Amkor Trades Near 52-Week High: Buy, Sell or Hold the Stock?

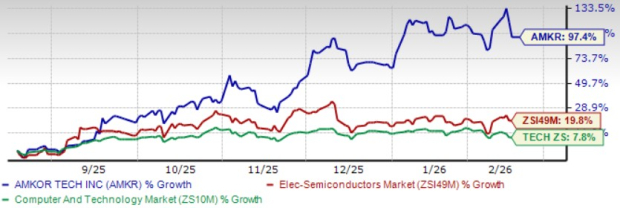

Amkor Technology AMKR shares closed at $47.48 on Friday, Feb. 13, down 16.8% from the 52-week high of $57.09 reached on Feb. 11, 2026. AMKR shares have jumped 97.4% in the past six months, outperforming the Zacks Computer & Technology sector’s return of 7.8% and the Zacks Electronics-Semiconductors industry's 19.8% growth.

The stock has underperformed its peer, ASE Technology ASX, whose shares have surged 131.7% over the same period, while tracking close to Intel INTC, up 97.8%, and outpacing Taiwan Semiconductor TSM, which has surged 51.8%.

The rally has been driven by accelerating demand for advanced packaging tied to AI and high-performance computing, particularly the ramp of AMKR’s High Density Fan Out (HDFO) platform for data center and CPU programs.

AMKR Stock’s Performance

Image Source: Zacks Investment Research

AMKR’s Q4 Strength and 2026 Investment Cycle

AMKR delivered a strong fourth quarter, with net sales of $1.89 billion rising 16% year over year and beating the Zacks Consensus Estimate by 3.35%. EPS of 69 cents surpassed the consensus mark by 60.5%. The upside reflects higher advanced packaging revenue, particularly in communications, where stronger iOS demand contributed meaningfully. The mix shift toward advanced products supported gross margin expansion to 16.7%, though approximately $30 million in one-time asset sale proceeds supported gross profit. For 2025, AMKR reported sales of $6.71 billion, up 6% year over year, reflecting steady progress in computing and automotive alongside stabilization in communications.

For the fiscal first-quarter, AMKR expects sales between $1.6 billion and $1.7 billion, implying 25% year-over-year growth at the midpoint. Gross margin is projected between 12.5% and 13.5%, reflecting normalization following the fourth-quarter asset sale benefit. Excluding that item, the underlying margin profile appears stable. AMKR anticipated capital expenditure of $2.5 billion to $3 billion in 2026 compared with $905 million in 2025. The increase is tied to Phase 1 construction of the Arizona facility and HDFO capacity expansion in Korea. While this elevated spending may increase execution risk, it is aimed at expanding advanced packaging capacity to support anticipated demand in AI and data center programs. Returns will depend on utilization levels and program ramp timing.

The Zacks Consensus Estimate for AMKOR’s first-quarter EPS is pegged at 23 cents, up by 21.1% over the past 30 days. The figure indicates a year-over-year improvement of 155.56%.

Amkor Technology, Inc. Price and Consensus

Amkor Technology, Inc. price-consensus-chart | Amkor Technology, Inc. Quote

AMKR Bets Big on AI Packaging

Amkor has positioned computing as its primary growth engine for 2026, targeting over 20% year-on-year expansion in that segment. Two new central processing unit programs supporting AI data centers are in final qualification, with combined 2.5D and HDFO capacity expected to nearly triple over the year. Korea serves as the primary production hub, with System-in-Package products migrating to Vietnam to free up floor space for the HDFO ramp. Government incentives under the CHIPS Act and a 25% investment tax credit are expected to contribute upward of $2.85 billion toward the Arizona project cost, though these inflows lag initial capital outflows.

Growth remains back-half loaded, with one program expected to ramp to high volume and the second still uncertain on full-volume timing. Delays in qualification, equipment delivery or space buildout could compress results, making execution across milestones critical.

AMKR Faces Stiff Competition

Amkor Technology competes directly with ASE Technology, which holds greater scale, a wider customer base and deeper capacity across advanced packaging platforms. Taiwan Semiconductor continues expanding its proprietary packaging platforms, compressing the addressable market for independent assemblers like AMKR. Intel, once a reliable source of overflow packaging volumes for Amkor, is prioritizing its own in-house packaging capabilities, which could erode a historically stable revenue stream. With ASE Technology pulling ahead on scale, Taiwan Semiconductor vertically integrating, and Intel reducing its external packaging dependency, AMKR faces the challenge of defending its positioning on multiple fronts simultaneously, even as it pursues an ambitious and expensive capacity expansion of its own.

AMKR Trades at a Stretched Valuation

AMKR trades at a forward price-to-earnings multiple of 28.15x, above the broader sector median of 25.17x, even as the company enters a capital-intensive phase. Capital expenditure is set to rise sharply in 2026, driven by the Arizona facility and HDFO capacity expansion. With margins normalizing from elevated fourth-quarter levels and earnings increasingly reliant on timely capacity buildouts and customer program ramps, the current valuation appears stretched relative to the execution risk embedded in the outlook.

AMKR’s P/E Valuation

Image Source: Zacks Investment Research

Conclusion

AMKR is seeing robust traction in advanced packaging, supported by strong fourth-quarter results and expanding exposure to AI-driven computing programs. The company is scaling capacity through the Arizona facility and HDFO investments, which could support long-term growth if executed efficiently. However, margins are normalizing, and capital expenditure is set to increase materially in 2026, raising the importance of disciplined execution across new program ramps and facility buildouts. Intensifying competition from larger outsourced assembly players and vertically integrated semiconductor manufacturers adds pressure.

With shares rising sharply over the past six months and valuations stretched, it may be prudent for existing investors to maintain their current positions while prospective investors wait for a more favorable entry point.

AMKR currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Intel Corporation (INTC): Free Stock Analysis Report

Taiwan Semiconductor Manufacturing Company Ltd. (TSM): Free Stock Analysis Report

Amkor Technology, Inc. (AMKR): Free Stock Analysis Report

ASE Technology Holding Co., Ltd. (ASX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).