Software stocks have had a bruising start to the year. Once viewed as steady compounders with recurring revenue and high switching costs, many enterprise software names have come under pressure amid fears that artificial intelligence (AI) could fundamentally disrupt their business models. Some investors have even dubbed the selloff a “SaaSpocalypse.”

However, not everyone is convinced the sky is falling. Legendary investor Michael Burry, best known for his prescient bet against the U.S. housing market, appears to believe that at least part of the recent downturn in software stocks has been driven more by technical factors than by deteriorating fundamentals. In a Substack post, Burry indicated he planned to add shares of Salesforce last Thursday, suggesting he sees an opportunity where others see disruption.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The move raises a critical question for investors: Is this a classic Burry-style contrarian call or a premature attempt to catch a falling knife in a sector facing real structural change? Let’s take a closer look.

About Salesforce Stock

Salesforce is the world’s leading provider of cloud-based customer relationship management (CRM) software. The company pioneered the Software-as-a-Service (SaaS) model, allowing businesses to manage sales, service, and marketing via a web browser rather than installed hardware. Its market cap currently stands at $153.1 billion.

Shares of the cloud computing software giant have fallen 34% on a year-to-date (YTD) basis. Software stocks, including CRM, have come under pressure amid worries about the effect of AI on software vendors and their subscription pricing models.

www.barchart.com

www.barchart.com Burry Buys Salesforce on the Dip After the “SaaSpocalypse” Selloff

Software stocks had a tough start to the year. Companies such as ServiceNow, Salesforce, and Intuit have come under heavy pressure in recent months, hitting multi-year lows as many investors viewed them as potential victims of AI disruption. Investors have been debating whether traditional enterprise software vendors can hold up against emerging AI-powered competitors. The selloff intensified amid the Middle East conflict. With the software sector becoming deeply oversold, some investors, including a legendary one, stepped in to buy the dip.

Michael Burry, famous for his early bet against the U.S. housing market and for being portrayed by Christian Bale in the movie “The Big Short,” believes that the recent selloff was driven more by technical factors than by weakening business fundamentals. Burry wrote in a Substack post last Wednesday that a “reflexive positive feedback loop” between declining stock prices and stress in bank debt linked to software companies amplified the selloff, ultimately creating what he now views as a buying opportunity. “I do not believe the technical pressures brought on by the private credit/software debt issues are big enough to affect these stocks for much longer,” he noted.

Burry said in a post that he planned to initiate a position in Salesforce the following day. Burry pointed out that the company does not depend on the private credit markets currently under stress, which he believes provides a “margin of safety.” If he followed through on his plan, his purchase price for CRM stock fell within the April 16 daily trading range of $178.57 to $184.55. Zooming in, since Burry was expected to buy the stock early Thursday, the likely purchase range narrows to roughly $179 to $184. In any case, his position is currently in the red, as CRM stock is taking another big beating today.

That said, Burry isn’t bullish on the entire software sector. He draws a clear line between companies he believes can withstand the “software apocalypse” and those he thinks could be severely disrupted by advanced large language models (LLMs). Burry’s move suggests he views Salesforce as belonging to the first camp. He also pointed out that Salesforce does not depend on private credit markets. “I do see several handfuls of companies seriously affected by advanced [LLMs] for specific reasons of the business models,” he said. “I do not see this for my selected companies and a good number of others, all of which I have just about finished analyzing forensically, competitively, and fundamentally as to investment potential.”

Salesforce CEO Dismisses Concerns Over AI Disruption

Salesforce CEO Mark Benioff told The Wall Street Journal in an interview published Sunday that AI is enhancing Salesforce’s value proposition, adding that AI startups and rivals can’t simply “vibe-code” their own sales-management tools to match Salesforce’s standards in security, compliance, and other critical features. “People think we have our back against the wall when in fact the opportunity has never been greater,” Benioff said.

In the interview, Benioff pointed to several catalysts he believes could help pull Salesforce out of its recent slump:

First, the company’s flagship Agentforce platform is picking up momentum after a sluggish start. The report noted that it is now being used by 23,000 customers out of a total base of 150,000 to build autonomous agents. Momentum has been bolstered by deeper integrations, such as the February 2026 expansion with Anthropic, allowing Agentforce tools to be accessed directly within Claude. Second, Salesforce plans to roll out a new AI platform, codenamed Agent Albert, by the end of this year. The tool would be capable of learning from its users and taking actions on their behalf automatically, the report said. Finally, Salesforce’s investment in Anthropic may be a meaningful catalyst. The company has invested more than $300 million in the AI startup since 2023, and Anthropic is reportedly considering launching an initial public offering as early as this year. Anthropic was valued at roughly $4 billion to $5 billion in 2023 before experiencing explosive growth, with its valuation approaching $350 billion by the end of 2025. It is currently valued at $380 billion.Could AI Disrupt Salesforce’s Business Model?

Well, to assess whether investors should follow Burry’s lead on Salesforce, let’s take a closer look at the company, particularly its business model, and how exposed it may be to AI disruption risks. And this is where the picture becomes more complicated. That’s because the core of Salesforce’s business model, charging per human “seat,” is directly threatened by AI productivity.

Salesforce user seats or user licenses are personalized access passes that determine the scope of features, data, and applications an employee or external user can access within a Salesforce organization. Every user must have exactly one user license assigned to them. Seat-based licenses are paid as a recurring monthly fee per person. However, AI agents that automate customer support and sales tasks may reduce the total number of human “seats” needed by enterprises, cannibalizing this primary revenue stream. If AI agents can automate 30-50% of the work previously done by humans, customers will naturally need fewer licenses. This year alone, we’re witnessing the rise of desktop agents capable of managing data, applications, and communications on a computer.

Moreover, there is a narrative that much of office work will eventually be handled by AI agents. In that scenario, software companies that charge per user could see sales slump and may be compelled to move away from the subscription model. And as we move into the agentic AI era, I believe the likelihood of such an outcome is gradually increasing (unless software companies take actions that prove otherwise). Of course, Salesforce has Agentforce, but as of the end of FY26, it generated only $800 million in annual recurring revenue (ARR), compared with the company’s total annual revenue of $41.5 billion.

There’s also a risk that the growing capabilities of LLMs (such as OpenAI/Anthropic) will enable companies to build their own CRM systems. If generic, cheaper AI solutions become “good enough,” they could threaten Salesforce’s premium, proprietary data moat. However, I currently see this risk as relatively limited. Although it may be possible to “vibe-code” sales-management software, such tools would likely lack the critical enterprise-grade capabilities that Salesforce offers.

Is CRM Stock a Buy Right Now?

Putting it all together, I don’t see CRM stock as offering an attractive risk/reward profile at the moment, given the risks outlined above. With that, I don't believe investors should follow Burry’s lead, as I don’t think this disruption has fully played out yet. There’s always a possibility that new models from OpenAI or further developments from Anthropic could emerge throughout the year and trigger another wave of selling in the sector. Moreover, the recent rebound in CRM stock and other names in the sector appears to be driven more by short covering than by underlying fundamentals.

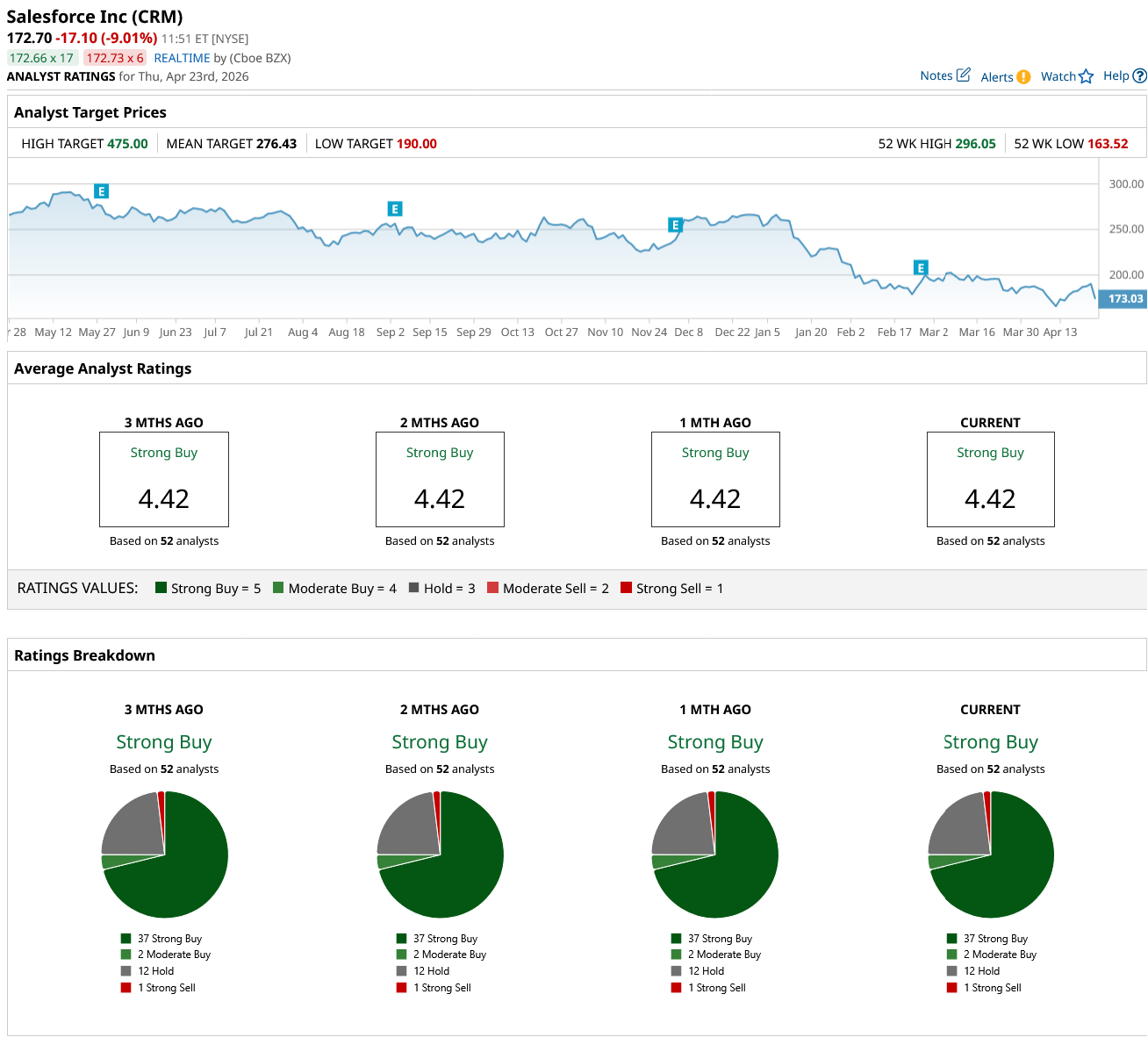

Still, Wall Street analysts remain bullish on Salesforce, giving the stock a consensus “Strong Buy” rating. Out of the 52 analysts covering CRM stock, 37 rate it as a “Strong Buy,” two advise a “Moderate Buy,” 12 give a “Hold” rating, and one considers it a “Strong Sell.” The mean price target for CRM stock is $276.43, which is 45.6% above Wednesday’s closing price.

www.barchart.com

www.barchart.com On the date of publication, Oleksandr Pylypenko did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

John Ternus Is Taking Over at Apple. Is That a Good Thing for AAPL Stock? Legendary Investor Michael Burry Is Shrugging Off the Software Apocalypse (Sort of) and Buying Salesforce Stock. Should You? How Long Will It Take for a Dramatic AI Pivot to Start Benefitting Allbirds Stock Investors? A $100 Billion Reason to Buy Amazon Stock Here