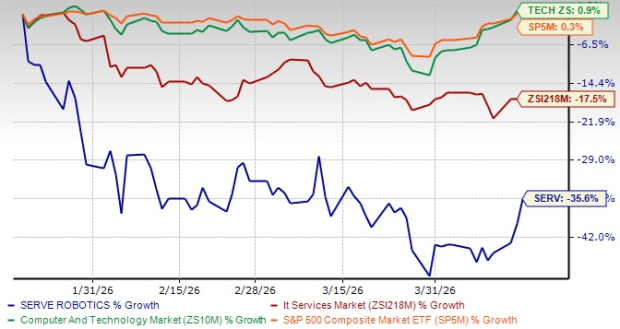

Serve Robotics Inc. SERV have plunged 35.6% over the past three months, sharply underperforming the Zacks Computers - IT Services industry’s 17.5% decline. The stock has also underperformed the broader Zacks Computer and Technology sector and the S&P 500 in the same period, as evidenced by the chart below.

SERV’s Past 3 Months Price Performance

Image Source: Zacks Investment Research

The stock has also underperformed its industry peers, including C3.ai, Inc. AI and Cognizant Technology Solutions Corporation CTSH, down 27% and 28.7%, respectively, in the same time frame.

Key Factors Affecting SERV’s Performance

Investor sentiment around Serve Robotics remains cautious despite strong expansion signals. This leading autonomous sidewalk delivery company continues to face pressure from high operating costs and an uncertain path to profitability. Non-GAAP operating expenses stood at $69 million in 2025, reflecting continued investment across fleet deployment, technology development and market expansion.

The company reported a non-GAAP net loss of $72.9 million in 2025, up from $24.6 million in 2024, while adjusted EBITDA stayed deeply negative at $78.6 million. These trends highlight the extended path toward breakeven as spending remains elevated. The company is also entering a phase where newly deployed robots operate below optimal efficiency, which can weigh on margins as utilization improves over time.

Further, the business remains capital-intensive, with continued investments required across infrastructure, autonomy development and acquisitions, which are expected to push 2026 non-GAAP operating expenses to $160-$170 million. Supply-chain lead times and the need to optimize existing fleet utilization before further expansion also create execution risks. While revenue growth is strong, the low base and reliance on future monetization streams such as advertising and data services add uncertainty to long-term earnings visibility.

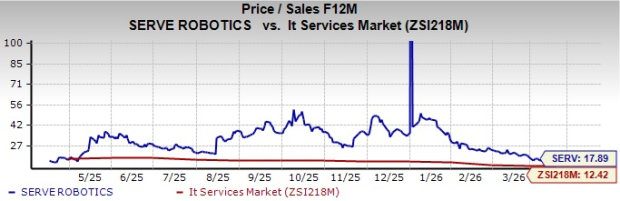

Taking a Look at SERV Stock’s Valuation

Serve Robotics stock is currently trading at a premium. SERV is currently trading at a forward 12-month price-to-sales (P/S) multiple of 17.89X, well above the industry average of 12.42X. Other industry players, such as C3.ai and Cognizant, have P/S of 5.56X and 1.27X, respectively.

Image Source: Zacks Investment Research

Earnings Estimates Remain Under Pressure for SERV

Earnings expectations for Serve Robotics continue to reflect near-term challenges. Estimates remain weak as the company continues to invest heavily in scaling operations, technology development and market expansion. Persistent losses and limited profitability visibility have weighed on forward projections. The Zacks Consensus Estimate for the loss per share in 2026 has widened to $2.39 over the past 30 days compared with a year-ago estimate of a loss of $1.63, reinforcing concerns around the earnings trajectory.

Image Source: Zacks Investment Research

That said, some underlying trends remain supportive of the company’s long-term growth direction. Despite the earlier sharp decline, the stock showed a noticeable rebound toward the end, indicating a pickup in momentum. This improvement aligns with strong revenue growth, expanding fleet deployment and rising delivery volumes, which supported better operational traction. Continued progress in partnerships and early traction in advertising and data monetization also adds to improving visibility.

Fleet Expansion Supports Serve Robotics’ Scale and Leverage

Serve Robotics continues to expand its fleet to strengthen operating scale and improve long-term economics. A larger deployed base supports higher delivery volumes while enabling better route density and data collection across urban environments. As scale increases, efficiency gains are expected to improve utilization and reduce per-unit costs over time.

The fleet reached 2,000 deployed robots by the end of 2025, with nearly 1,000 units added in the fourth quarter alone. Delivery volumes increased 53% sequentially, reflecting a stronger contribution from new deployments. Continued ramp-up of newly deployed robots is expected to further support utilization and operating leverage.

Partnerships Improve Serve Robotics’ Demand Access and Utilization

Serve Robotics is strengthening its delivery ecosystem through integrations with major platforms, improving access to high-frequency demand. A multi-platform setup allows robots to dynamically accept orders across networks, increasing delivery density and reducing idle time. This approach supports more consistent utilization across different markets.

Partnerships with Uber Eats and DoorDash provide access to more than 80% of the U.S. food delivery market, while collaborations with restaurant brands continue to expand. The company recently added White Castle as a partner, further increasing order density across markets. The merchant base has grown to more than 4,500 restaurants and retail partners, supporting higher volumes and improved monetization potential as the fleet scales.

Healthcare Expands Serve Robotics’ Revenue Mix

Serve Robotics is extending its platform beyond sidewalk delivery into healthcare automation, creating a more diversified revenue base. The acquisition of Diligent Robotics introduces hospital-based operations, where robotic systems operate in structured indoor environments with recurring demand. This expansion supports long-term stability by adding contractual and predictable revenue streams.

Diligent Robotics brings nearly 100 deployed robots across more than 25 hospitals, with each facility generating over $200,000 in annual revenues. The healthcare segment is expected to contribute approximately $7 million in 2026, supported by existing contracts. This vertical also strengthens data capabilities by adding a new operating environment, enhancing model performance across different use cases.

Geographic Expansion Supports Serve Robotics’ Growth Visibility

Serve Robotics continues to expand its footprint across multiple cities, increasing access to new demand pools and improving overall network density. Expansion into diverse urban environments supports stronger utilization, while also generating varied data that enhances autonomy performance. A broader geographic presence allows the company to scale operations more efficiently over time.

By the end of 2025, operations spanned 20 cities across six major metropolitan areas, reaching more than 1.7 million households. The company is also in discussions to expand into additional U.S. and international markets, including Canada and Australia. Increasing geographic scale supports higher delivery volumes, improved route optimization and stronger long-term growth visibility.

How to Play Serve Robotics Stock?

Serve Robotics continues to face near-term pressure from high operating costs, widening losses and an uncertain path to profitability. Elevated spending on fleet expansion, technology development and market scaling is weighing on margins, while earnings estimates remain under pressure. The stock is also trading at a premium valuation, which may limit near-term upside.

That said, underlying growth trends remain encouraging. Expanding fleet size, rising delivery volumes and strengthening partnerships are improving operational traction and demand visibility. Progress in new verticals such as healthcare and continued geographic expansion further support long-term growth potential. With a Zacks Rank #3 (Hold), the stock appears suitable for holding, while investors may wait for clearer signs of profitability and execution stability.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cognizant Technology Solutions Corporation (CTSH): Free Stock Analysis Report

C3.ai, Inc. (AI): Free Stock Analysis Report

Serve Robotics Inc. (SERV): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).