Pembina Pipeline Corporation PBA, a prominent Canada-based energy infrastructure firm, operates an extensive network of pipelines along with storage and transportation assets. The company is strategically focused on sustainable, long-term growth, leveraging shifting market dynamics and robust customer demand. Looking ahead, Pembina plans to expand investments across LNG, LPG, gas-to-power projects and emissions-reduction initiatives. These forward-looking strategies highlight its dedication to balancing growth with environmental responsibility, strengthening its position in North America’s energy landscape while enhancing operational efficiency and profitability.

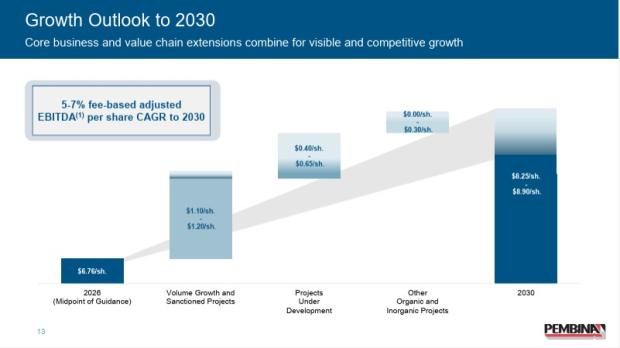

Recently, Pembina released its business update, highlighting strategic focus and growth outlook. The company targets 5-7% compound annual growth in fee-based adjusted EBITDA per share through 2030. This growth will be driven by higher utilization across existing assets, contributions from sanctioned projects entering service and a portfolio of development opportunities designed to extend the franchise.

Where Does Price Performance Stand for PBA?

In the past six months, PBA’s shares have gained 13.9%, underperforming the broader oil and energy sector's rise of 29.8% and the Oil & Gas Production and Pipelines sub-industry’s rally of 17.3%.

PBA’s Six-Month Stock Performance

Image Source: Zacks Investment Research

As the stock continues to underperform, investors are becoming increasingly cautious, seeking to understand the reasons behind the company's struggles and whether it’s wise to invest at this point. Let’s take a closer look at the factors contributing to the stock's decline and evaluate its core strengths.

Core Strengths of Pembina

Strong Visibility on Long-Term Earnings Growth: Pembina has provided clear guidance of 5-7% fee-based EBITDA per share growth through 2030, supported by visible drivers such as sanctioned projects, asset utilization gains and new developments. This is not purely aspirational — management highlighted that prior targets (2023-2026) are tracking within guidance despite external disruptions. The presence of long-term contracts and fee-based revenues reduces earnings volatility and enhances predictability, making the company attractive for investors seeking stable, compounding returns over a multi-year horizon.

PBA's 2030 Growth Outlook

Image Source: Pembina Pipeline Corporation

Exposure to Structural Growth in Canadian Energy Exports: Pembina is positioned at the center of expanding Western Canadian Sedimentary Basin growth, driven by rising LNG exports, pipeline expansions, petrochemical demand and global energy needs. Projects like TMX and LNG Canada are already increasing export capacity, while future developments (LNG, LPG, petrochemicals and data centers) are expected to further boost volumes. Since Pembina touches multiple commodities — oil, gas and NGLs — it benefits broadly from rising throughput across the entire system rather than relying on a single growth driver.

Emerging Growth Platforms Beyond Traditional Midstream: Pembina is actively expanding into new demand-driven segments such as LNG exports, petrochemicals and gas-to-power solutions for data centers (e.g., the Greenlight project). These initiatives extend its value chain and create incremental demand for its core services. Importantly, these are not speculative ventures — they are being pursued with long-term contracts and disciplined capital frameworks. This diversification positions Pembina to remain relevant even as energy markets evolve, supporting sustained growth beyond traditional pipeline operations.

Strong Execution Track Record and Capital Discipline: The company has demonstrated consistent operational excellence, including delivering projects on time and under budget, maintaining investment-grade credit ratings and meeting financial guidance historically. For example, Pembina expects to bring around $2 billion of projects online between 2024 and 2026, approximately 5% under budget. This disciplined execution reduces project risk, enhances investor confidence and ensures capital is deployed efficiently — key factors in infrastructure investing where cost overruns can significantly erode returns.

Risks That Could Hinder PBA's Growth

Heavy Dependence on Macro Energy Demand and Policy Support: Pembina’s growth outlook is closely tied to global energy demand, Canadian export expansion and supportive government policies. While current trends are favorable, any slowdown in LNG demand, regulatory changes, or geopolitical shifts could weaken the growth narrative. Management itself noted that not all aspirational targets (e.g., LNG expansion, petrochemical growth) are guaranteed, meaning part of the long-term outlook depends on external factors beyond the company’s control.

Exposure to Volume Risk Despite Fee-Based Model: While revenues are largely fee-based, they still depend on throughput volumes across pipelines and facilities. If upstream production slows due to weak commodity prices or reduced drilling activity, volumes flowing through Pembina’s system could decline. Even with contracts in place, lower utilization over time may limit growth and reduce operating leverage, particularly in a cyclical downturn in oil and gas markets.

Uncertainty Around New Growth Ventures: New initiatives such as data center power (Greenlight), petrochemical supply chains and LNG expansion introduce execution and demand risks. While these are positioned as contracted and disciplined investments, they still represent extensions into relatively newer areas. If customer demand fails to materialize as expected or if economics change, these projects may underperform, potentially diluting returns compared with traditional midstream assets.

Marketing Segment Weakness and Volatility: The company’s marketing and new ventures segment showed notable weakness in the fourth quarter due to narrower spreads and lower derivative gains. This segment can be volatile and less predictable compared with core pipeline operations. Continued underperformance here could offset gains from stable segments and drag overall earnings growth.

Final Verdict for PBA Stock

Pembina benefits from strong long-term visibility, backed by fee-based contracts, disciplined capital execution and exposure to structural growth in Canadian energy exports. The company’s expansion into LNG, petrochemicals and gas-to-power further strengthens its growth pipeline.

However, these positives are partly offset by the stock’s underperformance, reliance on macro energy demand and uncertainties tied to newer business segments. Volume sensitivity, despite a fee-based model and volatility in the marketing division, also remains a cause of concern. Given this mix of stable fundamentals and external risks, the stock lacks a strong near-term catalyst, making a hold strategy appropriate while awaiting clearer growth realization.

PBA’s Zacks Rank & Key Picks

Currently, PBA has a Zacks Rank #3 (Hold).

Investors interested in the energy sector may consider some better-ranked stocks like California Resources Corporation CRC, Permian Resources Corporation PR and Nabors Industries Ltd. NBR.While California Resources and Permian Resources sport a Zacks Rank #1 (Strong Buy) each at present, Nabors Industries carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

California Resources is an independent energy and carbon management company focused primarily on California. The company operates two reportable segments: oil and natural gas, and carbon management (Carbon TerraVault). The Zacks Consensus Estimate for CRC’s 2026 revenues indicates 2.8% year-over-year growth.

Midland, TX-based Permian Resources is an independent oil and gas company. The company solidifies its footprint in the Permian Basin as a major operator in one of the most productive oil regions in the United States. The Zacks Consensus Estimate for PR’s 2026 earnings indicates 20.3% year-over-year growth.

Hamilton-based Nabors Industries is one of the largest land-drilling contractors in the world, conducting oil, gas and geothermal land drilling operations. The Zacks Consensus Estimate for NBR’s 2026 earnings indicates 49.1% year-over-year growth.

Quantum Computing Stocks Set To Soar

Artificial intelligence has already reshaped the investment landscape, and its convergence with quantum computing could lead to the most significant wealth-building opportunities of our time.

Today, you have a chance to position your portfolio at the forefront of this technological revolution. In our urgent special report, Beyond AI: The Quantum Leap in Computing Power , you'll discover the little-known stocks we believe will win the quantum computing race and deliver massive gains to early investors.

Access the Report Free Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Nabors Industries Ltd. (NBR): Free Stock Analysis Report

Pembina Pipeline Corp. (PBA): Free Stock Analysis Report

California Resources Corporation (CRC): Free Stock Analysis Report

Permian Resources Corporation (PR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).