ADI Climbs 13% in a Month: Time to Buy, Sell or Hold the Stock?

Analog Devices ADI shares have jumped 13.2% in the past month, driven by positive investors’ sentiments based on ADI’s strong double-digit performance across industrial, communications and consumer segments and recovery in the automotive segment. ADI stock has outperformed the Zacks Semiconductor - Analog and Mixed industry’s appreciation of 9.8% and the Zacks Computer and Technology sector’s decline of 1.7%.

ADI One-Month Performance Chart

Image Source: Zacks Investment Research

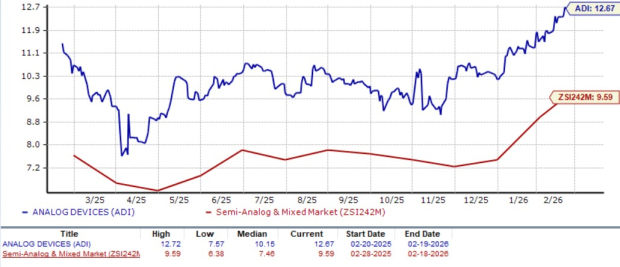

The rise in stock price has resulted in ADI trading at a premium with a forward (P/S) valuation of 12.67X, which is much above the industry’s valuation of 9.59X.

ADI Forward 12-Month Valuation Chart

Image Source: Zacks Investment Research

Given this strong outperformance and solid segmental growth, investors are left wondering if it is the right time to buy ADI stock when it’s trading at a premium. Let’s discuss the fundamentals in detail and uncover the investment opportunity in Analog Devices.

ADI Experiences Growth Across All Segments

ADI’s industrial and communication segments have been growing on the back of AI-driven infrastructure demand for the past four quarters. ADI’s industrial segment was driven by traction in automatic test equipment systems, which benefited from the demand for AI chips, broadening ADI’s strong position in the System on Chips and memory test markets.

In the first quarter of fiscal 2026, ADI’s industrial, communications, consumer and automotive showed year-over-year growth of 38%, 63%, 27% and 8%, respectively. In the communications segment, Analog Devices is experiencing strong demand for electro-optical interfaces with 800G moving toward 1.6T, precision power management, protection and monitoring.

ADI’s data center business has been growing in double digits year over year for the past four quarters. The company expects AI-driven advancements, including the development of more capable and content-rich humanoid robots, to create significant long-term growth opportunities and further strengthen ADI’s position in the robotics market.

Given these tailwinds, Analog Devices expects revenues of $3.5 billion (+/- $100 million) for the second quarter of fiscal 2026. The Zacks Consensus Estimate for second-quarter fiscal 2026 revenues is pegged at $3.21 billion, indicating year-over-year growth of 21.4%.

ADI Protects Its Margins Amid Rising Competition

Analog Devices' margins are expanding despite the rise in operating expenditure, capital expenditure and strong competitive pressure from companies. ADI’s first-quarter 2026 gross margin was 71.2%, up 140 basis points sequentially and 240 basis points year over year. The company’s operating margin was 45.5%, up 200 basis points sequentially and 500 basis points year over year.

ADI’s competitors include Texas Instruments TXN, STMicroelectronics STM and NXP Semiconductors NXPI. Texas Instruments competes with ADI in analog, digital and mixed signal chains, precision sensing, and power management for consumer electronics products. NXP Semiconductor is one of the leading solution providers of analog and mixed-signal chips serving mobile, connectivity, and consumer applications, serving front-end, power management, and mixed signal for consumer devices, especially in mobile and IOT markets.

Texas Instruments serves the auto market with its analog sensors, power ICs, in-vehicle networking/signal chain, and driver assistance electronics. STMicroelectronics competes with ADI with its sensors, such as MEMS and inertial, analog front ends, interface ICs, and microcontrollers. Although intense competition from major players pushed ADI to increase its research & development and sales & marketing spending at double-digit rates, the company’s strong revenue growth has helped protect its margins.

The Zacks Consensus Estimate for second-quarter fiscal 2026 earnings is pegged at $2.48, indicating year-over year growth of 34%. The Zacks Consensus Estimate for second-quarter fiscal 2026 earnings has been revised upward in the past seven days.

Image Source: Zacks Investment Research

Conclusion: Buy ADI Stock Now

Analog Devices’ strong stock performance reflects accelerating AI-driven growth, broad-based segment strength and resilient margins despite rising competition. With robust revenue momentum, expanding data center exposure, upward earnings revisions, and a bullish technical setup, ADI remains well-positioned, making this Zacks Rank #1 (Strong Buy) stock an attractive choice for long-term investors. You can see the complete list of today’s Zacks #1 Rank stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Analog Devices, Inc. (ADI): Free Stock Analysis Report

Texas Instruments Incorporated (TXN): Free Stock Analysis Report

STMicroelectronics N.V. (STM): Free Stock Analysis Report

NXP Semiconductors N.V. (NXPI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).