Burlington Stores, Inc.’s BURL solid value-driven merchandising strategy and improving brand assortment continue to strengthen consumer demand, as reflected in the healthy comps trend, supporting its ability to drive sustained growth and gain market share in the off-price retail space. The company’s focus on better brands, sharper pricing and disciplined inventory management has been instrumental in reinforcing store traffic and customer engagement.

This strength was reflected in the company’s comparable sales trend during the fourth quarter of fiscal 2025, with comps increasing 4% year over year, significantly above management’s guided range of 0% to 2%. Notably, this growth came on top of 6% comps rise in the prior-year period, resulting in a robust 10% two-year comp stack, highlighting sustained demand momentum across its customer base.

A key driver behind this performance was Burlington’s ongoing elevation strategy, aimed at offering more recognizable brands, better quality merchandise and fashion-right products at attractive value prices. Management noted that higher-priced merchandise buckets delivered the strongest growth, signaling customers’ willingness to trade up when offered compelling value propositions. This also contributed to a mid-single-digit increase in average unit retail during the fiscal fourth quarter.

The company also benefited from strong trends in categories such as apparel, footwear, beauty and accessories, which helped offset softer performance in certain home-related segments affected by tariff-driven assortment gaps. Even with these challenges, Burlington’s merchandising and supply-chain teams effectively chased demand, enabling strong sell-through during the crucial holiday season.

Looking ahead, management remains optimistic about the sales outlook for fiscal 2026, guiding for 1% to 3% comps growth with potential upside. Supported by easier comparisons, improved inventory levels and continued progress on Burlington 2.0 initiatives, comparable sales are expected to remain a major driver of the company’s revenue and earnings growth trajectory. We expect comps to improve 3% year over year in fiscal 2026.

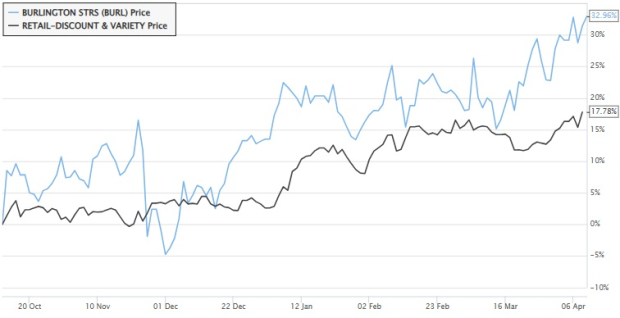

Burlington’s Price Performance, Valuation & Estimates

BURL stock has gained 33% in the past six months compared with the industry’s 17.8% growth.

Image Source: Zacks Investment Research

Burlington’s forward 12-month price-to-earnings ratio of 28.80X indicates a lower valuation compared with the industry’s average of 33.56X. BURL carries a Value Score of A.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Burlington’s current fiscal-year sales and earnings per share implies year-over-year growth of 9.7% and 15.5%, respectively. Earnings estimates for fiscal 2026 and 2027 have been upbound by 4 cents and 3 cents per share, respectively, in the past 30 days.

Image Source: Zacks Investment Research

Burlington currently carries a Zacks Rank #3 (Hold).

Key Picks

Some better-ranked stocks in the retail space are FIGS Inc. FIGS, Ross Stores Inc. ROST and Abercrombie & Fitch Co. ANF.

FIGS is a direct-to-consumer healthcare apparel and lifestyle brand, and it currently sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for FIGS’ current financial-year sales and earnings indicates growth of 11.7% and 15.8%, respectively, from the year-ago reported numbers. The company delivered a trailing four-quarter earnings surprise of 187.5%, on average.

Ross Stores operates as an off-price retailer of apparel and home accessories. It presently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for Ross Stores’ current fiscal-year earnings and sales implies growth of 10.1% and 6.3%, respectively, from the year-ago actuals. ROST delivered a trailing four-quarter average earnings surprise of 6.2%.

Abercrombie & Fitch operates as a specialty retailer of premium, high-quality casual apparel for men, women and kids. It currently has a Zacks Rank of 2.

The Zacks Consensus Estimate for Abercrombie & Fitch’s current fiscal-year earnings and sales implies growth of 8.6% and 4.3%, respectively, from the year-ago actuals. ANF delivered a trailing four-quarter average earnings surprise of 8.4%.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abercrombie & Fitch Company (ANF): Free Stock Analysis Report

Ross Stores, Inc. (ROST): Free Stock Analysis Report

Burlington Stores, Inc. (BURL): Free Stock Analysis Report

FIGS, Inc. (FIGS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).