For years, Amazon.com (AMZN) has been the quiet backbone of modern convenience, delivering everything from last-minute essentials to powering entire businesses through the cloud. Whether it’s one-click shopping or seamless streaming, the company has built a reputation for making complex systems feel effortless in everyday life.

Now, that same company is making headlines in a very different space – one powered not by boxes or bandwidth, but by silicon. The company’s in-house chips, once a behind-the-scenes effort inside Amazon Web Services (AWS), are quickly becoming a central piece of the AI race. Its Trainium lineup is already seeing surging demand, with newer versions nearly fully booked even before broad availability, signaling that customers are hungry for cost-efficient alternatives to traditional AI hardware.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The latest headline move brings Meta Platforms (META) into the picture. In a multiyear agreement, Meta plans to deploy tens of millions of Amazon’s Graviton processors – specifically the advanced Graviton5 chip – to power its expanding artificial intelligence (AI) ambitions. Unlike GPUs that dominate model training, these CPUs are increasingly critical for running AI agents. These are the systems designed for real-time reasoning, search, and multi-step task execution at massive scale. Built on cutting-edge 3-nanometer technology, Graviton5 is tailored for exactly this shift toward more autonomous, always-on AI systems.

Putting it all together, Amazon is not just offering AI through its cloud anymore, but building the core infrastructure behind it, chip by chip. Notably, these in-house designs are now finding traction beyond Amazon’s own ecosystem, bringing in external customers and helping balance the heavy costs of its AI buildout.

As demand keeps building and these chips take on a bigger role, Amazon is lining up multiple growth levers, turning its silicon push into a strong tailwind for AMZN stock.

About Amazon Stock

Amazon has evolved from its origins as an online bookstore into a technology leader, firmly positioned at the center of U.S. e-commerce and the broader digital economy. With a market capitalization of $2.84 trillion, its scale and reach extend far beyond retail, reflecting a diversified and deeply integrated business model.

Through AWS, the company provides critical infrastructure that powers a significant portion of the internet, while also maintaining a growing presence in streaming, smart devices, advertising, healthcare, and AI. Amazon is also designing its own chips, positioning itself deeper inside the AI infrastructure stack.

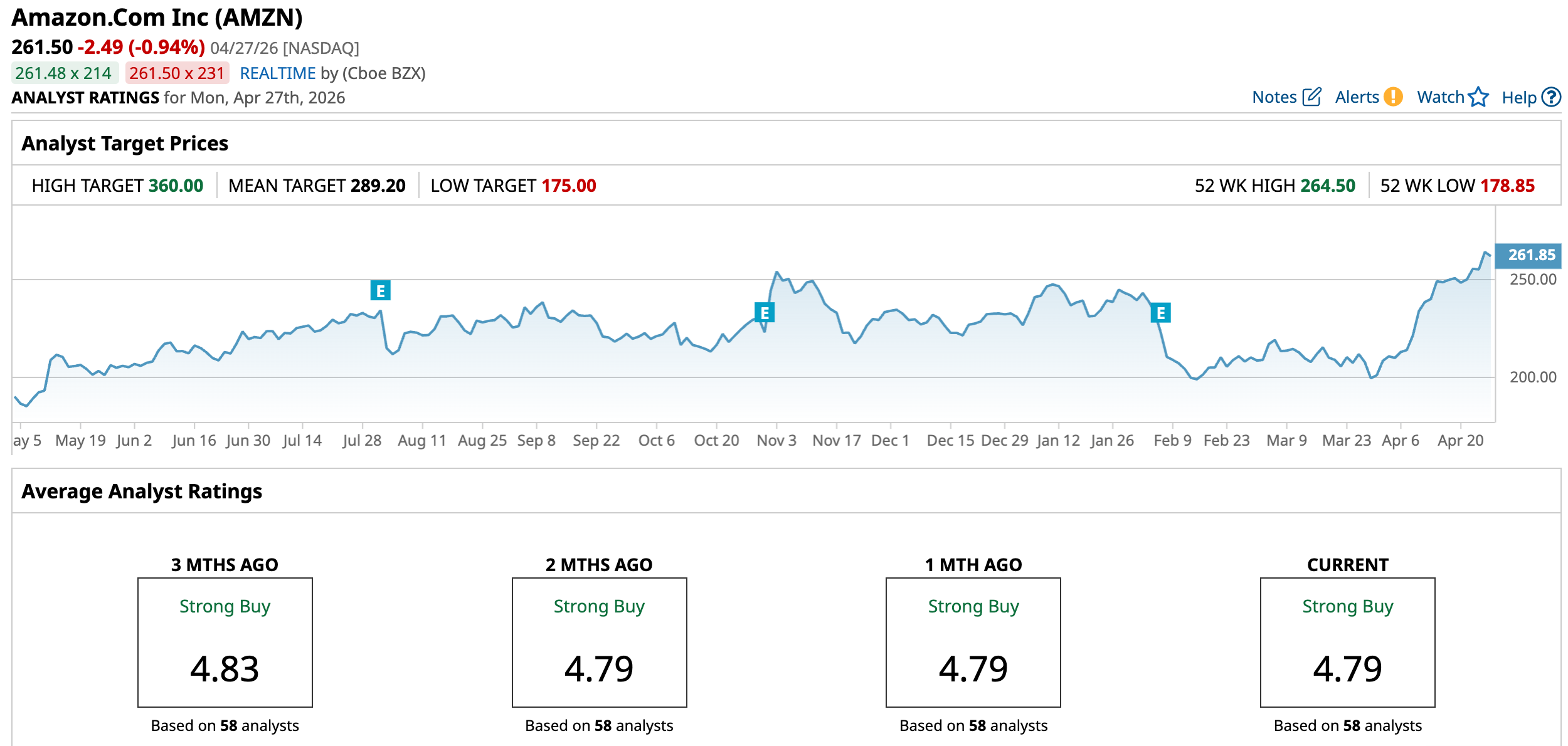

For a company as massive as Amazon, the long-term story still reads like a compounding machine. Over the past two decades, the stock has delivered an eye-popping 14,895% return, and even in the last ten years, it has climbed over 700%. More recently, the momentum has not faded much either, with shares up over 150% in the past three years.

Over the past 52 weeks, AMZN has gained 38.5%, recently touching a high of $264.50 on April 24. Nevertheless, the ride has not always been perfectly smooth.

In fact, 2026 didn’t start on the best note. After its Q4 results on Feb. 5, the stock fell for six straight sessions as investors reacted to Amazon’s plans to pour nearly $200 billion into AI, cloud infrastructure, robotics, and data centers, raising concerns around near-term margins and cash flow.

But sentiment has quickly turned again. A strong rebound over the past month, with the stock up 31.31%, has pushed AMZN back into positive territory for the year, now up 13.4% year-to-date (YTD). Fresh momentum last week, like a major deal with Meta Platforms and rising analyst optimism, has helped bring buyers back into the story.

Technically, AMZN stock has quickly flipped the script. The 14-day RSI, which was sitting close to oversold territory just last month, has now pushed firmly into overbought levels, highlighting a sharp pickup in momentum. Meanwhile, rising volumes are backing the move, signaling stronger buying interest behind the rally.

The MACD oscillator is flashing a bullish signal, with the MACD line rising above the blue signal line and both trending upward. Positive and rising histogram bars reflect growing confidence among the buyers.

www.barchart.com

www.barchart.com Valuation-wise, AMZN stock trades at a premium, priced at 32.94 times forward adjusted earnings and 3.51 times sales. That’s above sector averages, but compared to its own historical medians, they are cheaper than usual. With rising chip demand and fresh third-party deals adding momentum, the valuation feels more justified than stretched for a company scaling AI, cloud, and custom silicon together.

A Closer Look at Amazon’s Q4 Report

Amazon exited fiscal 2025 with a stellar quarter that looked solid on the surface, but left investors reading between the lines. The company's fourth-quarter net sales of $213.4 billion, up 14% year-over-year (YOY), and that’s a clear sign that demand across its vast ecosystem is still holding steady.

The real momentum, though, came from Amazon Web Services. AWS generated $35.6 billion in revenue, up 24% from a year ago, marking its fastest growth pace in over a year as AI workloads and enterprise cloud adoption continued to accelerate. Advertising added another layer of strength, rising 22% annually to $21.3 billion, showing Amazon is getting sharper at monetizing its massive traffic beyond just retail.

Meanwhile, EPS amounted to $1.95, slightly ahead of last year’s $1.86 but just below Wall Street’s expectations. That small miss, combined with what followed, was enough to shake confidence. The stock dropped about 5.6% the next day, as attention quickly shifted from performance to spending.

For fiscal 2025, Amazon’s revenue grew roughly 12% YOY to $716.9 billion, keeping the broader growth story solid. But free cash flow slipped to around $11.2 billion, reflecting Amazon’s aggressive push into AI infrastructure, data centers, custom chips, robotics, and satellite networks.

And that push is only getting bigger. Management signaled that capital expenditures could hit $200 billion in 2026, underlining Amazon’s intent to dominate the next wave of AI and cloud. The opportunity is massive, but so is the pressure on margins in the near term.

In a recent shareholder letter, CEO Andy Jassy highlighted the rapid pace at which Amazon’s chip business is scaling. He said the in-house chip business is set to cross $20 billion in annual revenue, growing at triple-digit rates. More striking, he noted that if this division operated as a stand-alone business and sold its current processors externally, it could potentially generate up to $50 billion a year in sales, underscoring the massive commercial opportunity ahead.

Amazon is gearing up to release its Q1 report for fiscal 2026 on Wednesday, April 29, after the market closes. The management guided revenue between $173.5 billion and $178.5 billion, pointing to 11% to 15% annual growth.

Wall Street analysts tracking Amazon project its revenue for Q1 to be around $177.15 billion, with EPS expected to rise 1.3% YOY to $1.61. For fiscal 2026, EPS is anticipated to be $7.74, indicating a 7.95% YOY surge, before rising by another 21.5% annually to $9.40 in fiscal 2027.

What Do Analysts Expect for Amazon Stock?

Recently, Oppenheimer raised AMZN’s price target to $275 from $260 while maintaining an “Outperform” rating. The brokerage firm sees AWS gaining momentum, with strong growth ahead, forecasting 29% AWS revenue growth in 2026 and 30% in 2027, with upside to 42% and 44% if spending scales well.

Advertising remains solid, though slowing a bit, while fuel costs could pressure margins in the short term. Even after recent concerns around guidance, Oppenheimer believes the stock still looks reasonably valued and potentially attractive compared to its peers.

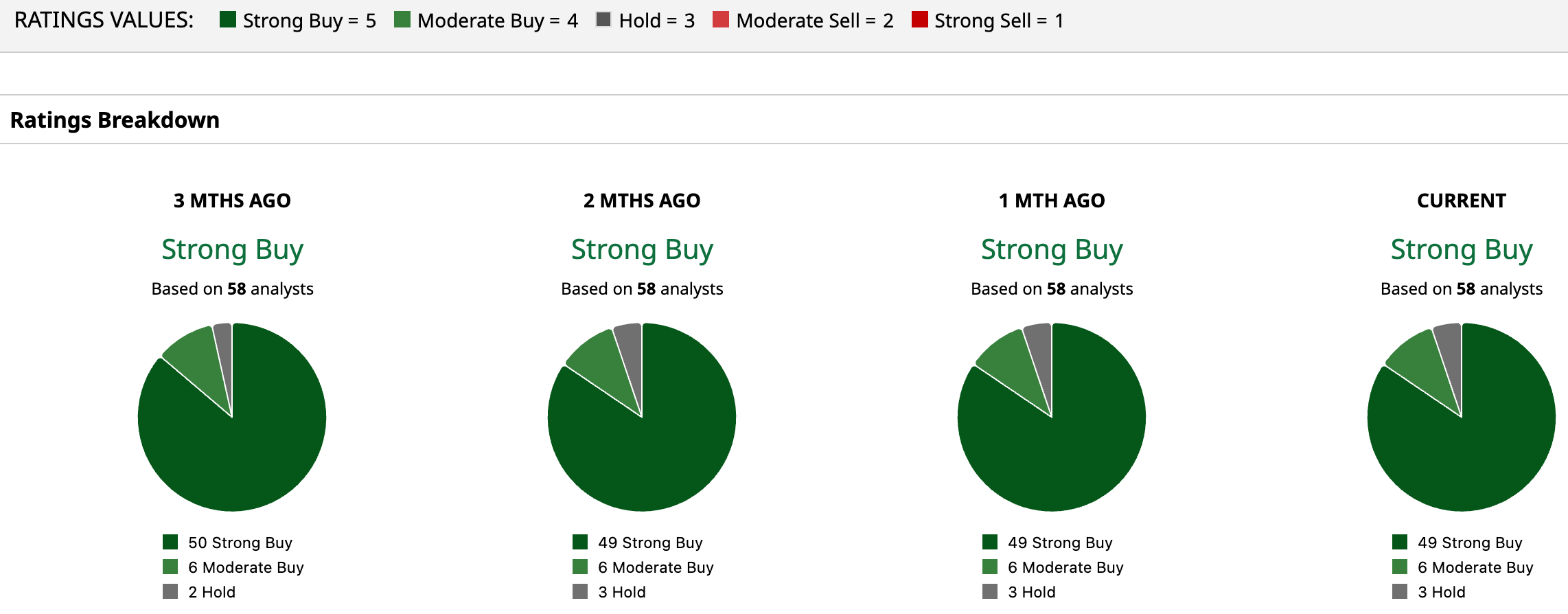

Analysts monitoring AMZN are bullish, with consensus leaning heavily toward a “Strong Buy.” Out of 58 analysts, 49 advise a “Strong Buy,” six recommend a “Moderate Buy,” and three are cautious with a “Hold” rating.

The average price target of $289.20 suggests a 10.6% upside potential from here. Meanwhile, Loop Capital’s Street-high target of $360 suggests AMZN stock could rise as much as 37.7%.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Down Nearly 30% in 2026, is SoFi Stock a Buy Before the Q1 Earnings? New ETF Filings Tout Ways to Play Prediction Markets with Your Retirement Savings. A Lot Could Go Wrong. Amazon Just Signed a Major Deal to Supply Its In-House Chips to Meta Platforms. AMZN Stock Now Has Multiple AI Chip Catalysts. Intellia Therapeutics Pops on CRISPR Trial Success. Does That Make NTLA Stock a Buy?