Analysts keep hiking their revenue forecasts for Micron Technologies (MU), as well as their price targets. Thus, its forecasted adjusted free cash flow projections (FCF) could push MU stock 43% higher to $610 per share over the next year.

MU closed up 1.42% yesterday at $426.56. It's been on a tear upward since bottoming out on March 30 at $321.80. However, MU is still below a recent peak of $461.73 on March 18.

Can’t Get Enough Options?: Join the list for Barchart’s daily unusual options report, delivered free.

MU stock - last 3 months - Barchart - April 13

MU stock - last 3 months - Barchart - April 13 I discussed Micron's valuation after analyzing its adjusted. FCF in a March 22 Barchart article, “Micron Technology Hikes Its Dividend 30% Due to Surging FCF - MU Is Worth 34% More - What's the Best Play?”

This article will update the MU price targets in that valuation, and the short-put plays that are still very attractive.

Higher Revenue and Adj. FCF Forecasts

Since my last article, analysts surveyed by Seeking Alpha have hiked their revenue estimates. This is due to surging demand for Micron's DRAM and NAND memory chips, integral to AI-related cloud and data center servers and other applications.

For example, revenue for the year ending Aug. 2027 is now forecasted to hit $165.99 billion, up from $159.25 billion three weeks ago, as seen in my previous Barchart article.

That implies, for the next 12 months (NTM), revenue will average $137.38 billion. So, using a 28.75% adj. FCF margin, which is equal to Micron's first-half margin (ending Feb. 26), Micron could generate almost $40 billion in adj. FCF:

$137.88 billion NTM revenue estimate x 0.2875 adj. FCF margin = $39.5 billion adj. FCF

That's up from my prior estimate of $38.5 billion. Moreover, for the year ending Aug. 2027, one and a quarter calendar years from now, Micron could produce:

$165.99 billion FY 27 revenue est. x 0.2875 = $47.7 billion adj. FCF

This range of $39.5 billion to $47.7 billion ($43.6 billion on average) is 58% higher than its run-rate FCF last quarter, when it generated a 28.9% adj. FCF margin.

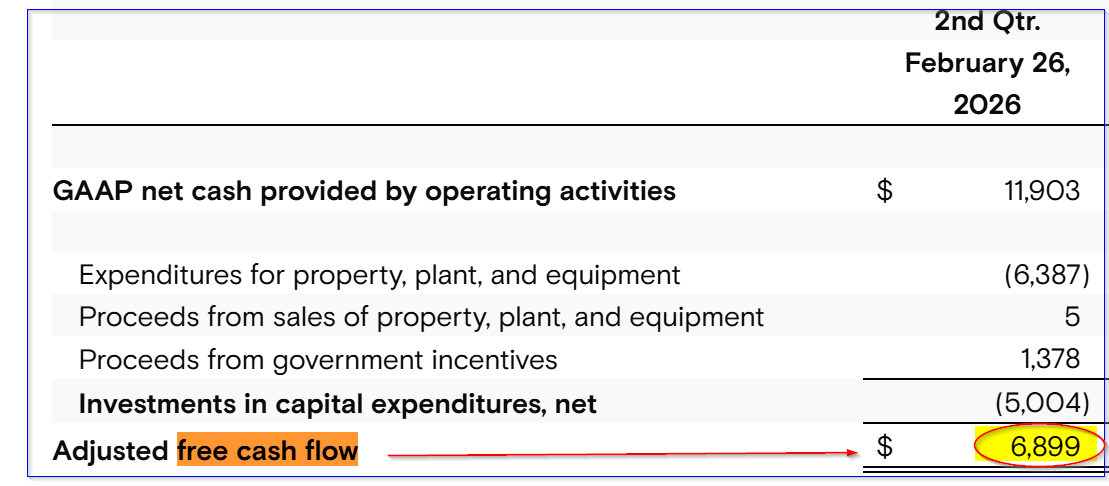

Micron's fiscal Q2 adj. FCF - March 18 earnings release

Micron's fiscal Q2 adj. FCF - March 18 earnings release For example, $6.899 billion x 4 = $27.596 billion run rate adj. FCF

So, $43.6 billion avg FCF / $27.596 billion = 1.5799 = +58% higher.

This implies a significantly higher valuation for MU stock. Here's why.

MU Price Targets

Yahoo! Finance reports that Micron's market value as of Monday's close was $481.05 billion. That implies that its run-rate FCF yield is about 5.736%:

$27.6b / $481b = 0.05738

In other words, assuming Micron keeps generating $6.9 billion in adj. FCF each quarter, and if it were to pay out 100% of that to shareholders over the next year, the dividend yield would be over 5.7%.

Therefore, we can use this to project its target valuation using our new revenue and adj. FCF estimates.

For example, dividing the NTM adj. FCF of $39.5 billion from above by 5.738%:

$39.5b / 0.0574 = $688 billion market value

That's over $200 billion more than the present $481 billion market cap, and implies a 43% increase in value over the next 12 months:

$688b / $481b = 1.43 -1 = +43% upside

That implies the new price target (PT) is $610:

$1.43 x $426.56 price today = $609.98

That's higher than my prior $566.64 PT three weeks ago. Moreover, analysts surveyed by Yahoo! Finance now have an average PT of $533.72, up from $512.67.

However, given that there is no guarantee MU will rise to this point, it makes sense to take advantage of high put option premiums now. That way, an investor can set a lower potential buy-in point, as well as get paid while waiting.

Shorting OTM MU Puts

I discussed this in my last article, when I suggested shorting the April 24 expiry $400 strike price put option contract. That put strike price was 6% below the spot price, and had an attractive 5.95% yield (i.e., $23.80/$400.00).

Today, that put option price is down to $10.05 from $23.80, making it a very profitable trade so far. Short-put investors will likely still hold on to that play until its premium wears down further.

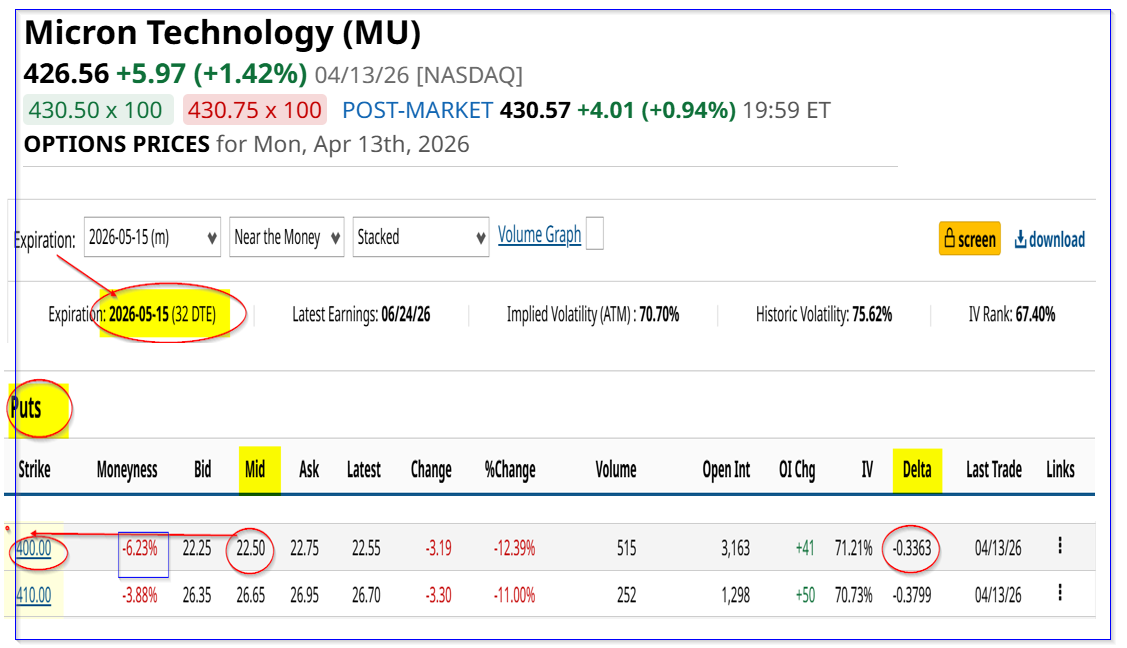

Moreover, one month out of expiry puts still has high yields. For example, look at the May 15 expiry contract shows that the $400 put strike price has a midpoint premium of $22.50.

MU puts expiring May 15 - Barchart - As of April 13, 2026

MU puts expiring May 15 - Barchart - As of April 13, 2026 That implies an investor who secures $40,000 with their brokerage firm can enter an order to “Sell to Open” 1 put contract. The account will then receive $2,250. So, the yield is:

$2,250 / $40,000 = 0.05625 = 5.625%

This is similar to last month's 5.95% yield at the same strike price.

That means that over the two months, a short-seller would make a total of 11.575% (i.e., 5.95% +5.625%).

If this keeps up, it's the same as seeing MU stock rise to $475.93 over the next two months, for a buy-and-hold investor at today's price. Moreover, the extra income for a short seller of these puts lowers the potential buy-in point in case MU falls to the strike price.

The bottom line is that this is an attractive way for an investor to play MU stock, given its huge upside.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Analysts Hike Their Micron Estimates, Pushing MU Stock Price Targets Higher Anthropic Just Triggered a Frenzied Selloff in Fastly Stock. Should You Buy the Dip? Higher Aluminum Prices Are a Win for Alcoa Stock, Says Morgan Stanley. Should You Buy AA Here? How to Buy Nvidia Stock for a 27% Discount or Achieve an 8% Annual Return