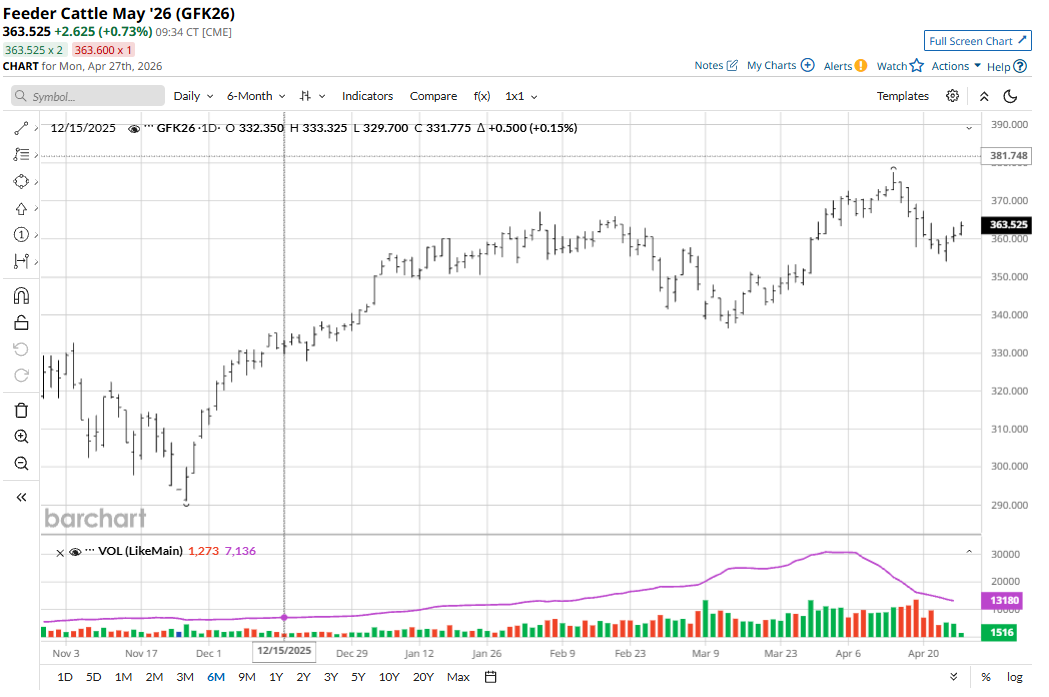

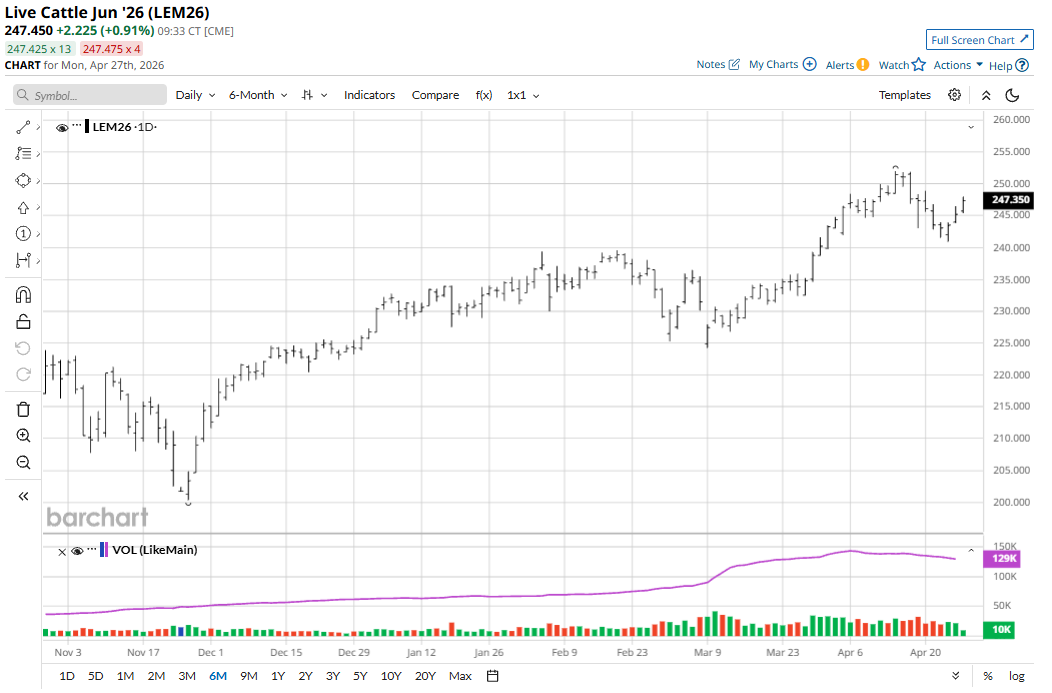

June live cattle (LEM26) futures on Friday rose $1.725 to $245.225 but for the week were down $2.475. May feeder cattle (GFK26) futures Friday gained $2.025 to $360.90 and for the week were down $4.375.

The live cattle and feeder cattle futures markets Friday saw corrective bounces, but the bears had the better week. The near-term technical postures for both markets have deteriorated further.

Don’t Miss a Day: From crude oil to coffee, sign up free for Barchart’s best-in-class commodity analysis.

Cattle are being removed from wheat fields earlier than usual, pushing April placements higher, although May could show a decline from last year. Weather remains a key driver – until drier areas receive impactful moisture, the demand for replacement cattle will likely remain subdued.

The USDA at midday on Friday reported active cash cattle trade, with steers averaging $246.00 and heifers $246.01. The agency earlier last week reported cash trading the week prior averaged $248.02.

Despite the recent dip in cash cattle prices, tight fed cattle supplies on feedlots will continue to favor feedlot operators in the coming weeks, especially with the outdoor grilling season on the doorstep. Meanwhile, packer margins have eased a bit but remain deep in the red despite firming boxed beef prices recently. That will continue to somewhat diminish cattle slaughter levels, which remain below those of one year ago.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com A worrisome element for cattle market bulls and for cattle producers is retail gasoline prices that are around the $4.00 level per gallon. If gasoline prices tick much above that level, consumer confidence will be dented and that could translate into reduced demand for higher-priced beef cuts at the meat counter. However, with U.S. stock indexes at or near record highs, such indicates consumer confidence in the coming months could remain solid.

www.barchart.com

www.barchart.com USDA Annual Cattle Slaughter Summary

The USDA last week released its annual cattle slaughter summary report, providing finalized data for U.S. meat production in 2025. In addition to the regular monthly reports, the annual provides insight on where meat production is concentrated as well as the number of plants operating as of Jan. 1, 2026.

Red meat production was down 2% from 2024 to 53.8 billion pounds. Beef production came in at 26.1 billion pounds, down 4% from 2024, while pork production was up 1% to 27.6 billion pounds. The numbers were little changed from the preliminary end of year estimates released in late January that showed 53.74 billion pounds of red meat production for 2025.

The report said 49.4% of commercial U.S. red meat production was focused in four states: Iowa (16.6%), Nebraska (14.4%), Kansas (10.4%), and Texas (8.0%). The total number of federally inspected plants increased from 1,089 on Jan. 1, 2025, to 1,127 on Jan. 1, 2026. There was a slight decrease in non-federally inspected plants from 1,827 to 1,796. In total, the number of plants increased by 7 to 2,923 in the U.S. Notably, Texas led states with the most new plants under federal inspections, up 9, to78.

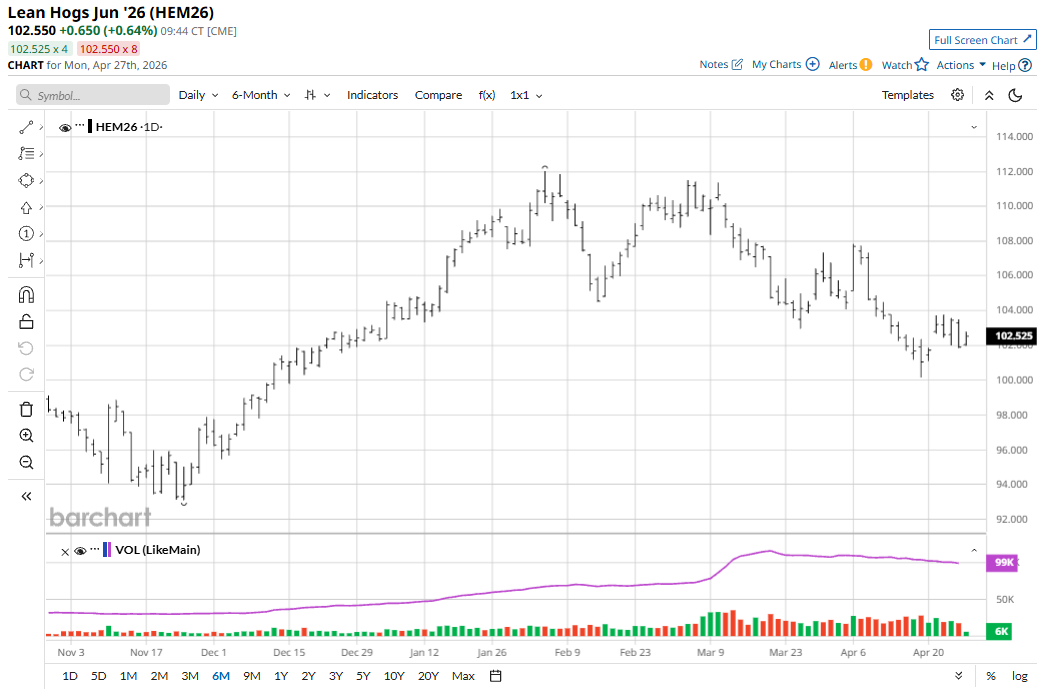

Lean Hog Futures Bulls Work to Stabilize Prices

June lean hog (HEM26) futures on Friday fell $1.55 to $101.90 but for the week were up 85 cents. The futures market saw technical selling pressure to end the trading week as prices remain trapped in a downtrend on the daily bar chart.

The latest CME lean hog index is up 38 cents to $91.43. Monday’s projected cash index price is up a penny to $91.44.

www.barchart.com

www.barchart.com Both cash hog and wholesale pork fundamentals have improved of late. Domestic demand remains relatively flat, although grocers should begin ramping up purchases for Memorial Day features and to meet summer grilling demand before slaughter and supplies wane seasonally. However, a potentially price-bearish element is that both average hog and carcass weights have risen in recent weeks.

Export demand for U.S. pork needs to pick up for cash hog, fresh pork, and futures prices to trek to higher ground in the coming weeks and months. Improving relations between the U.S. and China would likely mean better demand for U.S. pork from China. However, recent reports from China indicate that the nation is presently dealing with a glut of pork supplies.

Long-Term Implications of DOJ Meat Packer Investigation May Be Big

Cattle traders and feedlot operators will be keeping a close eye on developments and longer-term implications regarding the U.S. Department of Justice’s investigation into collusion in the meat-packing industry.

The DOJ investigation into the country’s largest meatpacking companies for collusion and price fixing has the potential to reshape the cattle and beef industries, longer term. However, past efforts to break the companies’ hold have gone nowhere. The White House called for an examination into the meatpacking companies’ practices after President Donald Trump, in a post on social media, accused packers of artificially inflating prices and jeopardizing the country’s food supply. A White House news release specifically named JBS (JBS), Cargill, Tyson Foods (TSN) and National Beef as targets of the investigation. The companies collectively slaughter 85% of the country’s cattle and a majority of its hogs.

Tell me what you think. I enjoy hearing from my valued Barchart readers from all around the globe. Email me at jim@jimwyckoff.com

On the date of publication, Jim Wyckoff did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Cattle, Hog Prices Are Starting to Lose Steam. Gasoline Prices, DOJ Meatpacking Investigation Are Key Catalysts to Watch. What Do We Know About the US Economy? ‘It’s Not Going to End Well’ for Investors Who ‘Get in Too Late’ to Volatile, Meme-Like Commodities. How to Trade the Chaos Instead. Dear Cattle Futures Traders, Mark Your Calendars for June 5