Carnival Corporation & plc CCL and Booking Holdings Inc. BKNG operate at the heart of the global travel and tourism industry, which revolves around facilitating leisure and business travel across lodging, transportation and experiential segments. This space is influenced by macroeconomic conditions, consumer spending patterns and seasonal demand trends, making pricing power, network scale and operational efficiency critical for sustained growth.

Carnival focuses on cruise vacations, leveraging its fleet scale, onboard experiences and itinerary diversification to drive passenger volumes and onboard spending. On the other hand, Booking Holdings emphasizes its asset-light, technology-driven platform spanning accommodations, flights and other travel services, supported by a broad global network and strong digital capabilities. The face-off highlights how each company is positioned to capitalize on travel demand, manage costs and sustain margins in an evolving travel landscape.

The Case for CCL

Carnival is benefiting from strong demand momentum, as reflected in higher ticket pricing and solid onboard spending trends. The company has seen healthy booking volumes, with a significant portion of its 2026 inventory already reserved at attractive pricing levels. This demand strength is not only driving revenue growth but also improving visibility into future performance. Additionally, increased guest engagement, particularly through pre-cruise purchases and bundled offerings, has enhanced onboard revenue opportunities, supporting overall yield expansion.

Another positive lies in Carnival’s improving operational execution and long-term strategy. The company continues to focus on disciplined capacity growth while investing in high-return initiatives such as destination development and fleet enhancements. Its ongoing efforts to optimize pricing, leverage technology and improve cost efficiency are helping expand margins. Management’s long-term targets, including higher returns on invested capital and stronger cash generation, signal confidence in sustained earnings growth and a more balanced capital allocation approach.

Despite strong demand, Carnival remains exposed to significant cost volatility, particularly from fuel prices. Rising fuel costs continue to pose a meaningful headwind to profitability, with even modest fluctuations having a notable impact on earnings. While the company is working on reducing fuel consumption and improving efficiency, its limited hedging strategy leaves it more vulnerable to energy price swings compared with some peers, which can pressure margins in the near term.

Additionally, the business is inherently sensitive to macroeconomic and geopolitical uncertainties. Changes in consumer sentiment, global conflicts or economic slowdowns can affect booking patterns, especially for discretionary travel like cruises. Certain regions may experience weaker demand during periods of uncertainty, and while Carnival has the flexibility to redeploy capacity, such disruptions can still impact pricing and occupancy. This cyclical exposure makes earnings less predictable, particularly in volatile global environments.

The Case for BKNG

Booking Holdings continues to benefit from resilient global travel demand and strong execution across its platform. The company delivered solid growth in bookings, revenues and earnings, supported by steady expansion in room nights and healthy travel activity across regions. Even amid geopolitical disruptions, underlying demand trends remain intact, reinforcing the structural strength of online travel. This ability to sustain growth despite external volatility highlights the durability of its business model and global reach.

Another key strength lies in Booking Holdings’ asset-light, technology-driven model, which enables scalable growth and strong profitability. The company’s “Connected Trip” strategy, integrating accommodations, flights, car rentals and attractions, has been gaining traction, with multi-product bookings growing faster than overall transactions. This ecosystem approach not only enhances user experience but also drives higher engagement, repeat usage and incremental revenue opportunities, strengthening its competitive positioning over time.

Booking Holdings is also leveraging innovation, particularly in artificial intelligence, to improve customer experience and operational efficiency. Investments in AI-driven tools, personalization and automation are helping boost conversion rates, reduce service costs and streamline processes. At the same time, its strong direct booking channel, loyalty program and global brand portfolio provide a durable moat, enabling the company to capture demand while maintaining marketing efficiency and long-term margin expansion potential.

Despite its strengths, Booking Holdings remains exposed to macroeconomic and geopolitical risks that can disrupt travel demand and booking patterns. Events such as regional conflicts can lead to increased cancellations, softer booking trends and volatility in key travel corridors, impacting near-term growth. Additionally, fluctuations in travel costs, currency movements and broader economic uncertainty can weigh on consumer sentiment, making performance somewhat sensitive to external factors beyond the company’s control.

How Does the Zacks Consensus Estimate Compare for CCL & BKNG?

The Zacks Consensus Estimate for Carnival’s fiscal 2026 sales and earnings per share (EPS) indicates year-over-year increases of 4.5% and down 0.4%, respectively. Over the past 30 days, earnings estimates for fiscal 2026 have been revised downward, as shown in the chart.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Booking Holdings’ 2026 sales and EPS implies year-over-year growth of 10.6% and 15.5%, respectively. Over the past 30 days, earnings estimates for 2026 have been revised downward.

Image Source: Zacks Investment Research

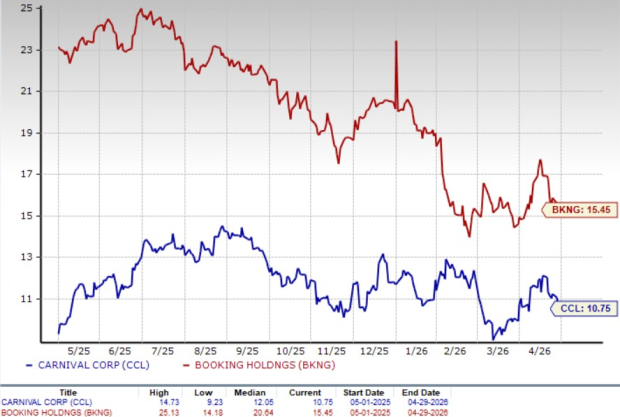

Price Performance & Valuation

Carnival’s shares have declined 21.2% in the past three months. Meanwhile, Booking Holdings stock has declined 15.1% over the same period, against the S&P 500’s 2.1% rise.

Price Performance

Image Source: Zacks Investment Research

CCL is trading at a forward 12-month price-to-earnings ratio of 10.75X, below its median of 12.05X over the last year. BKNG’s forward earnings multiple sits at 15.45X, below its median of 20.64X over the same time frame.

P/E (F12M)

Image Source: Zacks Investment Research

Wrapping Up

The comparison suggests a clear divergence in risk-reward profiles between Carnival and Booking Holdings. While Carnival is seeing solid demand and improving operations, its earnings outlook appears pressured by cost volatility, particularly fuel, along with sensitivity to macro and geopolitical disruptions that can quickly impact bookings and margins.

In contrast, Booking Holdings’ asset-light model, diversified global platform and strong execution continue to support more resilient growth, even in uncertain conditions. Its focus on technology, ecosystem expansion and customer engagement provides better visibility and structural advantages over time. Given these factors, the setup favors avoiding Carnival due to its higher earnings uncertainty, while maintaining a hold stance on Booking Holdings, which remains better positioned to navigate volatility and sustain long-term growth.

BKNG currently has a Zacks Rank #3 (Hold), while CCL carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Carnival Corporation (CCL): Free Stock Analysis Report

Booking Holdings Inc. (BKNG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).