Just as inference and agentic AI are rapidly becoming the next steps of the AI revolution, physical AI's day in the spotlight is also edging closer. In fact, one study by consulting firm PwC predicts that the physical AI market will grow to about $500 billion by 2030, with applications in healthcare, defense, mobility, and logistics, among others.

Amid its own newfound confidence, Intel (INTC) is looking to make a splash in this lucrative and rapidly growing market by partnering with a Japanese manufacturing legend in Hitachi (HTHIY). The duo has identified five strategic areas to focus on: foundry tools, quantum computing, energy optimization, custom silicon and edge-AI applications, and factory automation.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

"The coming wave of physical AI will transform the industrial edge of our economy through new advances in robotics, autonomous machines, and other AI edge devices," said Intel CEO Lip Bu-Tan.

Despite recent weakness, INTC stock has been on a roll this year, rising by a sharp 192% year-to-date (YTD). Can this latest development halt its share price decline and redirect shares upward again? Let's analyze by keeping the company's physical AI initiatives in focus.

www.barchart.com

www.barchart.com Intel and Physical AI

While the current bullish thesis around Intel revolves around its CPUs, the optimism flows down to physical AI as well.

The physical AI angle specifically runs through Intel's Core Ultra Series 3 processors, which launched at CES 2026 and began reaching enterprise robotics developers in earnest by COMPUTEX 2026. Intel's position here is that pairing Core Ultra Series 3 with its new OpenVINO Physical AI framework provides a unified hardware and software stack that lowers total cost of ownership and improves code efficiency compared to the dual-compute setups that have historically burdened robotics deployments. The company has also put benchmarks on the table. Intel claims cost, performance, and value advantages against Nvidia's (NVDA) Jetson AGX Orin and Jetson Thor T5000 on medium-sized vision-language-action workloads, though those comparisons come from Intel's own testing and should be read accordingly.

Notably, 130 companies are now testing or deploying applications on Intel's Series 3 processor family, which is a concrete early signal.

Overall, compared to Nvidia (NVDA) — which owns the physical AI narrative through its GR00T robot foundation models and the Jetson platform — Intel is a credible challenger, but still a challenger.

Intel has also introduced Physical AI Studio alongside OpenVINO Physical AI as part of its Robotics AI Suite, giving developers tools for data collection, model fine-tuning, optimization, quantization, and export of pre-validated models ready for deployment.

However, all of these developments are at the rudimentary stages, and whether Intel can generate material revenues with sustainable margins will be intriguing.

Intel's Improving Financials

Intel kicked off 2026 on a positive note, achieving a solid double beat on both top-line and bottom-line results in the first quarter of 2026.

Total revenue advanced 7% year-over-year (YOY) to $13.6 billion in Q1. Growth was primarily driven by the Data Center and Artificial Intelligence (DCAI) segment, along with the Foundry business. The DCAI unit expanded 22% YOY to $5.1 billion, while the Foundry segment posted a healthy 16% YOY increase to $5.4 billion. In contrast, the Client Computing Group — Intel’s largest revenue source — showed more modest progress with a 1% gain to $7.7 billion, constrained by supply limitations and a mature personal computer market.

On the profitability side, EPS more than doubled to $0.29, comfortably surpassing consensus estimates by a wide margin. This performance extended Intel’s streak of consecutive earnings beats to three quarters.

For Q2 2026, management projected revenue between $13.8 billion and $14.8 billion along with non-GAAP EPS of $0.20. Current Wall Street forecasts for Q2 stand at $14.4 billion in revenue and EPS of $0.21 per share.

Cash generation saw improvement as well in Q3, with net cash from operating activities rising to $1.1 billion from $813 million in the year-ago quarter. Intel ended the period with a strong cash position of $17.7 billion, well above its short-term debt levels of approximately $2 billion.

Valuation remains a key area of concern for the INTC stock investment thesis. The stock continues to trade at a premium compared with both sector peers and its own historical averages. The forward price-to-earnings (P/E) multiple of 156.6 times, forward price-to-sales (P/S) multiple of 9.4 times, and price-to-cash flow (P/CF) multiple of 44.2 times all sit significantly above relevant sector medians. This premium leaves the shares reliant on sustained strong execution to support the elevated market pricing.

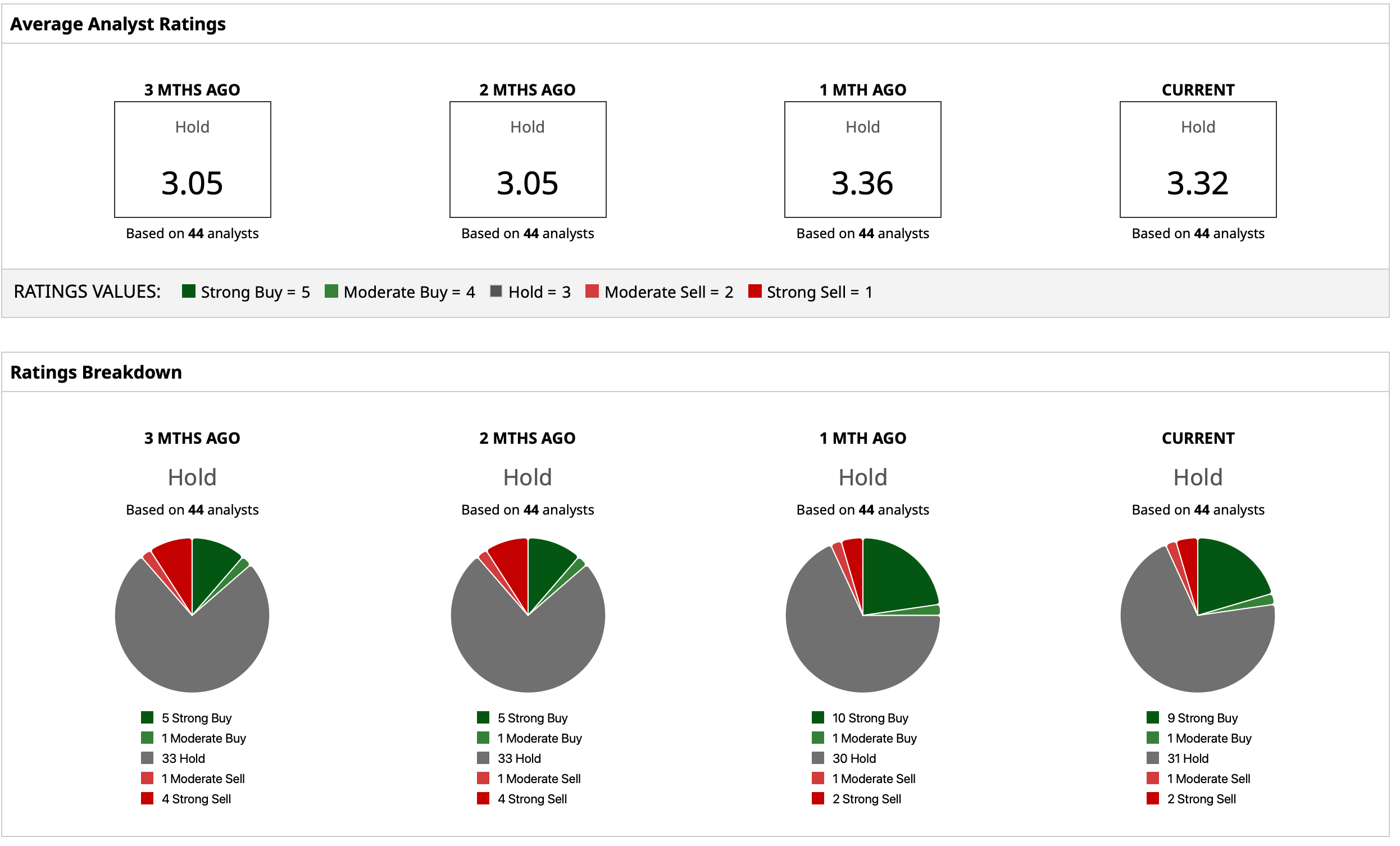

What Do Analysts Think of Intel Stock?

Considering all of this, analysts have an overall rating of “Hold” for INTC stock, with the mean target price of $90.58 already surpassed. The high target price of $150, however, indicates potential upside of about 39% from current levels. Out of 44 analysts covering INTC stock, nine have a “Strong Buy” rating, one has a “Moderate Buy” rating, 31 analysts have a “Hold” rating, one has a “Moderate Sell,” and two have a “Strong Sell” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Tapestry Stock Is Breaking Out: Why Shares Have at Least 10% More Upside Potential Wedbush Gives a Thumbs Up to Palantir’s AIPCon, But I Think AIPCon 2026 Was a Dud for PLTR Stock Intel Is Joining Hands With Hitachi to Bring Physical AI to Life. It Needs to Bring the INTC Stock Valuation Down, Too. Xpeng’s AI Progress Should Give XPEV Stock a Big Boost in the Long Term