13.6% on May 6 as traders focused less on the headline strength and more on what could lie ahead.

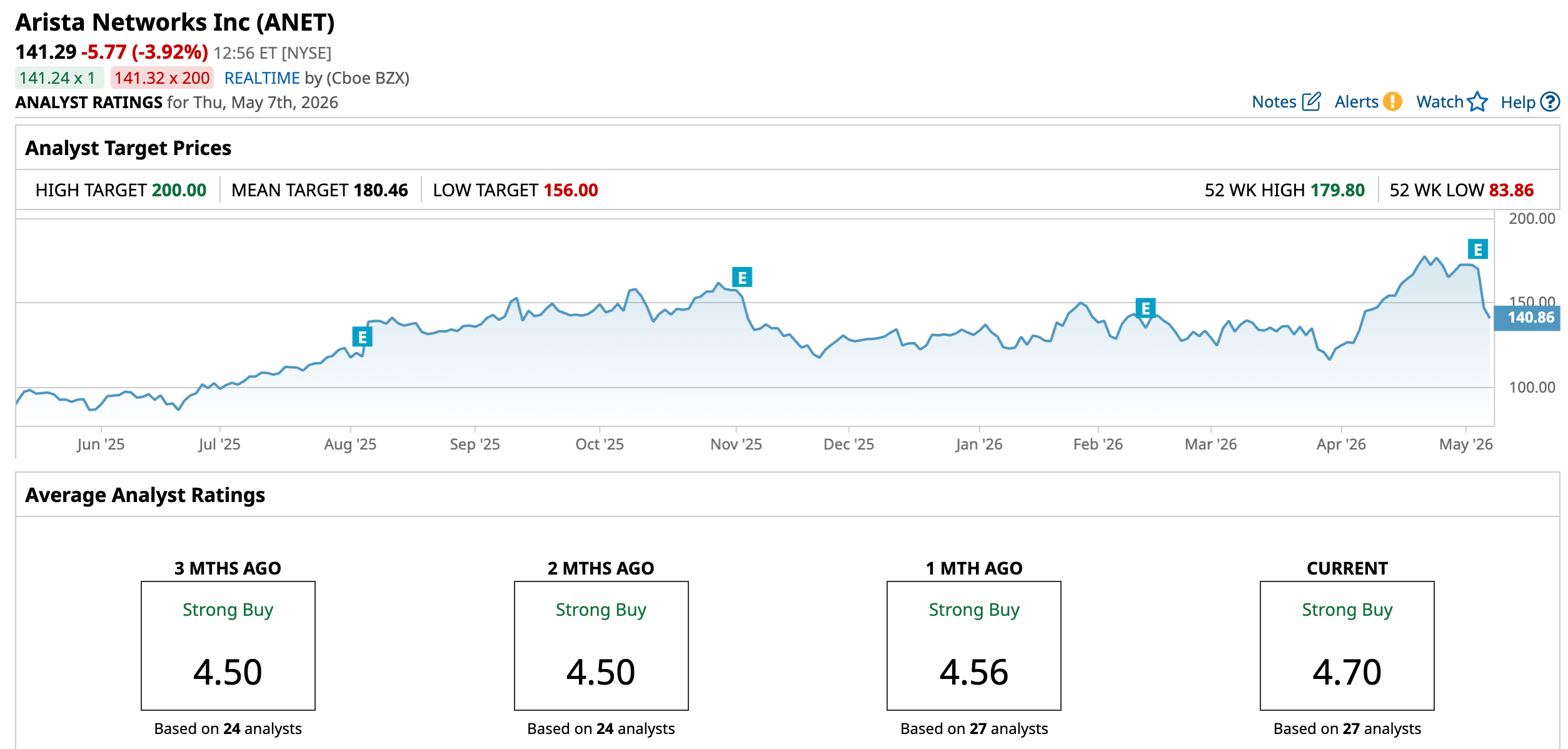

The sell-off appeared to stem from a combination of factors. Margin pressures, a guidance raise that failed to clear the market’s sky-high expectations, and management’s cautious commentary surrounding the supply chain outlook appeared to rattle confidence. Still, the sharp pullback has hardly crushed Wall Street’s confidence in Arista’s long-term story. Many analysts remain bullish on the stock and continue to stand by a Street-high price target of $200, signaling sizable double-digit upside potential from current levels.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

With hyperscalers continuing to pour billions into artificial intelligence (AI) infrastructure and high-speed networking becoming increasingly critical to the AI boom, the recent post-earnings plunge may have created a compelling opportunity for investors willing to look beyond the short-term noise.

About Arista Networks Stock

Arista Networks has established itself as a major player in data-driven, client-to-cloud networking, serving large-scale data center, AI, campus, and routing environments. The company’s award-winning platforms are built around an advanced network operating stack designed to deliver high availability, automation, analytics, agility, and security, capabilities that have become increasingly critical as enterprises and hyperscalers expand their AI and cloud infrastructure.

The company traces its origins back to Arastra, which was founded in 2004, before officially becoming Arista Networks in 2008. Arista later went public under the ticker ANET in 2014 and joined the S&P 500 Index ($SPX) in 2018. Since then, it has grown into a global force in cloud and AI-focused high-performance networking. Supporting that growth is a leadership team widely recognized across the networking industry for its long track record of innovation and technological expertise.

Despite the sharp post-earnings pullback, Arista Networks has still delivered remarkable gains over the past year as the AI infrastructure boom continues to fuel demand for high-performance networking solutions. With a market capitalization of roughly $185.17 billion, ANET stock has surged 63% over the last 12 months, comfortably outperforming the S&P 500 Index, which gained 30.53% during the same period.

The momentum has carried into 2026 as well. Even after the recent bout of volatility, Arista shares remain up 7.54% year-to-date (YTD), staying slightly ahead of the broader market’s 7.37% gain as investors continue to view the company as one of the key beneficiaries of the accelerating AI infrastructure buildout.

www.barchart.com

www.barchart.com Inside Arista Networks’ Q1 Earnings Report

Arista Networks delivered what appeared to be another standout quarter when it released its fiscal 2026 first-quarter earnings on May 5, but the market’s reaction made it clear that investors were expecting even more from one of the biggest beneficiaries of the AI infrastructure boom. While the networking giant comfortably topped Wall Street’s expectations on both revenue and earnings, concerns surrounding margins and supply constraints overshadowed the otherwise impressive performance.

Arista reported first-quarter revenue of $2.71 billion, marking a powerful 35.1% year-over-year (YOY) increase and coming in ahead of analysts’ expectations of $2.62 billion. Profitability also remained strong. Non-GAAP earnings per share climbed 32% YOY to $0.87, easily surpassing the consensus estimate of $0.81. Gross margin for the quarter landed at 62.4%, within management’s guided range of 62% to 63%, although it declined from 63.4% in the prior quarter.

Executives attributed the sequential compression largely to a lower mix of enterprise customer sales during the period. The company’s balance sheet continued to reflect significant financial strength. Arista ended the quarter with approximately $12.35 billion in cash, cash equivalents, and marketable securities. Meanwhile, cash generation remained exceptionally strong, with operating cash flow reaching roughly $1.69 billion during the quarter, the highest quarterly figure in the company’s history.

Still, despite the long list of positives, the stock experienced a sharp sell-the-news reaction as investors shifted their focus toward mounting supply chain challenges and the potential impact on profitability. During the earnings call, management acknowledged that industry-wide shortages continue to persist across critical components, including wafers, silicon chips, CPUs, optics, and memory.

Executives noted that demand currently exceeds supply, forcing the company to absorb elevated procurement costs and make supply-assurance tradeoffs to support customers. Arista added that its operations team has been actively strengthening vendor relationships and entering multi-year purchase agreements to improve supply visibility, though management cautioned that these efforts could continue pressuring margins in the near term.

Looking ahead, Arista issued second-quarter revenue guidance of approximately $2.8 billion, modestly ahead of Wall Street expectations of $2.78 billion. However, investors appeared more focused on the company’s projected operating margin range of 46% to 47%, which implies slight compression from the 47.8% operating margin achieved in the first quarter.

Even so, management struck an optimistic tone on the broader outlook and raised its fiscal 2026 revenue growth forecast to 27.7%, which would translate into approximately $11.5 billion in annual revenue. In addition, the company reiterated its full-year gross margin outlook of 62% to 64%.

How Are Analysts Viewing Arista Networks Stock?

Despite the sharp post-earnings pullback, Wall Street analysts appeared far from ready to give up on Arista Networks. Both J.P. Morgan and Evercore reiterated their bullish ratings and maintained Street-high $200 price targets, signaling continued confidence in the company’s long-term AI-driven growth story. J.P. Morgan acknowledged that ongoing supply constraints could temporarily cap the magnitude of near-term upside, but stressed that the broader growth narrative remains firmly intact.

The firm pointed to sustained hyperscaler demand, including what analysts believe is Microsoft (MSFT) increasingly shifting portions of its AI networking infrastructure from InfiniBand to Ethernet. Analysts also highlighted Arista’s growing traction against white-box competitors, expanding scale-across opportunities, and rising deferred revenue backlog as indicators of strong long-term demand visibility. Meanwhile, Evercore described the company’s first-quarter report as another example of strong operational execution, noting that demand across the AI networking market continues to outpace available supply.

The firm added that Arista likely would have delivered an even larger increase to its full-year outlook if not for ongoing supply chain bottlenecks tied to wafer fabrication shortages and extended component lead times. Even with near-term margin pressures and supply challenges lingering, analysts broadly believe the accelerating AI infrastructure buildout continues to position Arista for strong multi-year growth ahead.

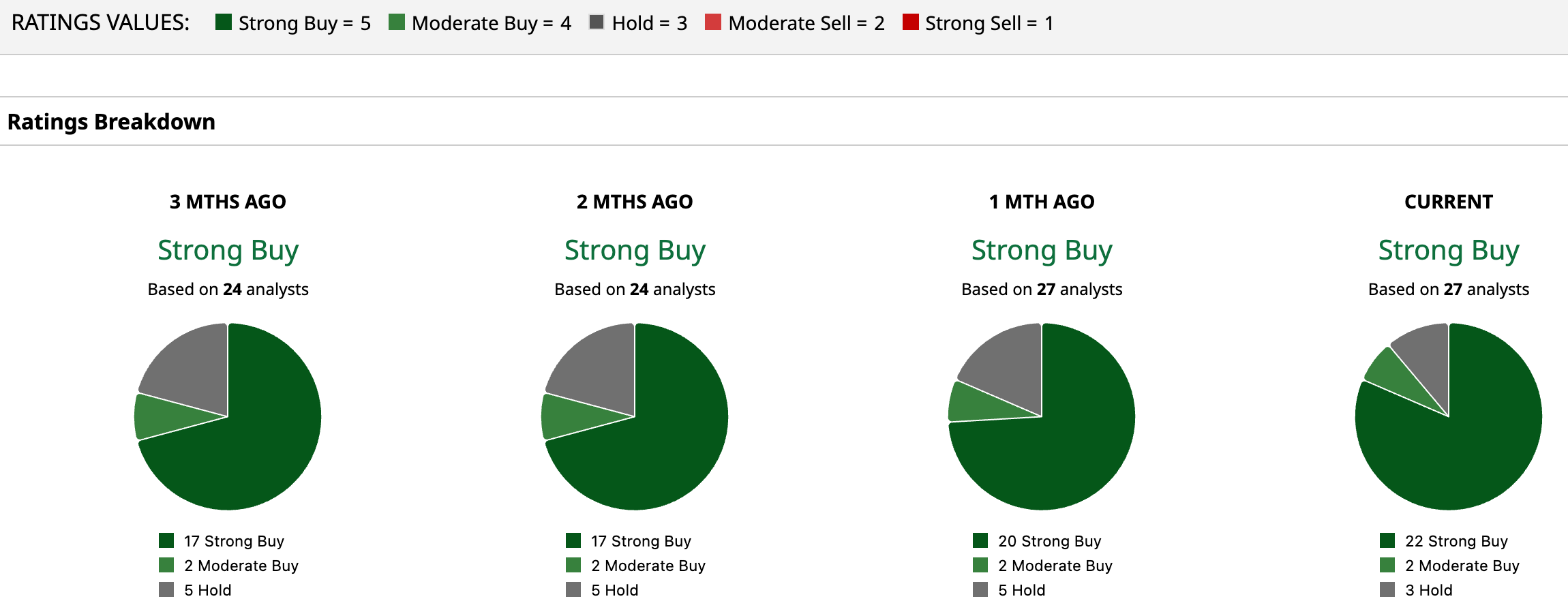

Overall, Wall Street remains overwhelmingly bullish on Arista Networks, with the stock carrying a consensus “Strong Buy” rating. Among the 27 analysts covering the company, 22 recommend “Strong Buy,” two rate it “Moderate Buy,” and only three remain on the sidelines with “Hold” ratings, highlighting continued confidence in Arista’s position at the center of the AI networking boom.

The bullish outlook also leaves room for meaningful upside ahead. The average analyst price target of $180.46 implies potential gains of 27.72% from current levels, while the Street-high target of $200 suggests the stock could rally as much as 41.55% despite the recent post-earnings volatility.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Ignore the Sell-Off in Arista Networks Stock. Analysts Still Think ANET Can Gain 36% from Here. Apple Stock Just Broke to New Record Highs with $300 Just Around the Corner 5 Stocks Our Top Technical Strategist is Tracking Now MSFT Stock Alert: Microsoft Weighs Abandoning Renewable Energy Target as AI Boom Continues