Intuit Inc. INTU, the software leader behind TurboTax, QuickBooks, Credit Karma and Mailchimp, has been a long-term winner in financial technology. Yet, despite reporting strong second-quarter fiscal 2026 results in February 2026, shares of Intuit have declined 41.4% over the past six months.

INTU shares have underperformed the Zacks Computer – Software industry, the S&P 500 composite, as well as peers such as Autodesk, Inc. ADSK and Commvault Systems, Inc. CVLT.

The decline reflects broader market pressures. In this environment, investors are likely to have reacted cautiously, with concerns that execution risks in certain segments could weigh on results.

However, the question now is whether this pullback creates a buying opportunity, signals further downside or suggests a period of holding steady.

Image Source: Zacks Investment Research

What’s in Favor of INTU Stock?

Intuit's growth thrives on blending AI with human intelligence (HI). This combo delivers "done-for-you" experiences that prioritize accuracy, compliance, security, reliability and data privacy, giving it a big edge over rivals. AI and HI automate tasks, boost payroll usage, and grow QuickBooks Live. Real-world testing over the past year proved that integrated AI-HI experiences yield better results for customers. This sets Intuit up for ongoing double-digit revenue growth as it taps into the total addressable market.

This month, Intuit announced QuickBooks Workforce in the United States, a new, end-to-end solution powered by agentic AI and human expertise that radically transforms how small and mid-market businesses run their human capital management.

Intuit is aggressively expanding into the mid-market through its AI-native Intuit Enterprise Suite, an all-in-one ERP platform that integrates financial management, payroll, HR, payments, and analytics. This addresses fragmented tech stacks and high costs for complex mid-market businesses. This platform is fueling the success of growing businesses, and the company is further scaling its investment in product innovation and go-to-market strategies to accelerate customer adoption.

Intuit delivered a strong second-quarter fiscal 2026, with revenues rising 17% year over year to $4.65 billion. Profitability also strengthened as non-GAAP operating income grew 23% to $1.55 billion. The company reiterated its fiscal 2026 guidance, projecting revenues between $20.997 billion and $21.186 billion, indicating 12-13% growth.

In the quarter, Global Business Solutions generated $3.2 billion in revenues, up 18% year over year, or 21% excluding Mailchimp. Intuit expects Global Business Solutions revenues to grow 14-15% for fiscal 2026. The Consumer Group delivered a solid performance in second-quarter fiscal 2026, with $1.5 billion in revenues, up 15% year over year. The company forecasts 8-9% revenue growth in 2026.

What Concerns Us About INTU?

Intuit has its share of challenges. Mailchimp remains a drag, with management expecting it to return to double-digit growth sometime beyond fiscal 2026. Moreover, Intuit’s performance is also partly tied to small-business health, lending conditions (Credit Karma) and consumer tax dynamics. A slowdown in consumer spending or credit demand could pressure growth.

Intuit’s high costs and expenses remain a major concern. The company has increased investments in engineering and marketing teams to grab the growing opportunity globally, making us cautious about the company’s bottom-line results. In the second quarter of fiscal 2026, the company’s total costs and expenses increased by 12.6% to $3.796 billion.

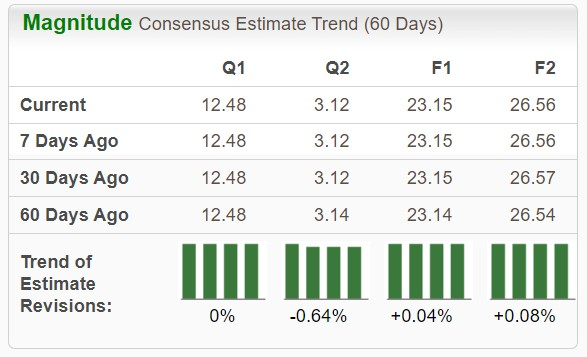

INTU’s Earnings Estimate Revision Trends Upward

The consensus estimate for Intuit’s fiscal 2026 earnings per share (EPS) has been revised upward by a cent to $23.15 over the past two months. 2026 EPS suggests 14.9% growth from the prior-year quarter.

Image Source: Zacks Investment Research

INTU Shares Trade at a Discount

In terms of forward 12-month price/sales (P/S), Intuit is trading at 4.62X, which is at a discount to the industry average of 6.91X.

Image Source: Zacks Investment Research

Final Take on INTU

Intuit remains one of the most compelling fintech platforms, with durable moats in tax, accounting and consumer finance. Its AI and HI integration, expanding mid-market presence and promising global business solutions and consumer segment results, positive earnings estimate and discounted valuation, position it well for sustained growth.

However, the Mailchimp drag and macro risks temper the near-term upside. While the 41.4% pullback improves entry points, it does not yet create a clear buying opportunity. Therefore, it seems prudent to hold the stock and wait for either signs of acceleration in Mailchimp or international growth before adding exposure.

Currently, Intuit carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Autodesk, Inc. (ADSK): Free Stock Analysis Report

Intuit Inc. (INTU): Free Stock Analysis Report

CommVault Systems, Inc. (CVLT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).