Bitcoin (BTCUSD) has been pressured for quite some time now. While in 2026, it is down by more than 10%; over the past year, the decline has been even sharper at close to 16%. Interestingly, its so-called status of “Digital Gold” was not reflected amid the latest flare-up in the Middle East, as investors still flocked to the classic safe-haven asset of gold to safeguard their portfolios.

However, this is not stopping believers. In fact, they are doubling down on buying the world's most popular and valuable cryptocurrency.

Join 200K+ Subscribers: Find out why the midday Barchart Brief newsletter is a must-read for thousands daily.

No Scaring Strategy Away From Bitcoin

While the world may have continued to ignore Bitcoin, the world's largest holder has been loading up. Michael Saylor-led Strategy (MSTR) (formerly MicroStrategy) has bought close to 75,000 bitcoins since the war started. Notably, the first two weeks of March saw the company accumulate more than 40,000 bitcoins, while its most recent purchase was of 34,164 more for a total value of about $2.54 billion. In total, Strategy now owns 815,061 bitcoins in total for a cumulative value of over $61 billion. More importantly, it now controls almost 4% of the total supply of Bitcoin in the global market.

This has convinced one of the oldest and privately held investment management firms to own additional shares of Strategy. The Capital Group, through its flagship American Funds, has purchased 4.32 million additional shares of the company for a cost of $747 million. The fund now owns 10.33 million shares of the company in total, which is worth close to $1.8 billion.

Known for thinking in years and not in quarters, this endorsement from American Funds certainly bodes well for Strategy, whose shares are already up over 18% for the year.

www.barchart.com

www.barchart.com Key components of this have been its valuation and management.

Michael Saylor's approach to managing Strategy's Bitcoin treasury has stood apart from anything else in the corporate world, and the mechanics behind it are certainly laudable. The company has built a sustainable method that involves issuing convertible equity and continuously refinancing its debt obligations, with every move oriented around a single aim of accumulating more Bitcoin. What makes this particularly compelling is how the structure interacts with volatility rather than running from it. By using leverage as an active tool rather than a passive liability, Strategy can turn Bitcoin's price swings into a compounding engine, one that works in favor of shareholders when conditions align.

Further, the premium at which Strategy trades relative to its Bitcoin net asset value is the other piece of the puzzle worth examining closely. During the peaks of prior Bitcoin cycles, that premium expanded to levels that reflected the full heat of market enthusiasm, something that tends to visit the asset class with some regularity each year. At present, that premium has pulled back considerably from those earlier extremes, which is actually a meaningful setup for what comes next. When Bitcoin enters its next sustained rally, history suggests the premium will begin to rebuild.

As that happens, equity issuance shifts become value-accretive because the company is effectively raising capital at a valuation that exceeds the underlying asset, allowing it to acquire more Bitcoin per dollar of new equity than would otherwise be possible. That dynamic, when it kicks in, creates a self-reinforcing loop that has the potential to generate substantial returns for those holding the stock.

Shaky Q4

Strategy's long-term strategic initiatives may be sound, but its results for the most recent quarter were the furthest from it.

Although the company's results were mixed with a beat on revenue and a miss on earnings, the miss in the latter was substantial. However, a shift to fair value accounting and a decline in Bitcoin prices were to blame.

Revenues for the quarter, which are entirely from its software business, came in at about $123 million. This was up just 2% from the prior year. Losses increased manifold to $42.93 per share from a loss of just $3.03 per share in the year-ago period, also coming in much higher than the consensus estimate of a loss of $0.08 per share.

However, the cash balance of the company swelled in 2025 to $2.3 billion, with just $31.3 million in short-term debt on its books.

BTC yield dropped to 22.8% in 2025 from a considerable 74.3%. Yet, the company managed to achieve profits of $8.9 billion in its BTC holdings while also adding 101,873 bitcoins to its pile in the year.

Analyst Opinion on MSTR Stock

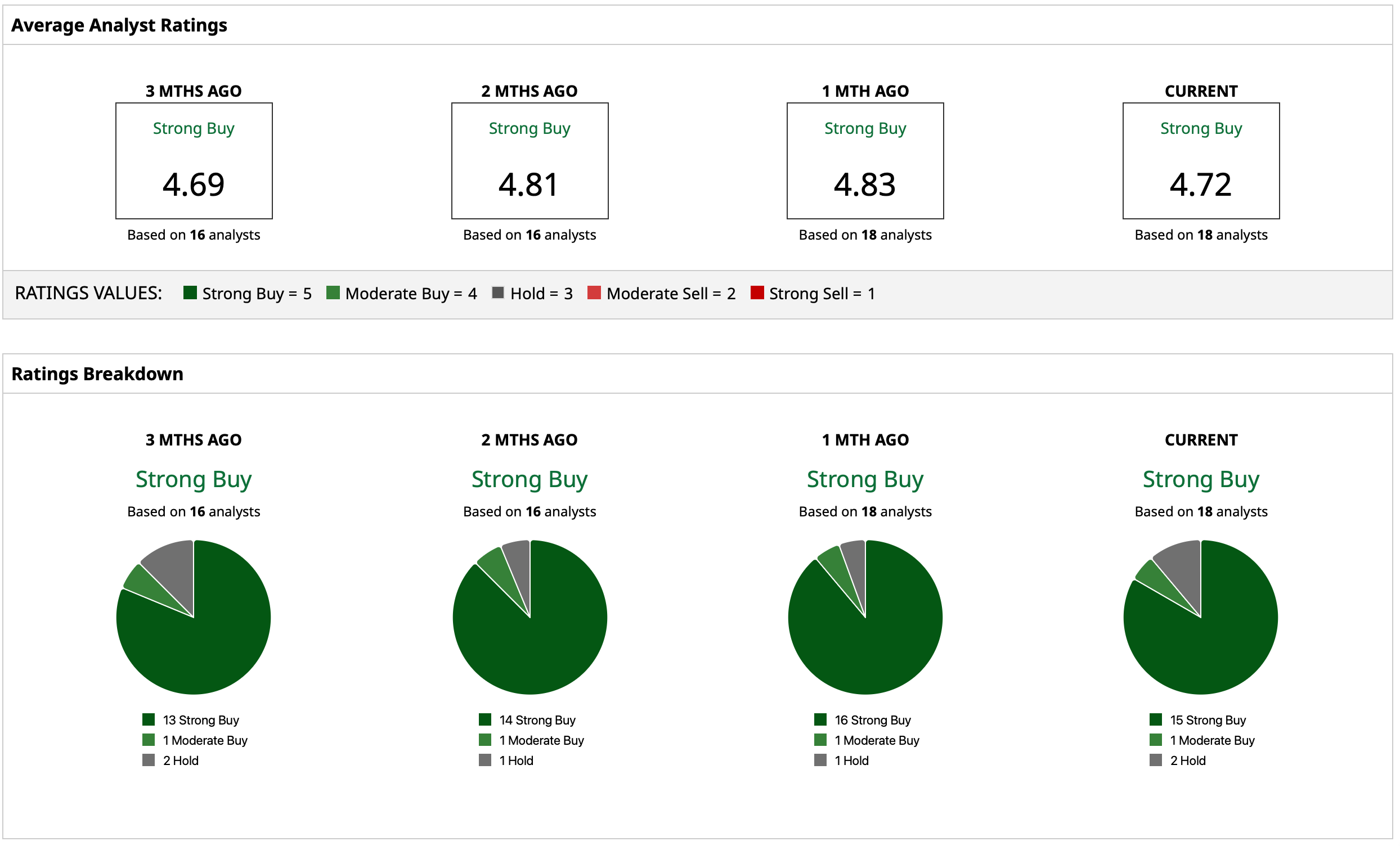

Thus, analysts have attributed an overall consensus rating of “Strong Buy” for MSTR stock, with a mean target price of $360.06. This indicates an upside potential of more than 100% from current levels. Out of 18 analysts covering the stock, 15 have a “Strong Buy” rating, one has a “Moderate Buy” rating, and two have a rating of “Hold.”

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Capital Group Is Doubling Down on MicroStrategy. Should You Buy MSTR Stock Here Too? Can Ethereum Make a Giant Comeback? Here’s the Bull Case. As Charles Schwab Unveils a New Crypto Trading Program, Is SCHW Stock a Buy, Sell, or Hold? What a New Generation of Traders in Commodities Might Mean For Markets