CRWD to Report Q4 Earnings: Should You Buy, Sell or Hold the Stock?

CrowdStrike Holdings CRWD is scheduled to report its fourth-quarter fiscal 2026 results on March 3, 2025.

CrowdStrike anticipates revenues between $1.29 billion and $1.30 billion for the fourth quarter of fiscal 2026. The Zacks Consensus Estimate for CrowdStrike’s fiscal fourth-quarter revenues is pegged at $1.30 billion, indicating year-over-year growth of 22.5%.

For the fiscal fourth quarter, the company expects non-GAAP earnings per share between $1.09 and $1.11. The Zacks Consensus Estimate for CrowdStrike’s fiscal fourth-quarter earnings is pegged at $1.10 per share, implying a year-over-year increase of 6.8%. The consensus mark for earnings has remained unchanged over the past 60 days.

Image Source: Zacks Investment Research

CrowdStrike’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 11.5%.

CrowdStrike Price and EPS Surprise

CrowdStrike price-eps-surprise | CrowdStrike Quote

Earnings Whispers for CRWD

Our proven model does not conclusively predict an earnings beat for CrowdStrike this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is not the case here.

CrowdStrike has an Earnings ESP of 0.00% and carries a Zacks Rank #3 at present. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter. You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Likely to Influence CRWD’s Q4 Results

CrowdStrike’s fourth-quarter fiscal 2026 results are likely to benefit from the robust demand for its cybersecurity products, given the increasing number of threat incidents across the globe. As a rising number of employees log into the enterprise's network, the vulnerabilities of cyber breaches lead to a greater need for security. These factors are likely to have spurred the demand for CrowdStrike’s products in the fiscal fourth quarter.

CrowdStrike’s Falcon Flex subscription model is expected to have remained a major growth driver. Annual recurring revenue (ARR) from Flex accounts crossed $1.35 billion, growing more than 200% year over year during the third quarter, showing strong adoption across enterprise customers. Falcon Flex helps customers adopt new modules without long contract steps, which leads to faster platform usage. This structure is leading to larger deals.

During the third quarter, CrowdStrike highlighted several Falcon Flex expansion deals. One example was a large European bank that renewed more than 500,000 workload endpoint deployments and added Next Generation (Next-Gen) Security Information and Event Management (SIEM), Onum, and Charlotte AI in a large eight-figure deal. Another example was a global healthcare customer that signed an eight-figure Falcon Flex contract, with Charlotte AI playing a central role in its security operations transformation.

CrowdStrike is seeing strong momentum in its Next-Gen SIEM as part of its mission to protect enterprises against evolving cyber threats. In the third quarter of fiscal 2026, Next-Gen SIEM posted record net new ARR, showing that more customers are choosing it over older SIEM tools that are costly and slow. A key boost came from CrowdStrike’s expanded partnership with Amazon Web Services (“AWS”). Millions of AWS users can now access Falcon Next-Gen SIEM directly inside AWS Security Hub. This gives CrowdStrike a much wider pool of potential customers and may help convert free usage into Flex subscriptions over time. The momentum is likely to have continued in the to-be-reported quarter.

CrowdStrike has enhanced AI-based capabilities like AI Model Scanning, Shadow AI detection and Charlotte AI Agentic Detection Triage. In the third quarter, CrowdStrike described Charlotte AI as an agentic security analyst that can help automate tasks like triage, investigation and response. Management said work that would take four days to complete can now be done in minutes using Charlotte AI. Charlotte AI achieved FedRAMP high authorization during the third quarter, as well. This means U.S. government agencies can use Charlotte AI through the Falcon platform in GovCloud. Since government and regulated customers are large security buyers, so this can support SIEM and SOC deals, which is expected to have boded well for CrowdStrike’s prospects in the to-be-reported quarter.

CRWD Price Performance & Stock Valuation

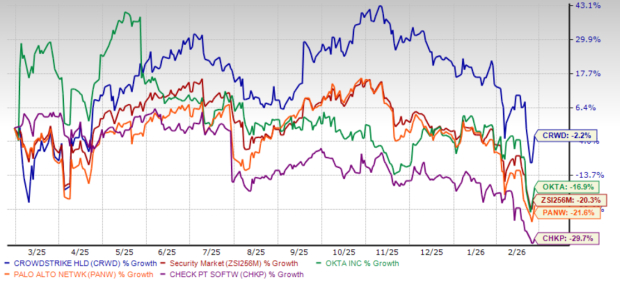

Over the past year, shares of CrowdStrike have lost 2.2%, outperforming the Zacks Security industry and its peers, including Check Point Software CHKP, Palo Alto Networks PANW and Okta Inc. OKTA.

The Zacks Security industry has declined 20.3% over the past year. Shares of Palo Alto Networks, Check Point Software and Okta have plunged 21.6%, 29.7% and 16.9%, respectively.

One-Year Price Return Performance

Image Source: Zacks Investment Research

Now, let’s look at the value CrowdStrike offers investors at the current levels. CrowdStrike is trading at a premium with a forward 12-month P/S of 16.19X compared with the industry’s 9.61X, reflecting a stretched valuation.

Forward 12-Month P/S Ratio

Image Source: Zacks Investment Research

CrowdStrike stock also trades at a higher P/S multiple compared with other industry peers, including Checkpoint Software, Palo Alto Networks and Okta. At present, Checkpoint Software, Palo Alto Networks and Okta have P/S multiples of 5.83X, 9.92X and 4.18X, respectively.

Investment Consideration for CrowdStrike

A significant driver of new customer addition is the Falcon Flex subscription model, which simplifies security adoption by offering modular, scalable cybersecurity solutions. CrowdStrike secured major deals in the last reported quarter, including eight-figure Falcon Flex agreements with a global healthcare customer company and a large European bank, showing strong enterprise demand. This shows CrowdStrike’s ability to attract high-value customers, encourages long-term commitments, steady revenue growth and deep customer integration.

However, CrowdStrike’s rising costs are a cause of concern. Over the last six fiscals, CrowdStrike’s Research & Development expenses increased 12-fold, while Sales & Marketing expenses rose nearly ninefold to $1.52 billion in fiscal 2025 from $173 million in fiscal 2019. Though the firm foresees these investments generating benefits over the long run, higher expenses are expected to weigh on the company’s bottom-line results.

Conclusion: Hold CrowdStrike Stock Right Now

As businesses continue prioritizing AI-driven cybersecurity solutions, CrowdStrike’s leadership in threat prevention, response and recovery will only strengthen. CrowdStrike’s subscription-based model and recurring revenue streams, along with its strong partner base, should provide stability and gradual growth, even amid ongoing macroeconomic challenges and geopolitical issues.

However, rising costs and premium valuation warrant a cautious approach to the stock.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Check Point Software Technologies Ltd. (CHKP): Free Stock Analysis Report

Palo Alto Networks, Inc. (PANW): Free Stock Analysis Report

Okta, Inc. (OKTA): Free Stock Analysis Report

CrowdStrike (CRWD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).