Ondas, Inc. ONDS is trading at a forward 12-month price-to-sales ratio of 9.14X, a premium compared with the Zacks Wireless National industry’s 1.84X and the Zacks Computer and Technology sector’s 6.04X.

Image Source: Zacks Investment Research

The company’s lofty premium valuation raises an important question for investors. Does this accurately capture the company’s long-term opportunity, or is it running ahead of fundamentals?

Let’s break it down.

ONDS’ Explosive Growth Masks Several Challenges

At first glance, ONDS appears as a compelling story.

Ondas entered 2026 following a transformational year marked by a pivot to autonomous systems, aggressive portfolio expansion and platform scaling.

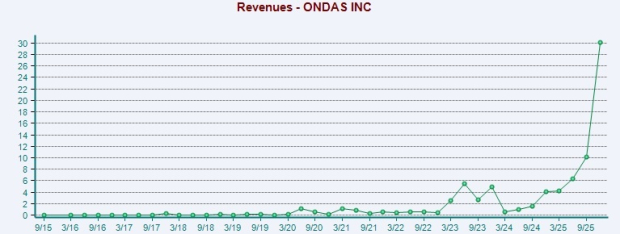

Revenues surged 629% for the fourth quarter of 2025, while full-year revenues were up 605% to $50.7 million. Building on this momentum, management raised its 2026 revenue outlook to at least $375 million, from an earlier target of $170-$180 million.

Image Source: Zacks Investment Research

At the heart of ONDS explosive growth is Ondas Autonomous Systems (“OAS”) division. OAS has quickly become a comprehensive “system-of-systems” platform. The division is now a multi-domain autonomy platform spanning Intelligence, Surveillance, Reconnaissance or ISR, Counter-UAS, loitering munitions/strike systems, unmanned ground vehicles and stratospheric sensing via World View acquisition.

An ambitious acquisition strategy is fueling Ondas’ expansion. In the first quarter of 2026, ONDS announced five acquisitions (World View, Mistral, Rotron, BIRD and INDO Earth). These acquisitions add strategic capabilities while expanding the addressable market for Ondas. Last year, the company acquired several companies, including Sentrycs, Apeiro Motion, Zickel and Roboteam.

However, Ondas’ acquisition spree raises an important concern. The company is not scaling a proven business model, but it is assembling one through aggressive deal-making.

ONDS’ bullish guidance for 2026 is anchored mostly by its inorganic efforts. The company expects the five acquisitions announced in the first quarter of 2026 to add $230 million to revenues. This is a little problematic as so many acquisitions in such a short period can create integration overload and execution risks, as achieving targets depends on timely integration and conversion of backlog into revenues.

Image Source: Zacks Investment Research

Further, profitability remains elusive. In the fourth quarter of 2025, operating expenses increased to $36.1 million, up from $9.4 million in the prior-year quarter, mainly driven by M&A activity, infrastructure investments and higher personnel costs. As a result, adjusted EBITDA loss widened to $9.9 million compared with a loss of $7 million in the year-ago quarter. Net loss was $101 million for the fourth quarter and $133.4 million for the full year.

Adjusted EBITDA losses are expected to widen in the first quarter due to higher operating expenses, including increased leadership hiring and marketing investments to support rapid growth. Ondas expects EBITDA margins to improve over the year and expects product-level profitability by the third quarter of 2026. However, OAS profitability is expected by the third quarter of 2027, and more importantly, company-wide profitability only by the first quarter of 2028.

While management characterizes these investments as necessary to support growth, this can pose a significant concern for investors.

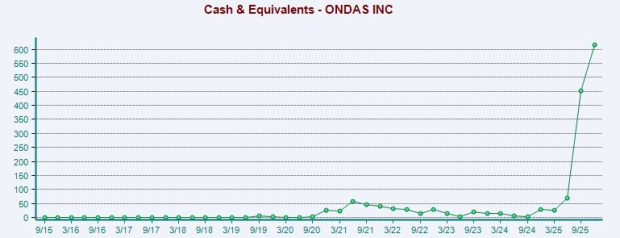

Another concern is the ballooning pro forma cash balance. The company has resorted to financing ($1.8 billion since mid-2025), and this has boosted the pro forma cash balance to $1.5 billion. ONDS highlights this as an advantage to scale rapidly. However, cash generation remains a problem. The company used $38.7 million in operating activities for 2025 and expects cash usage to increase in the first half of 2026.

Image Source: Zacks Investment Research

Heavy reliance on OAS for revenue growth in the increasingly crowded drone space is also concerning.

The drone industry is experiencing rapid growth, with the unmanned aerial vehicle drones market expected to witness a CAGR of 16.77% from 2026 to 2035, according to a report from Precedence Research. Competition has intensified with drone companies such as Red Cat Holdings RCAT, AeroVironment AVAV and Unusual Machines UMAC vying to capture a larger share.

For ONDS, if a single large customer delays, reduces or cancels, revenues would decline materially. Also, revenues from Ondas Networks are expected to remain modest due to uncertain rail network buildout timelines.

Image Source: Zacks Investment Research

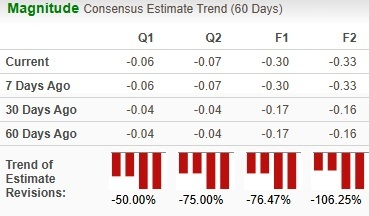

Given these factors, analysts have significantly revised their earnings estimates downwards for ONDS’ current year and the next year.

ONDS Stock in the Red

After a meteoric rise in 2025, ONDS is pulling back from its all-time highs. The stock has lost 30.7% in the last three months.

Image Source: Zacks Investment Research

AVAV and UMAC has lost 52.1% and 15.8% over the same time frame while RCAT is almost at breakeven.

The forward 12-month price/sales multiple for AVAV, UMAC and RCAT stand at 4.09X, 19.24X and 7.85X, respectively.

Conclusion: How to Approach ONDS Stock?

ONDS does offer compelling long-term potential while expanding the autonomous systems platform and strengthening its presence in the fast-growing drone market.

However, much of this opportunity remains forward-looking. Ballooning losses and risks tied to rapid scaling and acquisitions warrant a cautious approach in the near term. Its premium valuation exposes investors to sharp volatility and heightens downside risk in the near to medium term.

Until Ondas can demonstrate sustainable organic growth and make progress toward profitability, investors need to exercise caution.

At present, ONDS carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AeroVironment, Inc. (AVAV): Free Stock Analysis Report

Ondas Holdings Inc. (ONDS): Free Stock Analysis Report

Red Cat Holdings, Inc. (RCAT): Free Stock Analysis Report

Unusual Machines, Inc. (UMAC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).