Orion S.A. OEC is currently trading at a discount to its industry. The market is assigning Orion some recovery value, while still demanding a discount for a near-term earnings reset.

That frames the debate: is the multiple anticipating a rebound or simply pricing in resilience during a down year?

Is OEC Priced for the Reset or for Recovery?

The fundamental setup points to a reset first. Management’s 2026 adjusted EBITDA guide of $160-$200 million implies a step down from $248 million in 2025. The drivers are a contract pricing reset in the Rubber segment and continued softness in Western tire builds, with rubber contract pricing for 2026 largely set. That reduces the scope for a quick upside surprise from pricing.

At the same time, Orion is not positioned like a company forced into defensive moves. Management is guiding to positive free cash flow in 2026 despite lower EBITDA, supported by reduced capital expenditures and working-capital programs. That cash emphasis can help keep valuation from compressing sharply, even if earnings dip.

The upshot is a balanced risk-reward profile over the next six to 12 months. Upside requires stabilization in tire activity and mix, while downside is buffered by cash discipline, cost actions and capacity tightening.

OEC’s Multiples: How the Market Is Framing Earnings Power

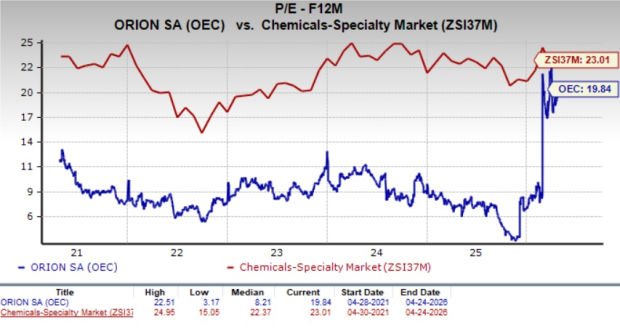

OEC currently trades at 19.84x forward 12-month earnings. That sits below the Zacks Chemicals Specialty industry’s multiple of 23.01. At 19.84x forward earnings, the market is threading a needle. The discount to the industry suggests investors are not assuming a clean recovery.

Over the past five years, OEC’s forward multiple has ranged from 3.17x to 22.51x, with a five-year median of 8.21x.

Orion’s 2026 Guideposts for a Risk Checklist

If results trend toward the low end of OEC’s 2026 adjusted EBITDA guidance, the current multiple can feel demanding in a down-earnings year. Tracking closer to the midpoint or better would likely require steadier volumes and improved mix versus the cautious assumptions embedded in guidance.

Seasonality also matters as management expects the first half of 2026 to contribute $90-$110 million of adjusted EBITDA. That front-half weighting makes early-quarter performance a key checkpoint. Investors should watch whether reliability, capacity actions and cost controls show up fast enough to support first-half delivery.

Finally, free cash flow is guided at $25-$50 million, supported by lower capital expenditures of around $90 million and continued working-capital discipline. For a valuation-driven stock, hitting the cash range can be as important as hitting the EBITDA range because it underwrites deleveraging and reduces financial risk.

OEC's Deleveraging Math: Why Cash Comes Before Returns

Leverage remains the constraint that can cap valuation upside. Net debt ended 2025 at $921 million, with trailing twelve months net debt-to-adjusted EBITDA of 3.71x. Finance costs increased to $62 million in 2025 from $49 million in 2024, which makes the cost of carrying leverage more visible when EBITDA steps down.

The amended credit agreement provides covenant headroom, but management’s priority is clear: generate cash, delever and protect flexibility. With growth projects deferred and capital returns constrained, the equity case depends more on balance-sheet progress than on shareholder payouts in 2026.

Orion’s Execution Levers That Can Protect Downside

When pricing is set and volumes are uncertain, controllables carry outsized weight. Orion improved execution in 2025, with North America reliability up more than 200 basis points and broader programs scaling, supporting service levels and working capital.

Capacity discipline is another lever. Management plans to rationalize three to five production lines across the Americas and EMEA, with three lines already closed, removing roughly 3%-5% of capacity. Tighter capacity can help stabilize fixed-cost absorption and protect margins even in a trough environment.

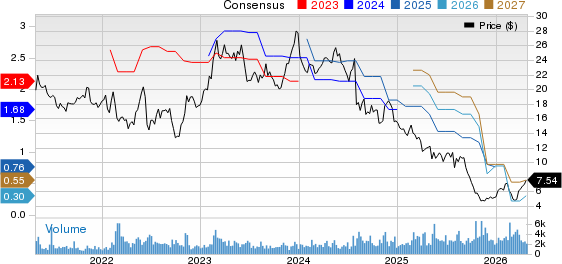

Orion S.A. Price and Consensus

Orion S.A. price-consensus-chart | Orion S.A. Quote

Practical Takeaway for Action-Oriented Investors

A more constructive view would need confirmation that end-market pressure is easing and that the company is converting execution into cash. Watch for evidence of Western tire build stabilization, improved regional and customer mix, and traction from cost actions, including the roughly $20 million run-rate savings target.

The valuation case strengthens if 2026 free cash flow lands within the guided range while leverage trends improve. OEC’s valuation fits a “Hold” framework until those signposts become clearer.

OEC currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

For context, Cabot Corporation CBT and The Chemours Company CC are among the industry names investors may compare for valuation and trend.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cabot Corporation (CBT): Free Stock Analysis Report

Orion S.A. (OEC): Free Stock Analysis Report

The Chemours Company (CC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).