Warning: A key part of the options market you may be relying on is no longer working.

I’m talking about the fact that implied volatility is spiking selectively, sending call option premiums into the stratosphere. Everyone is scrambling to buy short-dated upside exposure, paying massive premiums for the privilege.

Can’t Get Enough Options?: Join the list for Barchart’s daily unusual options report, delivered free.

There are plenty of cases, but I’ll use perhaps the most timely example. That’s Micron (MU).

www.barchart.com

www.barchart.com That price chart is the thing traders dream about. But when a stock vaults like that, if you own it, you want to hedge it. And if you don’t own it, you want to. But you don’t want to be the “greatest fool” buying in at the potential peak.

The knee-jerk response has always been to pass on the stock we “missed” and instead buy out-of-the-money call options on it. After all, when controlling 100 shares of MU now requires more than $90,000 invested and thus at risk, why not buy an out-of-the-money call option for a fraction of that price?

For perhaps a capital commitment and maximum loss of $5,000 or less, you might end up making more in dollars using call options. That’s what I call “good leverage.”

READ MORE: I found a new article from my colleague Rick Orford in Barchart’s great library. It explains the basics of this approach.

MU’s rapid rise in price would typically cause call option prices to stay fairly low. That’s because when a stock goes up, options math relates that to lower risk. The opposite case is in force too. This is why ETFs like the ProShares VIX Short-Term Futures ETF (VIXY) and the ProShares VIX Mid-Term Futures ETF (VIXM), which I’ve covered here, are valuable hedges against down markets. Higher volatility is not normally associated with higher prices.

www.barchart.com

www.barchart.com That’s changing.

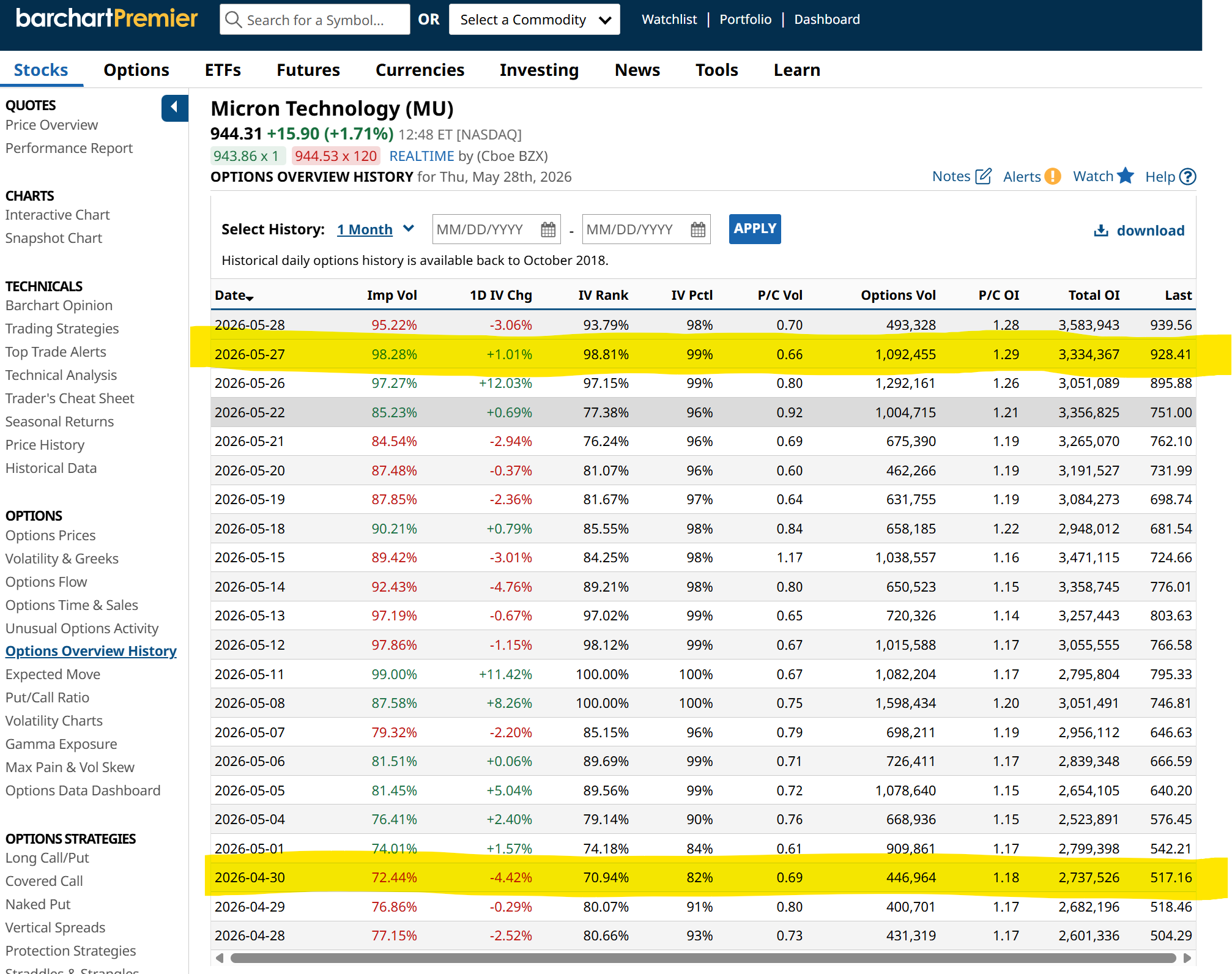

In the table above, I’ve highlighted where MU call options were in the aggregate about a month ago. And where they are now. Their implied volatility has gone UP not down. That means call options are much more expensive than usual. Which in turn means trying to “get away” with the old trader’s trick of using call options as a surrogate to get our “fair share” of extended moves in hot stocks has been blunted. This is because many investors have caught on to this approach, and the surge in demand has popped the lid off call option valuations.

I say this from personal experience. I recently wanted to buy calls on MU. When I saw this happening, sitting at my trading desk, I said out loud “oh no!”

Chasing expensive calls is a sucker’s game when premiums are this heavily inflated. Instead, there is a far smarter, high-conviction structural strategy staring us right in the face: utilizing 3X single-stock leveraged ETFs — the “celebrity” vehicles of the trading world.

Why 3X Leveraged ETFs Beat Buying Expensive Calls

When call options are wildly overpriced, buying them means you are fighting severe structural drag. The stock has to make an immediate, massive vertical move just for your option to break even before time decay eats your capital.

3X single-stock leveraged ETFs completely sidestep this problem while keeping the explosive upside alive. These high-octane vehicles are engineered to deliver 300% of the daily performance of single mega-cap leaders — the “celebrities” of our current momentum market like Nvidia (NVDA), Apple (AAPL), or Tesla (TSLA).

When you buy a 3X leveraged ETF instead of an option, you get the dramatic asset acceleration you want without a ticking clock. There is no expiration date, and you aren’t paying a massive volatility premium to an options seller. You are effectively capturing structural, amplified momentum through a liquid equity instrument.

The key, as always, is to not be a pig. Keep your position size VERY light. My rule of thumb with 3x long ETFs is to buy one-third as much of what I would have bought, so my “exposure” is the same as if I bought the stock.

But if it is an inverse ETF I’m buying to effect a bearish position or hedge on a stock or market segment, I will also do what smart hedge fund managers do: my short position is on average going to be smaller than my average long position. Bearish trades are great when they work, but the math of investing loss can get you quickly if the first move in the stock is a strong up move. Remember, you lose 20% and it takes a 25% gain just to get back to even.

You can be a bull or a bear with this strategy since many popular stocks are now available to trade via leveraged long and inverse ETFs. That means you can literally build your own long-short hedge fund, without the risks of shorting. And without having to consider overpriced options. .

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob’s written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

How Overzealous Option Traders Are Making 3X Leveraged ETFs Look Like Saviors Northrop Grumman Just Hiked Its Dividend, But Its Stock Has Tanked - Time to Buy NOC? Unusual Options Activity Points to Boston Scientific Stock as a Hot M&A Target Marvell Technology Reports Strong FCF and Outlook - Could MRVL Move Higher?