Emerging chip products seller POET Technologies (POET) had scored a contract with Marvell Technology (MRVL) Celestial AI (which it had acquired in February), which was expected to be a huge factor for the company’s upcoming revenue. However, Marvell accused POET of breaching confidentiality by disclosing details of these orders after acquiring Celestial, and subsequently canceled all related purchase orders.

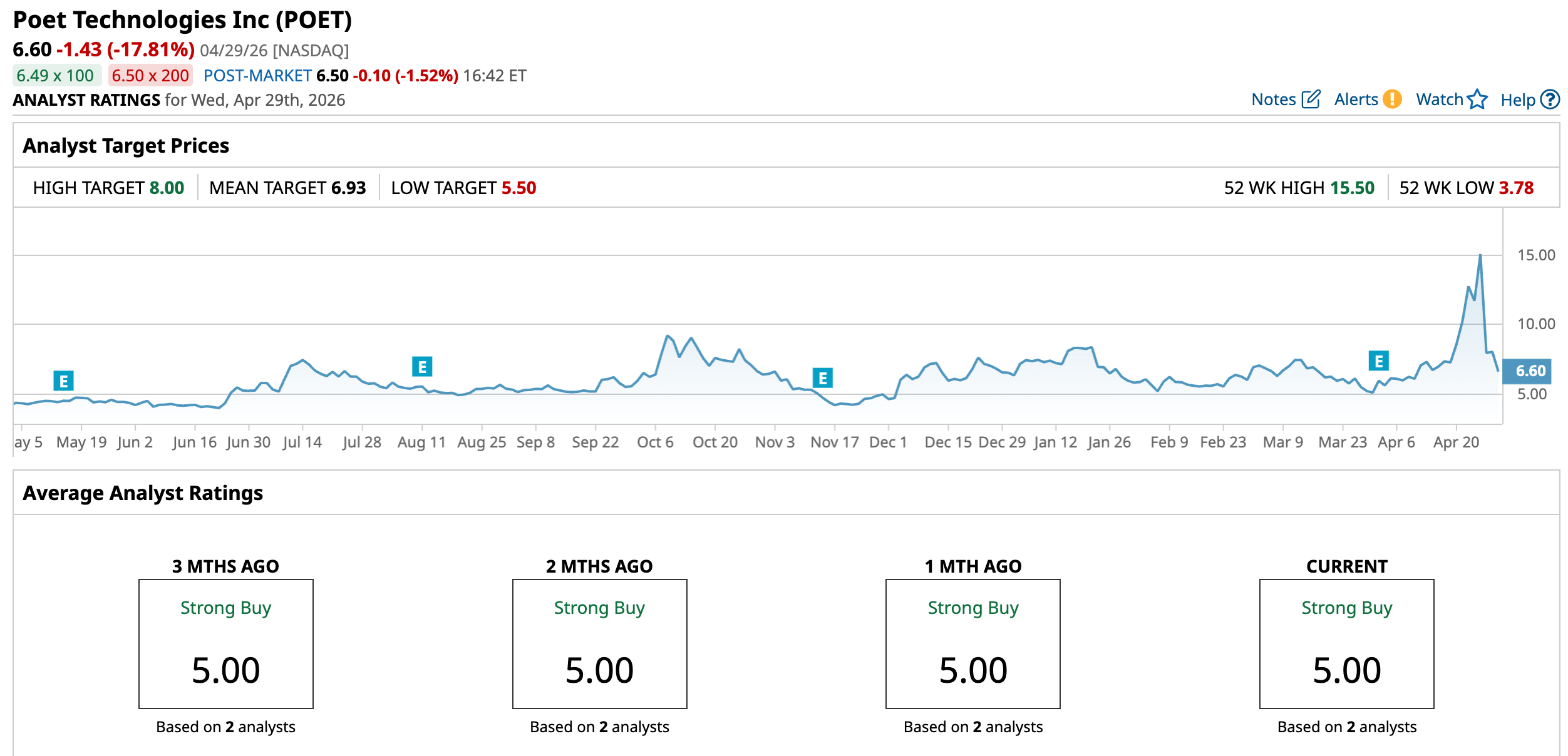

POET saw its stock dip 47.4% intraday on April 27 after losing the contract. POET had reached a 52-week high of $15.50 on April 24, but is down 57.4% from that level amid this selloff. Against this backdrop, should you consider buying POET’s stock?

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About POET Technologies Stock

POET Technologies specializes in designing, manufacturing, and selling high-performance semiconductor products that merge electronic and photonic devices on its proprietary Optical Interposer platform. Headquartered in Toronto, Canada, the company transforms traditional chip packaging by using a novel wafer-level semiconductor manufacturing process.

This approach enables seamless integration of lasers, modulators, and detectors directly onto a silicon platform, bypassing costly, complex die-to-die assembly methods common in the industry.

What sets POET apart is its ability to create compact, high-speed multi-chip modules tailored for next-generation applications like AI data centers, telecom networks, and sensing systems. The company, currently finding its footing in the chip space, has a market capitalization of $1.06 billion.

POET’s stock has surged 62.16% over the past 52 weeks, amid explosive growth in AI infrastructure demand for advanced optical interconnects. Even though the MRVL deal was snatched away, it was a key business win while it lasted. But now year-to-date (YTD), POET’s shares have been up only 4.27%.

www.barchart.com

www.barchart.com The selloff has sent POET’s 14-day RSI from the overbought category to 45.60, below the moderately bullish level, indicating that momentum has somewhat stalled. The stock still trades at a significantly high valuation. On a forward-adjusted basis, its price-to-sales ratio of 121.39x is considerably larger than the industry average of 3.14x.

POET Technologies Reported Strong Q4, Advances AI Optical Roadmap

For the fourth quarter of 2025, POET reported $341.20 thousand in non-recurring engineering (NRE) and product revenue, compared to $29.03 thousand in the fourth quarter of 2024. During the quarter, POET transitioned from “development to execution.” Of course, this requires significant capital inflows, which the company is trying to finance. POET’s quarterly net loss per share dropped by 36% year-over-year (YOY) to $0.32.

During the fourth quarter, POET secured over $225 million in financing and an additional $150 million in January 2026. The company also received an order exceeding $5 million for its POET Infinity optical engines. Notably, it completed three rounds of equity financing with new institutional investors, leading to $375 million in gross proceeds.

Before POET begins large-scale expansion, it sees an opportunity for its External Laser Small Form-Factor Pluggable (ELSFP) optical engines across both high-speed and high-power applications. Moreover, manufacturing in Malaysia is primed to start high-volume light-source production in Q2, with 800G optical engines ramping in Q3 to meet current and expected demand for POET Infinity transmit and receive engines.

Wall Street analysts have faith in POET's ability to reduce its bottom line losses. For the current year, its loss per share is expected to decline by 48.8% YOY to $0.21, followed by another 109.5% improvement to an EPS of $0.02 in the next year.

What Do Analysts Think About POET Technologies’ Stock?

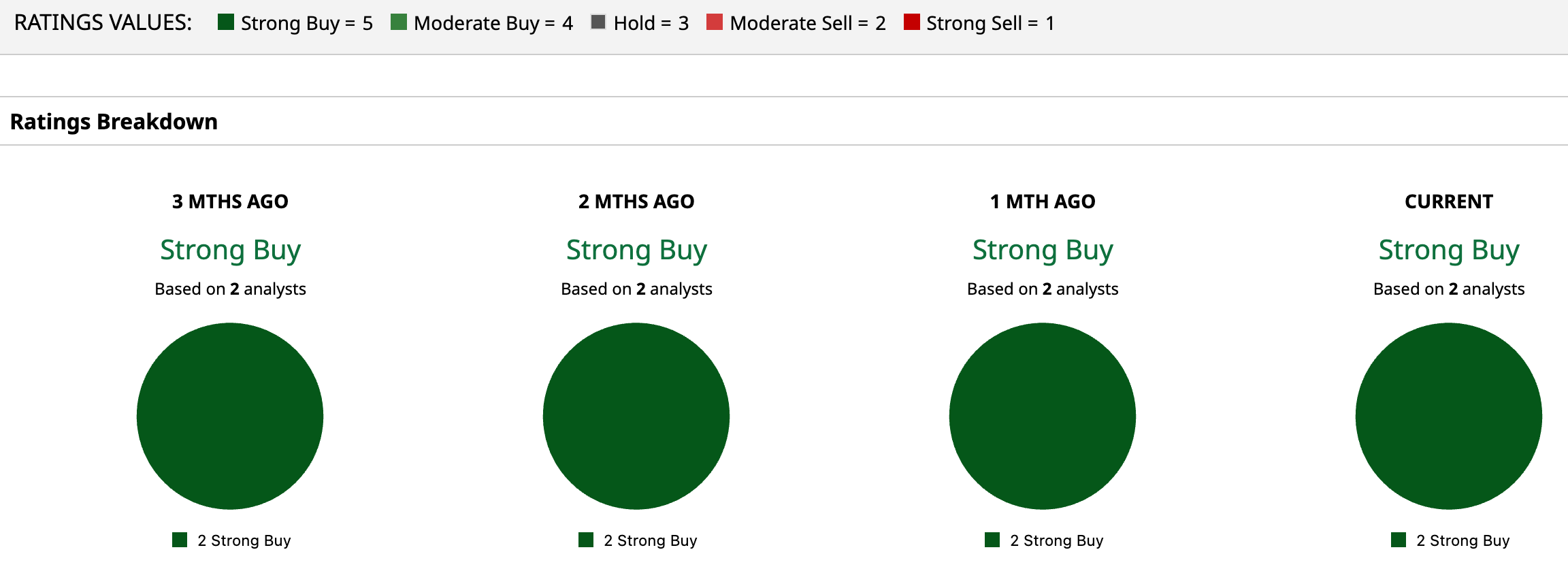

The small-cap stock has few analyst ratings. The two analysts who have rated POET’s stock have rated it “Strong Buy.” The consensus price target of $6.93 represents a 5% upside from current levels. Moreover, the Street-high price target of $8 shows a 22% upside potential from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Bottom Line

The cancellation of the order from Marvell has been a major blow to an emerging business like POET Technologies. However, the company is financing major manufacturing upscaling. Therefore, it might be wise to look into the stock if you are not risk-averse.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Down Nearly 50% from All-Time Highs, Should You Buy the dip in POET Technologies Stock? ‘I’d Love to Be Able to Save an Airline,’ Says Trump About Spirit. But Is There Any Saving FLYYQ Stock? Semiconductor Stocks Are the New Elephant in the Room at 14% of the S&P 500. How to Play This Tech Super-Sector. As Alibaba Rolls Out the Happy Horse AI Model, Should You Buy, Sell, or Hold BABA Stock?