Driven by solid U.S. GDP growth, which boosted confidence in economic resilience and future earnings, shares of Ally Financial Inc. ALLY have gained 13.7% in the past six months, outperforming the industry and the S&P 500 index’s growth of 7.4% and 11%, respectively.

If we compare ALLY’s price performance with its close peers, OneMain Holdings, Inc. OMF and Credit Acceptance Corporation CACC, it appears that ALLY has outperformed both CACC and OMF.

Over the past six months, shares of Credit Acceptance have gained 9.7%, while OneMain Holdings’ stock has rallied 10.8%.

6-Month Price Performance

Image Source: Zacks Investment Research

Does ALLY stock have more upside left despite recent strength in price? Let us find out.

Factors Aiding Ally Financial’s Growth

Revenue Strength: Growth in one of the key sources of revenues — net financing revenues — has been a major positive for Ally Financial. While the metric declined in 2024, it witnessed a compound annual growth rate (CAGR) of 4.9% over the six years ended 2025. The company’s net total finance receivables and loans recorded a CAGR of 3.1% in the five years ended 2025.

Supported by strong origination volumes, retail loan growth and ALLY’s balance sheet repositioning action (undertaken in March 2025), its net financing revenues are expected to continue improving in the quarters ahead.

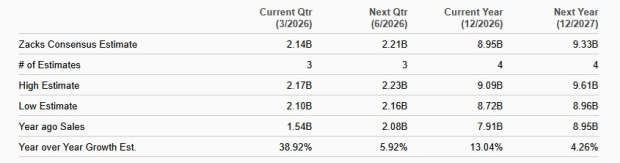

Per the Zacks Consensus Estimate, ALLY’s total revenues for 2026 are projected to grow 13% on a year-over-year basis.

Revenue Growth Estimate

Image Source: Zacks Investment Research

Restructuring Efforts: Ally Financial has been restructuring its operations to create a simplified and streamlined organizational structure. As such, the company announced some business actions in January 2025. These include the divestiture of its credit card business (Ally Credit Card), ceasing new mortgage loan originations and reducing workforce.

In 2024, the company divested its point-of-sale financing business, Ally Lending. Further, Ally Financial plans to invest resources in growing core businesses and strengthening relationships with dealer customers.

These efforts are expected to drive the company’s other revenues. While the metric declined in 2025, it saw a five-year (ended 2024) CAGR of 4.2%.

Robust Liquidity Position: As of Dec. 31, 2025, Ally Financial had total debt of $21.8 billion (the majority of this is long-term in nature) and total cash and cash equivalents of $10 billion. Nevertheless, the company maintains investment grade ratings of BBB- from both Standard & Poor’s and Fitch, and Baa3 from Moody’s on its long-term debt, which enables it to access the debt markets easily.

Moreover, ALLY has come a long way in improving its balance sheet and fundamentals. This has resulted in the company’s robust capital distribution actions. In January 2022, it announced a 20% dividend hike and has maintained it since then.

In December 2025, the company announced a multi-year share repurchase plan to repurchase shares worth up to $2 billion (without an expiration date). Ally Financial did not repurchase shares since 2023 but resumed buybacks in the fourth quarter of 2025. The company is expected to be able to sustain enhanced capital distributions, driven by its capital strength, earnings growth and favorable dividend payout ratio. Through this, ALLY will be able to keep enhancing shareholder value.

What’s Hurting Ally Financial?

Weak Asset Quality: Weakening asset quality is a major headwind for Ally Financial. Although the company’s net charge-offs (NCOs) and provision for loan losses declined in 2021, both increased in the years post that. While both metrics declined in 2025, relatively high interest rates, volatility and cumulative inflationary pressure are leading to the deteriorating credit profile of the company’s borrowers, which will likely result in a near-term rise in credit costs. Hence, NCOs and provisions are expected to remain elevated.

Elevated Expense Base: Ally Financial has been witnessing a persistent rise in expenses. Over the last six years (ended 2025), the company’s expenses saw a CAGR of 7.8%. The increase was mainly due to higher compensation and benefit costs.

With the company launching products and focusing on core operations, non-interest expenses are expected to remain elevated. Management expects adjusted non-interest expenses to increase 1% year over year in 2026.

Pressure on Net Interest Margin (NIM): While ALLY’s net yield on interest-earning assets expanded to 3.43% in 2025, the metric declined to 3.27% in 2024 from 3.32% in 2023, 3.85% in 2022 and 3.54% in 2021 because of a jump in deposit costs.

Although management expects the company’s balance sheet to turn liability-sensitive in the medium term, it will remain modestly asset-sensitive in the next few quarters.

Thus, despite the Federal Reserve cutting interest rates, the still relatively high interest-rate environment is expected to adversely impact Ally Financial’s NIM. The sale of the credit card business will further affect NIM expansion, while runoff in the mortgage loan portfolio is expected to offset this to some extent.

Analyzing ALLY’s Earnings Estimates & Valuation

Analysts do not seem optimistic regarding ALLY’s earnings growth potential. Over the past 30 days, the Zacks Consensus Estimate for its 2026 and 2027 earnings has moved lower.

Estimate Revision Trend

Image Source: Zacks Investment Research

The earnings estimate for 2026 of $5.09 per share suggests a year-over-year rise of 33.6%. The estimate for 2027 of $6.15 suggests growth of 20.7%.

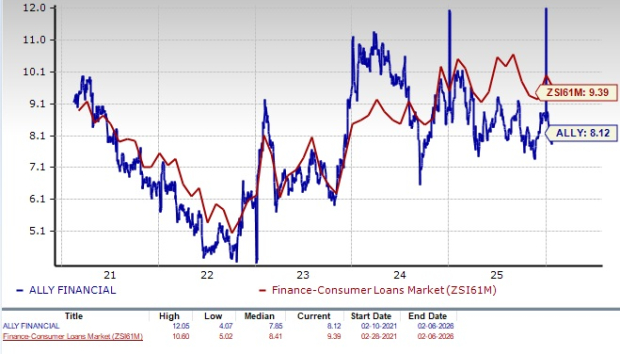

In terms of its valuation, ALLY’s forward 12-month price-to-earnings (P/E) ratio of 8.12X is currently below the industry average of 9.39X. This indicates that Ally Financial’s shares are trading at a discount in comparison to its peers.

P/E (F12M) Ratio

Image Source: Zacks Investment Research

How to Play ALLY Stock Now

Increasing net financing revenues and a solid liquidity position are expected to keep supporting ALLY’s financials. Moreover, the company’s business streamlining initiatives, focus on core businesses, solid origination volumes and balance sheet repositioning actions will likely drive revenue growth. An attractive valuation is another positive for the company.

However, weak asset quality, NIM pressure and elevated expenses remain major near-term headwinds for the company, which make us apprehensive about its growth prospects.

Thus, ALLY stock remains a cautious bet for investors at the moment. Those who already own the stock can hold on to it for now as it is less likely to disappoint in the long run.

Currently, Ally Financial carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Credit Acceptance Corporation (CACC): Free Stock Analysis Report

Ally Financial Inc. (ALLY): Free Stock Analysis Report

OneMain Holdings, Inc. (OMF): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).