Under Armour, Inc.’s UAA fiscal 2026 transformation highlights meaningful progress in simplifying its business and improving execution consistency. The company’s restructuring efforts are increasingly translating into a more agile operating model, setting the stage for stabilization and long-term value creation.

A major component of the transformation has been organizational restructuring and cost discipline. Under Armour has streamlined its structure, reduced decision-making layers and aligned teams under a category-managed model. These changes, along with targeted leadership realignments, are enhancing accountability, improving speed to market and ensuring tighter coordination across product and regional teams.

Operational streamlining continues to drive efficiency gains. The company has already cut roughly 25% of its SKUs and is refining its product assortment to focus on fewer, higher-impact offerings. Inventory management is improving, planning is more precise, and product segmentation is clearer. Together, these steps are enhancing pricing discipline, reducing inefficiencies and reinforcing brand positioning.

The financial impact of these efforts is becoming evident in cost metrics. Adjusted SG&A declined 7% year over year to $563 million, attributable to lower marketing spend due to timing, with a greater portion of fiscal 2025 marketing investments recognized earlier, alongside continued benefits from restructuring actions and disciplined control of discretionary expenses. Overall, the company has incurred $224 million in restructuring-related charges as of the third quarter of fiscal 2026 and expects up to $255 million in total, while generating $35 million in savings in fiscal 2025 and targeting an additional $55 million in fiscal 2026.

Beyond cost savings, Under Armour’s transformation is reshaping its go-to-market strategy and product philosophy. By emphasizing a category-managed model, tighter assortments and higher full-price realization, the company is shifting toward a more premium and focused approach. Combined with ongoing efficiency initiatives, these actions are positioning Under Armour for improved margins, steadier performance and sustainable growth over the long term.

UAA’s Price Performance, Valuation & Estimates

Shares of the company have gained 31.4% in the past six months compared with the industry’s 1.4% growth.

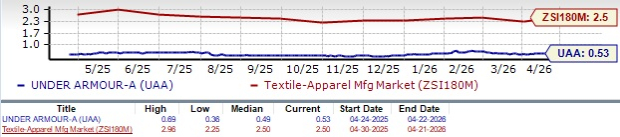

Image Source: Zacks Investment Research

From a valuation standpoint, Under Armour is trading at a forward 12-month price-to-sales ratio of 0.53X, down from the industry average of 2.50X. UAA has a Value Score of B.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Under Armour’s fiscal 2026 earnings implies a year-over-year decline of 64.5%, whereas the same for fiscal 2027 indicates an uptick of 98.4%. Estimates for fiscal 2026 and 2027 have been unchanged in the past 30 days.

Image Source: Zacks Investment Research

Under Armour currently sports a Zacks Rank #1 (Strong Buy).

Other Key Picks

Some other top-ranked stocks are FIGS Inc. FIGS, Tapestry, Inc. TPR and Tilly's, Inc. TLYS.

FIGS is a direct-to-consumer healthcare apparel and lifestyle brand, and it currently sports a Zacks Rank of 1. The company delivered a trailing four-quarter earnings surprise of 187.5%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for FIGS’ current financial-year sales and earnings indicates growth of 11.8% and 26.3%, respectively, from the year-ago reported numbers.

Tapestry, which was formerly known as Coach, Inc., is the designer and marketer of fine accessories and gifts for women and men in the United States and internationally. It currently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for Tapestry’s current fiscal-year earnings and sales implies growth of 26.5% and 11.2%, respectively, from the year-ago actuals. TPR delivered a trailing four-quarter average earnings surprise of 12.8%.

Tilly's is a specialty retailer in the action sports industry, selling clothing, shoes and accessories. It has a Zacks Rank of 2 at present.

The Zacks Consensus Estimate for Tilly's current fiscal-year earnings and sales implies growth of 70.7% and 2.6%, respectively, from the year-ago actuals. TLYS delivered a trailing four-quarter average earnings surprise of 147%.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Tilly's, Inc. (TLYS): Free Stock Analysis Report

Under Armour, Inc. (UAA): Free Stock Analysis Report

Tapestry, Inc. (TPR): Free Stock Analysis Report

FIGS, Inc. (FIGS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).