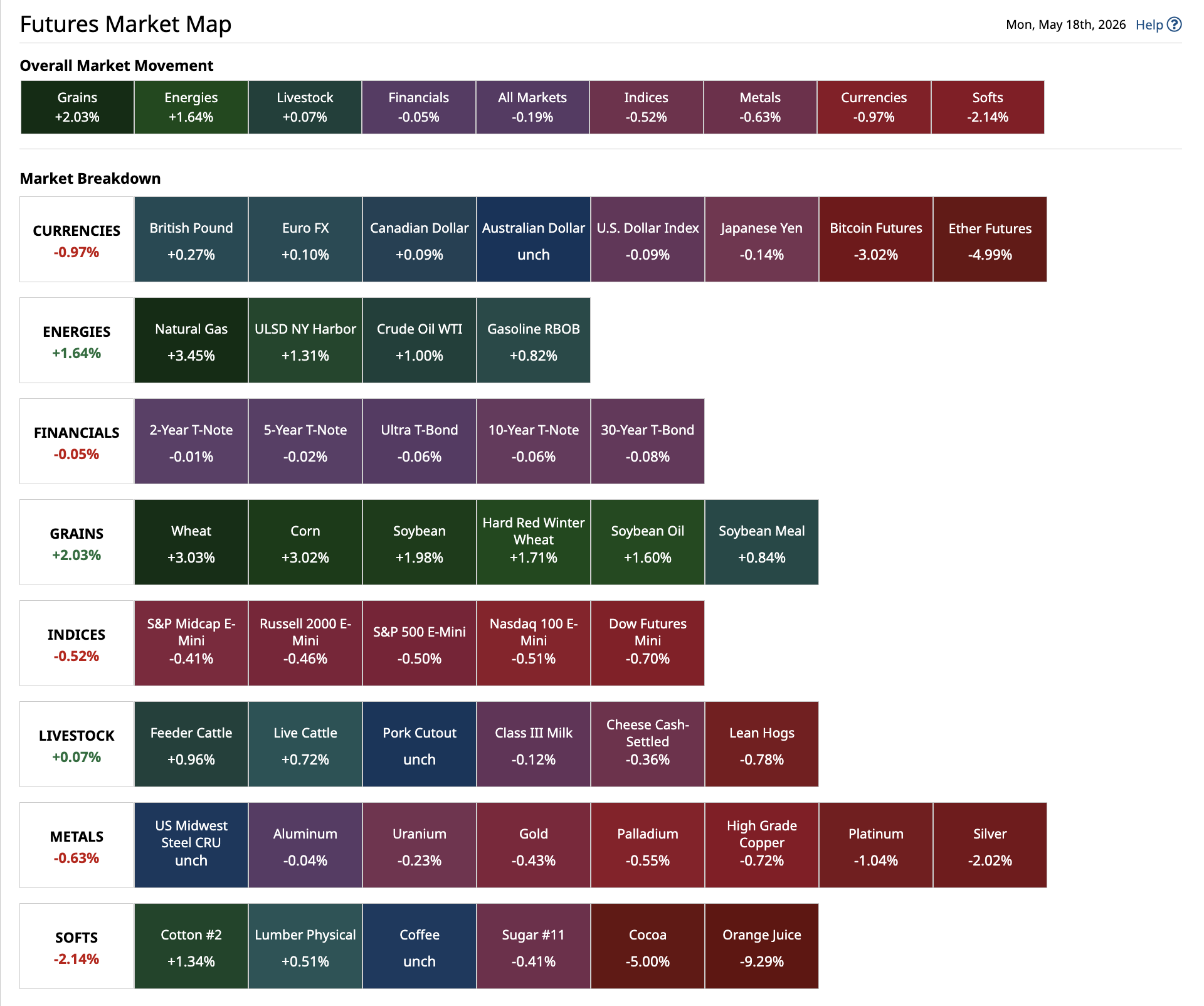

As markets across the commodity complex opened Sunday evening, we saw algorithms buy markets in both the Energies and Grains sectors to start the week.

Fundamentally, Energies remain bullish given nothing has really changed in the US president's War on Iran.

Don’t Miss a Day: From crude oil to coffee, sign up free for Barchart’s best-in-class commodity analysis.

As for the Grains sector, Watson wasn't watching weather with weekend rains stretching across the US Plains and Midwest.

Morning Summary: As I mentioned in the Sunday Night Markets Quick Take, Watson was once again driven to start the week by Sunday headlines. The two that stood out to me, ones we’ve heard countless times before, were the US president threatening destruction of Iran if the latter didn’t give in to his demands and the US administration saying China was going to be buying agricultural products from the US. You and I, along with anyone else who has more than one brain cell, know none of this is true, but Watson isn’t wired that way. Algorithms aren’t based on logic, oddly enough, but rather key words in a headline. Is it a crazy system? Absolutely, but it is the one we must deal with these days. To no surprise we wake to find both the Grains and Energies sectors higher to start the week. WTI crude oil (CLM26) rallied as much as $3.28 overnight but had given most of the gain back through Monday’s early morning hours. Diesel fuel (HOM26) added as much as 7.25 cents and was sitting 2.8 cents higher at this writing. Meanwhile, gold is down about $15 to start the day with silver off $2.15. Indices (US stock index futures) (ESM26) (YMM26) (NQM26) were lower to start the day, as would be expected for a Monday.

Corn: The corn market was sharply higher early Monday morning on big trade volume. After all, the world’s largest buyer of agricultural products is going to be back in the US market in a bigly way. How do we know? The US president told us so. Right. July (ZCN26) rallied as much as 17.5 cents on trade volume of 82,000 contracts and was sitting 14.25 cents higher at this writing. Recall July closed last Friday (it seems like an eternity ago, doesn’t it?) 11.75 cents lower for the day and 15.5 cents in the red for the week. The National Corn Index came in at $4.1575, also down about 11.75 cents for the day leaving national average basis at 40.0 cents under July futures as compared to the previous 10-year low weekly close for last week of 37.25 cents under July. Yes, the basis market remains weak. As for new-crop, September (ZCU26) was up 13.75 cents to start the day while December (ZCZ26) was up 12.75 cents, both on solid trade volume of 36,000 contracts and 46,000 contracts. Did it rain across the US Plains and Midwest this past week? Yes, it did. Are forecasts calling for more of the same this week? Also yes, but keep in mind weather doesn’t seem to matter to Watson these days.

Soybeans: The oilseed sub-sector was also solidly higher pre-dawn Monday. Here we see soybeans led the way, naturally, given the US will be delivering all it can produce to China by way of boat, plane, rocket ship, donkey, and even teleportation. Or so we’ve been told. And we’ve never been told this before, right? It was never previously suggested US producers should “work overtime” to produce more soybeans to meet China’s promised demand via Phase 1, Phase 2, Phase 10, Phase 46, or whatever “deal” phase we are up to now, right? None of those matters, though, for soybean contracts are higher today so all is fine with the world. July (ZSN26) added as much as 32.5 cents overnight on trade volume of 37,000 contracts and was sitting 24.75 cents in the green at this writing. A look back at last Friday and we see July closed 15.5 cents lower for the day and 31.0 cents lower for the week. National average basis came in Friday night at 65.0 cents under July futures, as compared to the previous 5-year low weekly close for last week of 63.0 cents under July. New-crop November (ZSX26) was up 24.0 cents after settling last Friday 12.75 cents in the red for the day and 18.75 cents lower for the week.

Wheat: The wheat sub-sector was glowing green across the board as well with all three markets posting double-digit gains. July SRW (ZWN26) added as much as 21.5 cents on trade volume of 23,000 contracts and was up 19.25 cents to start the day. Did it rain across much of the Midwest growing region this past weekend? Yes, it did. Is the SRW market fundamentally bearish? Well, national average basis came in last Friday at 55.5 cents under July futures as compared to the previous 5-year low for last week of 59.75 cents under. Also at last week’s close, the July-September futures spread covered 84% calculated full commercial carry while the September-December covered 82%. So, yes, the SRW market remains fundamentally bearish, but Watson said “Covfefe to our reads on real supply and demand because headlines told it to buy anyway. It’s also worth noting the latest Commitments of Traders report showed Watson still held a net-short futures position of 14,420 contracts as of Tuesday, May 12, though this was a decrease of 2,250 contracts from the previous week. July HRW (KEN26) was up 11.5 cents at this writing after adding as much as 17.5 cents overnight.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Was the Rally in Energies and Grains to Start the Week a Surprise? What Made Friday's Headlines Expected? Buy Corn Here If You Agree That Grains Will Be the Next Commodities to Rocket Higher Like Silver Why Was Tuesday Wheat's Time to Shine?