Astronics vs. TransDigm: Which Aerospace Stock Is a Better Buy?

Increasing aircraft deliveries worldwide, fleet expansion by airlines and rising demand for maintenance, repair and overhaul (MRO) services are fueling growth across the aviation services sector. Continued recovery in global air travel and sustained defense modernization efforts are enhancing investor confidence in aerospace service providers such as Astronics Corporation ATRO and TransDigm Group Incorporated TDG.

ATRO is a leading provider of advanced technologies to the global aerospace, defense and electronics industries. TransDigm is a leading global designer, producer and supplier of highly engineered aircraft components that are critical to the safe and effective operation of nearly all commercial and military aircraft worldwide.

Ongoing technological advancements, heightened emphasis on aircraft efficiency and the gradual easing of supply-chain constraints are drawing growing attention to aviation support companies.

As an investment option, which stock, ATRO or TDG, is more attractive for long-term investors? Let’s take a closer look.

The Case for Astronics

Astronics is a specialized provider of advanced electrical power, connectivity, lighting, and test systems serving the global aerospace and defense markets. With exposure to both commercial and military aviation, the company is well-positioned to benefit from multiple demand drivers across end markets.

Favorable conditions in defense and commercial aerospace are supporting growth. Rising global defense budgets are sustaining demand for military aircraft programs, while continued air travel expansion is encouraging airlines to invest in cabin upgrades such as in-seat power and in-flight connectivity—areas aligned with Astronics’ core capabilities. These trends offer a solid platform for continued expansion.

The company benefits from long product life cycles, high switching costs, and established customer relationships, creating durable competitive advantages and recurring revenue opportunities. As aerospace market conditions improve, these strengths support a multi-year growth outlook and margin recovery potential.

Management is focused on margin enhancement through cost discipline, supply-chain stabilization and prudent capital allocation. Increasing production volumes are expected to drive operating leverage, supporting margin expansion and stronger free cash flow. The aerospace segment, which generates most revenues, continues to grow steadily, and a solid backlog enhances revenue visibility. Astronics’ projected 2026 revenue range of $950–$990 million reflects sustained defense spending and ongoing airline upgrade activity.

However, supply-chain constraints—including raw material shortages, higher input costs, skilled labor limitations, and rising U.S. tariffs—may put pressure on production schedules and delay deliveries, potentially weighing on near-term performance.

Despite these risks, Astronics’ return on invested capital (ROIC) of 15.8% is significantly above the industry average of 3.3%. This highlights its strong capital efficiency and effective deployment of resources relative to peers.

The Case for TransDigm

TransDigm’s business model is built around proprietary, sole-source products and a strong presence in the aftermarket segment. The company often serves as the only approved supplier for many of its components, which gives it considerable pricing power and creates high switching costs for customers. This unique positioning enables TransDigm to maintain resilient margins and generate consistent cash flows.

The company also holds a meaningful position in the U.S. defense aerospace market. It stands to benefit from the U.S. government’s increased focus on strengthening national defense capabilities through higher spending. In January 2026, President Donald Trump proposed raising annual military expenditures to approximately $1.5 trillion by 2027, a substantial increase from the roughly $901 billion defense budget approved for fiscal 2026, pending congressional approval. If enacted, this significant funding boost could drive additional contract awards for major defense contractors such as Boeing and other military aircraft manufacturers. As a key supplier of critical components, TransDigm would likely benefit from higher production volumes and expanded defense programs.

At the same time, improving global air traffic trends have supported a rebound in the commercial aerospace market. Strong growth in both domestic and international revenue passenger kilometers (RPKs) has fueled demand for aircraft maintenance and replacement parts, further strengthening TransDigm’s high-margin aftermarket business. The company continues to pursue a disciplined acquisition strategy, targeting niche, proprietary businesses that expand its product portfolio and enhance aftermarket revenues.

However, TransDigm faces headwinds in its commercial original equipment segment, along with ongoing supply-chain disruptions, including shortages of electronic components, castings and skilled labor. Also, its ROIC is negative 5.9%.

Estimates for ATRO and TDG

The Zacks Consensus Estimate for ATRO’s 2026 and 2027 revenues implies a 11.9% and 5.8% respective year-over-year increase. EPS estimates for 2026 and 2027 imply 30.4% and 18.1% year-over-year increase, respectively. Earnings estimates for 2026 and 2027 have moved up 2.7% and 5.5%, respectively, in the past seven days.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for TDG’s 2026 and 2027 revenues implies a 13.6% and 8.8% year-over-year increase, respectively. EPS estimates for 2026 and 2027 imply 5.7% and 17.7% year-over-year increase, respectively. Earnings estimates for 2026 and 2027 have moved up a respective 3.7% and 8.9% in the past seven days.

Image Source: Zacks Investment Research

Price Performance of ATRO and TDG

ATRO shares have gained 4.8% in a month, while TDG shares have lost 6.9% in the same time.

Image Source: Zacks Investment Research

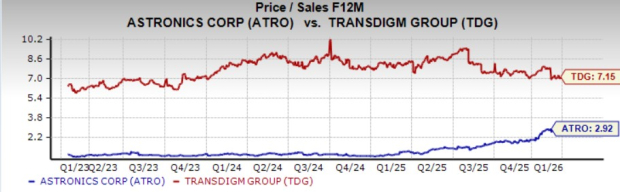

Are ATRO and TDG Shares Expensive?

ATRO is trading at a forward 12-month price-to-sales multiple of 2.92, higher than its median of 0.83X over the past three years. TDG’s forward 12-month price-to-sales multiple sits at 7.15, lower than its median of 7.89X over the past three years.

Image Source: Zacks Investment Research

Both ATRO and TDG are trading lower than the industry average of 12.7X.

Parting Thoughts

Astronics is poised to grow on its niche focus, proprietary technologies, and exposure to secular aerospace growth trends. Its solid growth prospects and its VGM Score of B instill confidence.

On the other hand, TransDigm, being an equipment supplier of renowned military jet makers, should benefit from solid funding provisions from the U.S. government.

Astronics sports a Zacks Rank #1 (Strong Buy) while TransDigm carries a Zacks Rank #2 (Buy). Price appreciation, valuation, VGM Score, growth estimates and analyst sentiments give ATRO an edge over TDG.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Transdigm Group Incorporated (TDG): Free Stock Analysis Report

Astronics Corporation (ATRO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).